At last glance, 30-year fixed mortgage rates were sitting above 7%. Despite this, there are virtually no homes for sale.

One would assume that after such a massive interest rate spike, demand would flounder and supply would flood the market.

Yet here we are, looking at a housing market that has barely any for-sale inventory available.

And when you remove the new home inventory (from home builders) from the equation, it’s even worse.

Let’s explore what’s going on and what it might take to see listings return to the market.

Why There Are No Homes for Sale Right Now?

The housing market is highly unusual at the moment, and has been for quite some time.

In fact, since the pandemic it’s never really been normal. The housing market came to a halt in early 2020 as the world stopped, but then took off like a rocket.

If you recall, the 30-year fixed spent the entire second half of 2020 in the sub-3% range, fueling voracious demand from buyers.

And as Zillow pointed out, the age demographics had already lined up nicely for a surge of demand anyway.

Around that time, some 45 million Americans were expected to hit the typical first-time home buyer age of 34.

When you combined the demographics, the record low mortgage rates, a pandemic (which allowed for increased mobility), and already limited inventory, it didn’t take much to create a frenzy.

At the same time, you had existing homeowners buying up second homes on the cheap, due to those low rates and generous underwriting guidelines.

And let’s not forget investors, who were taking advantage of the very accommodative interest rate environment and the insatiable demand from buyers.

The rise of Airbnb and short-term rentals (STRs) coincided with this low-rate environment, potentially taking additional inventory off the market.

This quickly depleted supply, which was already trending down thanks to a lack of new home building after the prior mortgage crisis.

Home builders got burned in the early 2000s as foreclosures and short sales spiked and prices plummeted. And their excess supply sat on the market.

As a result, they developed cold feet and didn’t build enough in subsequent years to keep up with the growing housing needs of Americans.

Collectively, all of these events led to the massive housing supply shortage.

Low Mortgage Rates Got Buyers in the Door, But Will They Ever Leave?

Low supply aside, another unique issue affecting housing supply is a concept known as mortgage rate lock-in.

In short, there’s an argument that today’s homeowners have such low mortgage rates that they won’t sell. Or can’t sell.

Either they don’t want to give up their low mortgage rate simply because it’s so cheap. Or they are unable to afford a home purchase at today’s rates and prices.

Simply put, most can’t trade in a 3% rate for a 7% rate and purchase a home that’s probably more expensive than theirs was a few years earlier.

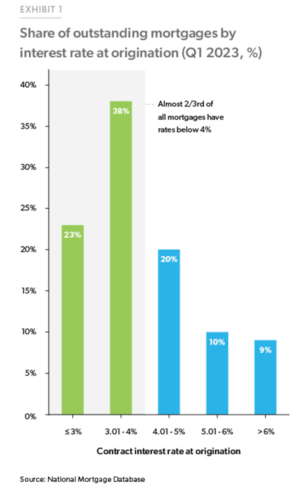

And this isn’t some tiny subset of the population. Per Freddie Mac, nearly two-thirds of all mortgages have an interest rate below 4%.

And nearly a quarter have a mortgage rate below 3%. How on earth will these folks sell and buy a replacement home if prices haven’t come down, but have in fact risen?

The answer is most will not budge, and will continue to enjoy their low, fixed-rate mortgage for many years to come.

This further explains why inventory is so tight and not really improving, despite the Fed’s attack on housing demand via 11 rate hikes.

[Why are home prices not dropping?]

Housing Supply Is at an All-Time Low

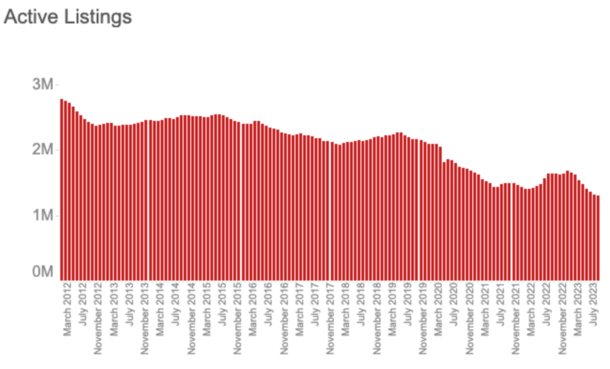

Redfin reported that the total number of homes for sale hit a record low in August.

Active listings were down 1.1% month-over-month on a seasonally adjusted basis, and a whopping 20.8% year-over-year.

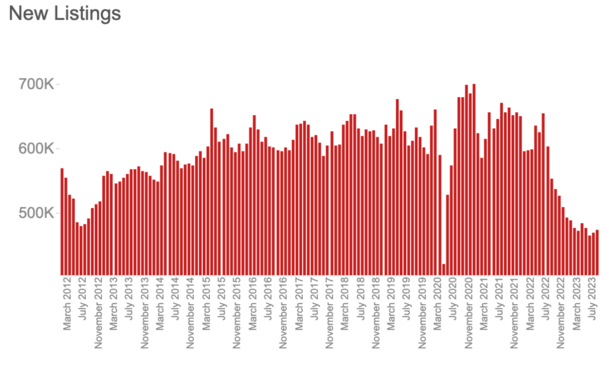

That’s the biggest annual decrease since June 2021. However, new listings have ticked higher the past two months on a seasonally adjusted basis.

In August, new listings increased 0.8% from a month earlier after increasing the month before that.

But due to nearly a year’s worth of monthly declines prior to that, new listings were still off a big 14.4% year-over-year.

This meant months of supply stood at just two months, well below the 4-5 months usually considered healthy.

Redfin Economics Research Lead Chen Zhao noted that “new listings have likely bottomed out,” arguing that those who are locked in by low rates have already decided not to sell.

That leaves those who must sell their property, due to stuff like divorce or a change in work-from-home policy.

Interestingly, even some WFH homeowners are moving back closer to work, but keeping their homes because they can rent them out.

Because homeowners got in so cheap, it’s not out of the question to keep the old house and go rent or buy another property.

All of this has created a huge dearth of existing home supply, but there is one winner out there.

Home Builders Are Gaining a Ton of Market Share

While existing homes, also known as previously-owned or used homes, are hard to come by, newly-built homes are somewhat plentiful.

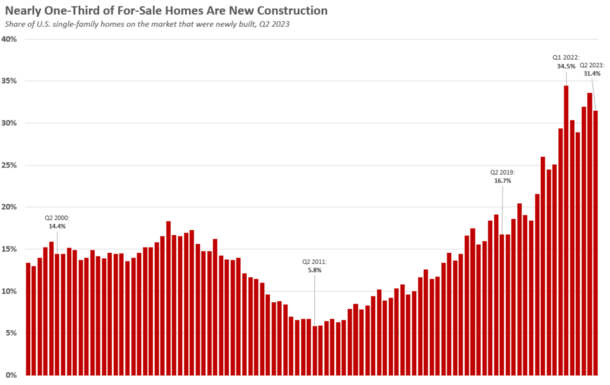

In fact, newly built single-family homes for sale were up 4.5% year-over-year in June, per Redfin, while existing homes for sale were down 18%.

And roughly one-third of homes for sale were new builds, up markedly from prior years and well above the norm that might be closer to 10%.

Astonishingly, new homes accounted for more than half (52%) of single-family homes for sale in El Paso, Texas.

Similar market share could be seen in Omaha (46%), Raleigh (42.1%), Oklahoma City (39%), and Boise (38%).

Meanwhile, the National Association of Realtors (NAR) predicts that new home sales will increase 12.3% this year, and 13.9% in 2024.

As for why home builders are seeing a big increase in market share, it’s mostly due to a lack of competition from existing home sellers.

In short, they’re the only game in town, and they don’t need to worry about finding a replacement property if they sell (like existing homeowners)

Additionally, they’re able to tack on huge incentives such as rate buydowns, including temporary and permanent ones, along with lender credits.

This allows them to sell at higher prices but make the monthly payment more palatable for the buyer.

Perhaps more importantly, it allows buyers to still qualify for a mortgage at today’s sky-high prices.

When Will More Homes Hit the Market?

For now, this new reality is expected to be the status quo. After all, those with so-called golden handcuffs have 30-year fixed-rate mortgages.

That means they can continue to take advantage of their dirt-cheap mortgage for the next few decades.

This includes second home owners and investors, who got in cheap when prices were much lower and mortgage rates were also on sale.

Meanwhile, the home builders don’t seem to be going nuts with supply, and even if they ramped up production, it wouldn’t satisfy the market.

Remember, existing home sales typically account for around 85-90% of sales, so builders won’t come close to satisfying demand.

The only real way we get a big influx of supply is via distress, sadly. That could be the result of a bad recession with mass unemployment.

And it could be triggered by the 11 Fed rate hikes already in the books, coupled with a lack of new stimulus and the resumption of things like student loan payments.

Compounding that is sticky inflation, which has made everything more expensive and is quickly depleting the savings accounts of Americans.

But even then, you could argue that a mass loan modification program would be unveiled to at least keep owner-occupied households in their properties.

Considering how cheap their housing payments are, assuming they’ve got a low fixed-rate mortgage, it’d be hard to find them a cheaper alternative, even if renting.

In the early 2000s this wasn’t the case because the typical homeowner held a toxic mortgage, such as an option ARM or an interest-only loan. And many weren’t even properly qualified to begin with.

Read more: Today’s Housing Market Risk Factors: Is Real Estate in Trouble?

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

- Mortgage Rates Are Now Higher Than They Were a Year Ago - August 5, 2026