So you need a job and you’re thinking about becoming a residential mortgage loan officer? Or a mortgage loan originator (MLO) as they’re now known.

Well, there are probably job openings right this very second, but it’s not for the faint of heart.

It’s true, loan officer jobs pay more than most any other occupation out there, assuming you haven’t passed the bar or made your way through medical school. Or happen to be a financial advisor or a pro athlete.

But it can’t be that easy, could it? To make six figures without a high school diploma you would think you’d have to invent something or start your own business.

Not so – the prospect of being a loan officer has changed conventional thought, especially as the housing market shot off in recent years like a bottle rocket.

Jump to loan officer topics:

– Loan Officer Job Description

– Loan Officer Educational Requirements

– Loan Officer Salary

– Loan Officer Career Advancement

– How to Be a Top Producing Loan Officer

– What the Future Holds for Loan Officers

So now as we lie in the wake of another possible housing bubble bust, are loan officers still making money? The answer is MAYBE.

But the number of loan officers has probably been cut in half, if not more in the past year or so.

At the same time, the quality (and quantity) of mortgage loans at the moment isn’t what is once was a few years ago.

It seems most of the smart money already refinanced, or made home purchases before values went up. And many of the remaining deals are tricky and/or riddled with hurdles and low credit scores.

In truth, it can always feel that way when you’re trying to get a home loan approve. A mortgage loan originator’s typical day will never be easy.

But there’s always an opportunity for a loan officer, even if the market is in a down cycle or a lull. Even if mortgage rates aren’t as low as they once were.

Being a Loan Officer Can Be Really Lucrative

- There are few jobs other than doctors, lawyers, and sports stars

- That pay several hundred thousand dollars a year in salary

- Top loan officers have the potential to make that kind of money too

- And even average ones can make six-figures annually during good years

If a mortgage loan officer gets just one of those deals to go through, it often equates to a huge payday.

Sometimes as much as a few months’ salary working a minimum wage job or another low-paying job.

So that’s the incentive, big money. But there are a number of questions you need to ask yourself before setting out in the mortgage industry as a loan officer.

First and foremost, it is not an easy job. Sure, a mortgage broker or bank may tell you that it’s simple.

And you may not have to work very hard in the traditional sense. Or take part in any back-breaking work.

But factor in the stress, the near misses, lost deals, the shots to your ego, and the wheel-spinning and it isn’t as effortless as they may make it out to be.

There Will Be Ups and Downs

You will see deals fall through and you will waste a lot of time. There will be mental breakdowns as loans slip through your fingers, and brokers and real estate agents scream at you as deadlines close in.

You will undoubtedly make mistakes, which require a phone call to the borrower to let them know you can’t do the deal. It will be embarrassing and unpleasant.

But if you can handle all that, being a loan officer can be quite lucrative, and fairly easy if you get yourself organized and educated on mortgages and the many loan options available to homeowners.

It’s not for everyone, and there is definitely a lot you need to learn before starting a career in mortgage. But once you get a taste of the money you may have trouble walking away, no matter how high the stress and quality of your life.

Trust me, I know lots of people who can’t leave. They want to leave, but they can’t because they know they won’t earn as much elsewhere. And they’ll probably hate that other job too.

All that aside, let’s look at a loan officer’s typical day, not that any day is ever typical…

Loan Officer Job Description

- Sell, sell, sell! Always be closing!

- That’s pretty much the job description of a loan officer

- But you also have to be well-versed in customer satisfaction, mortgage lingo, and product knowledge

- And stay up-to-date on the many rules/regulations involved

First off, a loan officer may be referred to as a mortgage planner, lending officer, MLO, mortgage specialist, dedicated lending associate, loan consultant, loan agent, mortgage professional, senior of any of these, or junior of any of these.

There are lots of creative names for the position depending on the company in question, but the job description will likely be the same regardless.

A loan officer may come into work in the late morning around 9 or 10am and work until 6-9pm.

The time may be structured to work around when companies are allowed to solicit consumers in their homes. The traditional peak hours for sales calls take place in the early evening, between 6pm and 9pm.

Of course, you could also be a go-getter who arrives at 6am and only works until the early afternoon. There is certainly flexibility when it comes to working hours, though it does depend on the type of company you work for.

It Could Be a 9 to 5 Job

If you work for a large company, such as a depository bank, credit unions, or a mortgage banker, chances are you’ll work the typical 9-5 schedule since bank branches are only open during those hours.

If you work for a smaller mortgage company, or a broker, you might be able to set your own hours and do whatever you please.

This has to do with compensation, as the former will likely get a base salary along with commission, while the latter will likely be a commission-only employee.

Mortgage brokers won’t care when you come in or leave as long as you’re closing loans.

Money aside, the culture will be a lot different at a large lending institution versus a small shop. If you can stomach a dress code and an uber-corporate environment, the bank setting might work out nicely.

If you’re the type who would prefer to run your own business, but don’t have the knowledge or the wherewithal, a small shop could be a desirable place to be. At least to start.

What Does a Loan Officer Do on a Daily Basis?

- Selling is the main focus of a loan officer

- That means bringing in new customers to apply for home loans

- Whether it’s a refinance loan or a purchase loan

- So you can earn a commission when it eventually funds

The broker or bank, or whomever employs the loan officer, may provide sales leads to the loan officer, or they may be completely on their own when it comes to acquiring business, making up their own sales and marketing to pitch potential borrowers.

If you work at a large bank or call center, you may be fortunate enough to just take incoming phone calls.

That means you’ll sit in a cubicle all day and field phone calls. You could also be required to follow-up with customers who expressed interest.

The good part is that you won’t have to find prospects on your own. That can be the hardest part.

If you work for a broker or a small company, you may still be provided with leads, though the quality could be less than desirable. That means you will have to network, make contacts, and market yourself and your services.

This entails trying to get individuals to finance home purchases or refinance their existing mortgages. That’s it. When that happens, you generally get paid.

Often, loan officers will implicitly or explicitly partner with a real estate agent or office so they can provide financing to their home buying prospects.

If you’ve ever purchased a home, you’ve likely had the preferred lender’s contact info thrown your way when it comes time to fill out a loan application.

A loan officer may get these leads and run no-obligation pre-approvals for those clients to win them over. Often, a real estate agent’s recommendation will end up providing financing since borrowers don’t tend to shop around.

Loan Officer’s Job Is to Sell!

In any case, your role as a loan officer is to sell and that’s pretty much it. If I had to sum up a loan officer jobs description, I’d simply say selling.

Sure, you’ll have to put your clients at ease throughout the loan process, and communicate with your staff, but the main objective is sales.

You won’t be doing the loan underwriting, nor will you approve loans that come in the door. That’s not part of your job description.

Loan officers at smaller shops and independent companies need to self-manage their time, and strive to call out up to 100 contacts a day. When demand for loans is low, it can be really tough.

Once a call is successful and a loan officer is able to retrieve a prospective customer’s information, they need to secure financing for their client.

If you work for a broker, you will also need to work with third-party banks and lenders (and Account Executives) to secure financing.

If you work directly for a bank or mortgage lender, you will need to familiarize yourself with the company’s entire product suite so you know what it is you’re selling.

In both situations, your main objective will be to originate loans and assist in processing them, at the same time making sure your borrower is attended to during the entire loan process.

Loan Officer Educational Requirements

- Depending on where you work you may need to be licensed

- It may easier to get started at a big bank than a smaller mortgage shop

- You’ll likely also have to pass a background check and get fingerprinted

- And potentially complete continuing education

Interestingly, you can become a loan officer with no experience. Yep, it’s a potentially high-paying job that also welcomes newbies.

In fact, mortgage loan officers don’t even need a bachelors degree, let alone a high school diploma to gain employment with certain brokers and mortgage lenders.

With the larger financial institutions, a college degree will likely be obligatory without notable sales experience.

In terms of licensing, it depends on the state, company, and specific position. These days, many loan officers need to be licensed, though there are still many positions at large retail banks that don’t require an MLO license.

Loan Officer Background Check

However, most MLOs need to be registered, perform a background check, and get fingerprinted. This is to protect the public from unscrupulous individuals working for mortgage companies.

If you do need to be licensed, it’s not the end of the world. In most cases, you simply need to take 20 hours of pre-licensure education, pass a test, and complete eight hours of continuing education annually.

The takeaway is that it might be easier to get a job at a retail bank, but these loan officers may be less knowledgeable as a result, and they could be lower paying jobs.

Of course, they may also be the ones that tend to work in call centers and simply plug in numbers into a loan application, as opposed to coming up with creative loan solutions. So they may not need to know very much.

Loan Officer Salary Can Vary Widely

- Similar to a real estate agent’s salary, a loan officer’s take home pay can range dramatically

- It all depends on how much you sell/close in a given year

- If you’re a top loan officer, you can make a ton of money (even $1 million+ annually)

- If you’re just an average or underperforming LO, expect comparably lower salaries

Wondering how much a loan officer makes an hour? Or what the average mortgage loan officer salary is?

Well, take note that most loan officers do not receive a base salary, only commission, so they are paid for performance. Sales performance.

*Some companies use non-commissioned loan officers like Better Mortgage, but it’s uncommon.

The median annual income for a loan officer in the United States was $63,380 as of May 2021, according to the Bureau of Labor Statistics (BLS). That works out to an hourly wage of $30.47 per hour, which isn’t terrible by any stretch.

And there were about 355,000 loan officers employed as of 2021, which has likely fallen as mortgage rates jumped higher.

My assumption is that the number won’t change a great deal in 2022 or beyond, not that I would focus on the numbers from the Bureau of Labor Statistics anyway.

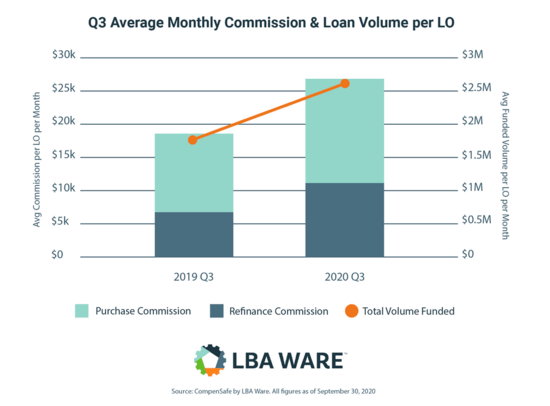

A better gauge might be the quarterly reports from a company called LBA Ware, which has a ton of data on loan officer compensation.

They said the average LO produced 51% more in volume during Q3 2020 ($2.6M per month) versus $1.7M per month in the same period in 2019.

And per-loan commission was 106 basis points in the third quarter of 2020, meaning the average LO made over $27,000 per month.

That works out to over $300,000 annually if they’re able to keep that up consistently.

There Will Be Good Years and Bad Years

As awesome as those numbers look, the mortgage market has cooled considerably. So loan officer who made six figures in 2020 may now be struggling to make five figures.

They could be even laid off due to the unprecedented rise in mortgage rates.

And while the salary may seem super high, the average pay could be skewed by the sheer number of loan officers who do very little. Or are simply unsuccessful.

So you might have some big shots closing tons of jumbo loans while others languish and close next to nothing. These types of loans can pay a ton because of the large loan amounts.

Ultimately, loan officers have the ability to earn several hundred thousand dollars a year (or more). If they work hard and make the right connections.

The salary broken down as a hourly wage could be very high if loan volume is solid and efficiency is high (aka not a lot of wasted hours chasing bad leads).

How Much Does a Loan Officer Make an Hour?

- Some loan officers are paid hourly if they work at big retail banks

- And may not actually be paid on their loan volume

- But many loan officers are paid commission-only in lieu of a base salary

- Which you can break down into hourly wages at year-end (it may often be much better than a guaranteed hourly wage)

As noted, MLOs are typically not paid hourly, and are instead paid commission for the loans they bring in and fund.

This means total compensation can range significantly based on the sales performance of the loan officer in question. It also depends on how much a loan officer makes per loan.

If the LO works for a small shop and has very little support, they might make a mortgage point or two per loan. By that, I mean 1-2% of the loan amount, which may or may not be split with their broker or mortgage company.

On a $500,000 loan, we’re talking $5,000 – $10,000, less any costs and splits. As you can see, the money can be really good if you’re even mildly successful in this industry, especially if you operate in an expensive region of the country.

Conversely, those who work at big banks and credit unions and are essentially fed a constant stream of clients via walk-ins, incoming phone calls, and the like, may only receive a small commission relative to those going it alone.

What About a Loan Officer at a Big Bank?

For example, we might be talking about 20-30 basis points, or bps, per loan closed. Represented as a fraction, that’s .20% to .30% of the loan amount.

Using the same $500,000 loan amount, that’s $1,000 to $1,500 per loan. Still good, but not as lucrative as our earlier example.

However, this latter group might get a small base salary, along with benefits like 401k and insurance and so forth. And as noted, they get leads, which can be huge for the individual who is unable or unwilling to chase after new business.

If you work for a wholesale mortgage lender and are an Account Executive (the LO equivalent), the commission might be even lower, sometimes less than 10 bps per loan.

Lastly, let’s talk about quotas. Sometimes the company you work for will have a monthly quota that must be met to get paid the higher rates of commission.

So if you don’t close X million per month, you might get paid a lot less, possibly just a fixed dollar amount per loan, such as $250 or $500.

Be sure to take a good look at the company’s compensation package so you fully understand all the particulars. And if you don’t, speak up and ask for clarification.

Loan Officer Career Advancement

- It’s generally a lateral move from one shop to another based on compensation structure

- Other than going from say a junior loan officer to a senior loan officer

- Most LOs just switch companies to get better commissions

- Though it might be possible to open your own shop or become a sales manager as well

Loan officers generally stay in one place and don’t advance internally within a company.

They may change their status to Senior Loan Officer, but usually it means very little aside from the fact that they’ve been around a little longer than typical loan officers. There could be a bump in compensation levels though.

More likely, loan officers can advance externally if recruited by other companies paying higher commissions, or even a base salary. Or a mega bonus to jump ship.

Those who are able to create and manage a large book of business may wind up with a lot of suitors, and it’s not out of the realm of possibilities to be offered a six-figure bonus to change companies.

Many loan officers also apply for a broker’s license as a means for advancement. And eventually employ their own loan officers, and take a cut off everything they earn.

In that sense, there are a variety of advancement opportunities for successful individuals. It’s also possible to shift to the operations side of things (in a mortgage-related occupation) if you turn out to be not much of a salesperson.

How to Be a Top Producing Loan Officer

- It’s simple really and there’s no secret formula

- Work hard and close as many loans as possible

- You can accomplish this by solid networking and putting in the time

- There’s nothing magical about it, just strong work ethic

While there might be gimmicks and top 10 lists and classes that teach you “how to sell,” it really comes down to hustling. Honestly.

If you’re committed to the business, you can be really successful and earn a ton of money. When I worked for a wholesale lender, there were Account Executives who sat around and complained, and others who just put their heads down and dialed the phone.

That latter group made a lot of money, while the complainers made average salaries and eventually quit. Ultimately, it’s about work ethic and drive.

All the other stuff, like education and the art of selling, will come with experience. You can’t teach someone how to sell in a class, nor can you teach them everything about mortgages in a day or a week.

It takes time and real-life experience to master those things. But without motivation and hard work, it will mean very little.

So if you want to be successful as a loan officer, you need to work hard and network. Don’t be shy, make calls, visit real estate offices and link up with real estate brokers, and eventually it will get easier and easier.

Sure, you might have some nervous calls and meetings early on, but once you gain confidence, it’ll become second nature and pay dividends.

What Does the Future Hold for Loan Officers

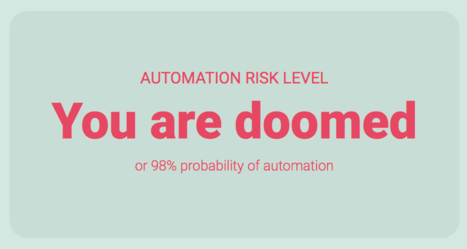

Lastly, let me point out that because of the way technology is going, the loan officer position might be at risk in the near future.

According to the site willrobotstakemyjob.com, loan officers have a 98% chance of losing their jobs to robots, aka automation.

There are around 355,000 loan officers nationwide, and 4% growth is expected between now and 2031.

But at some point, they may be phased out thanks to disruptors. In fact, we’re already seeing it with companies like 360 Mortgage Group and Homie.

So that’s something to keep in mind. Though as mentioned, it might be possible to make moves to related positions that open up as a result of technological advances.

Final Word on Loan Officers

To sum it up, loan officers have the potential to make more money than the majority of the population, including doctors and lawyers.

And even pro athletes if their careers are long enough, but financial situations will vary greatly based on sales performance.

The amount of time and work you put in is paramount, and you must be very driven to excel in the mortgage industry. It can be a very cut-throat field, filled with stress, deadlines, and missed opportunities.

After all, we’re talking about a lot of money and big life moments for the families taking out these loans. So it’s not to be taken lightly.

The job certainly isn’t for everyone, but if you think you’ve got what it takes, it can be very fruitful and lead to other opportunities, such as being a broker, working with a large banking institution, or working in commercial real estate, just to name a few.

Always do plenty of research about the mortgage company or broker you decide to work for to ensure you know exactly how and what you will be paid, and what is expected of you. Good luck out there!

- Did Everyone Forget Mortgage Rates Were 2-3% Back in 2012 Too? - June 8, 2026

- Mortgage Rates Now Face a Triple Threat - June 5, 2026

- Can You Have Two Mortgages at the Same Time? - June 4, 2026

Below average potential since 2009

Potential is not only a small fraction of what it was prior to 2009, but now the time required to get someone approved has increased 100 fold.

Only people who are good at accounting, memorizing guidelines and adhering to the rules make good LOs.

Any tips on getting OUT of the business?

Rick,

Run? Just kidding. It’s a hard business to leave once you’re in because it can be pretty lucrative, as noted above.

Hi Colin,

I’m very interested in becoming a MLO myself, so much that I’ve already taken the courses, passed both exams (National and State for Florida) and already in the process of getting my license. Here’s the problem…I don’t have any MLO experience and everywhere I look experience is required. How in the world can I get any experience if companies are only hiring MLOs with experience? What gives? Where do I start? Any suggestions?

Thanks

Moses R

Moses,

Keep reaching out and look for an experienced LO to shadow. You may not get a base salary or paid straight away but it might get your foot in the door and give you a lot of good experience. Good luck!

Colin, I’ve been a MB for 29 yrs. I started my own company in 1995. Since 2007 it’s been so hard. Redid my license,, NMLS, etc. Regs are making me nuts. I LOVE what I do (did) but I find people no longer believe or trust. I can truly save them money but going nowhere. It’s time to close the doors and I don’t know what to do.

Jackie,

It’s hard to escape the mortgage industry once you’re a part of it.

Colin, good/honest article. I have been an LO at one level or another for 42yrs and it never gets easier, but it seems to keep getting more profitable–IF YOU UNDERSTAND your market place and adjust accordingly. 1st, 2nd’s, Alt-A, FHA, refi, Purchase. Just keep your eyes one and ear to the ground. The market will tell you your next opportunity.

Thank you

Jackie,

What state are you in?

I would be interested in speaking with you when you have a moment??

Don’t quit!!

Mouse

Yes, I’ve worked as an account executive, real estate agent , and vp of title company .. But b/c paper originating was my most enjoyable and most profitable. Just find your niche/talent and do your own thing. I’m just now looking to get back in with both feet and stay in! I love selling dreams and money. What a fun business that always keeps you on your feet and multi tasking and directing others to help you get that approval and closing. Anyone in south Florida who needs a partner let me know . Best wishes

I have been working with a credit repair company and I am interested in becoming a MLO in the state of Utah. Is it better to find a company before I start with my licensing? I would just like to know how you guys got into becoming a LO and if you guys can give me some input!

I just started 4 weeks ago as a mlo. I’m having a hard time getting apps. I’ve consistently (weekly) visited real estate offices, taken treats/chatted, and I feel like I’m spinning my wheels. Any advise?

Thanks

Carrie,

Keep at it…gotta look at the long game…once you get clients, you get their referrals, repeat business, etc…takes time to get established. Consider the work now the reason you’ll get paid a lot in the future.

A major bank in CA is willing to hire me as a HMC-JR . I was once before 2007 market crash an appraiser trainee , but had to leave that indusrty as working / shadowing a CG Appraiser was not paying off. I’m now 50 years old and worked in HVAC industry for the past 7 years and climbing ladders with 75 – 95 pounds of parts, tools is not as easy as it used to be. Any suggestions??

Moses,

I can bring you on with my company. I am in Florida too.

Will

talk2william@yahoo.com

Alex,

As the article mentions, you can do very well as a loan officer, but many either quit or don’t do all that well. If you’re willing to put in the work and ride the ups and downs there’s always good opportunity as a MLO.

I’ve originated since 2007. Some years more lucrative than others but i understand the viewpoints discussed. The lender i’m with now is just simply priced out of the market because of their retail comp structure etc. I’ve had most success doing volume on lower margins and providing referral partners and clients with a competitive deal. i’m Currently licensed in 18+ states and interested in discussing opportunities. It is definitely a lucrative career path with the right structure, processing support and relationships.

Great article and very truthful. Becoming a loan officer is a tough endeavor and then succeeding as one is even tougher! Most don’t realize that it takes time to build your client/referral base but if done right it pays off for life.

When starting new, do you think it is better to work for a bank or a mortgage broker. Do banks provide leads to their mortgage bankers or is it all still self sourced like is often the case when you work for a mortgage broker.

JGlad, I would like to know this as well.

JGlad,

Big banks will probably provide leads for their loan officers because they’re so large and advertise heavily…but the compensation per loan might not be as good. You’ll probably also learn a lot more under a broker because you’ll be working with a variety of different lenders and loan programs. However, you may need to hustle to get leads, so you might not learn a thing unless you’re actually getting loans in the door.

How does working as a LO in a small town of 3,500 for a bank with four location differ from working in a bigger city for a bigger bank? Is it possible to make a decent living in a smaller setting? Do small banks pay commission only? What is the average commission rate of pay for a LO or MLO?

I began work as a dialer for a mortgage company a few months ago. I have been extremely successful and brought in a new realtor partner so that we have 2-3 new apps a day! I’m extremely good at marketing and dialing. I took pre-education and passed exams and now have my own license! My boss wants to keep me on full time dialing and is offering 2.5 bps. This seems like an insultingly low percentage. I wanted to counter at 25bps does that seem too high for the industry?

Mike,

Hard to say really – are you getting a base salary as well? Are you doing any work on the loans once you get the customer in the door? All those details matter, but it never hurts to try to negotiate better pay if you feel you’re being undervalued.

Jodi,

Not sure how the commission/pay might be structured from large national bank to smaller regional bank. I’m assuming the smaller bank would have lower volume so ideally there would be a base salary, but perhaps smaller commission. Could pay more to work for a larger bank in a call center type setting. Would have to compare pros and cons of all options.

Great article! I live in central California. I am interested in getting my home mortgage lending originator license. I am 33, I’ve been in sales all my life. My main concern before getting my license is regarding taking a paycut. I’m the only income for me & my family and I’m making about $40k a year. If I change careers it needs to be a smooth transition because I’m the only income. Any tips on how I can transition from my current job to becoming a home mortgage loan originator without taking a paycut? Where do I start? I have to at least match my income. Everything requires experience. I don’t mind shadowing someone or being a assistant to get my foot in the door. I don’t mind the work I just can’t take a paycut. All help is appreciated. Thank you

Ron,

It might be a side gig for you initially if you have time between your current job and free time…that’s one of the benefits of an LO job…it’s possible to do it on your own time.

Great read Colin. I’m stuck between a decision of leaving my current salary based position to potentially become a LO. I have jumped from job to job coming out of college for four years now and have a secured position with a salary to count on and full health benefits. I am hesitant to leave a secured job, for a field to me that is filled with so many unknowns. Any advice?

Colin,

Thanks for the informative article regarding LO.

I am a field engineer and currently working for a telecom company as a contractor. I have a BSEE since 1986. I quit telecom field and obtained a real estate broker license since 1996. I also was a mortgage broker for several years until 2008. I returned to work in the telecom field in 2011. I am close to 60 years old now and want to get back into mortgage business. I don’t like to drive folks around showing houses. My brother in law is a certified appraiser and he’s doing quite well. Should I get into Mortgage business or Appraisal business.

Please advise. Thanks again for your wonderful article.

@Chris robinson

Hi Chris,

What part of Florida you lived in?

Give me a call at (817) 881-1777 when you have a chance.

Leave me a message when I can’t get to the phone.

Thanks

Mike,

That’s a question only you can answer…as I’ve noted in the post, there are pros to working on your own such as unlimited income but that doesn’t come without risk and hard work. Good luck in your decision!

Tien,

It’s really your decision – which job do your prefer? It sounds like you’ve already done mortgages, appraisals might require new training and starting from the bottom.

I currently live Houston area and about to take my Mortgage Loan Originator course. Home sales are always pretty good around this area there are always prospects. My concern is I work as a firefighter with a schedule of 48/96 meaning I work two days straight and and 4 straight days off. While I am at work I can always take call of do any paperwork I may need to do. Would this be possible or even worth doing. My personal opinion is yes but figured I would as those that are in the industry. I also have 3 coworkers who are RE agents so not only does it make me think I can do it but now I have leads for new loans. Thank you for your time and information.

Jeff,

You could face some challenges if you have loan closings on specific days when you’re stuck working your day job…such as the end of the month rush. But I suppose it’s possible. May need an assistant though (or a solid office to work at) if you’re definitely going to be stuck somewhere else each month.

Hey Colin,

I was in the mortgage in IL and I was pretty good. I got out in 2008 and now I am trying to get back in. Do mortgage companies cover any fees involved with licensing?

Great article. I am a new Loan Originator. I can pull clients in but feel I have very little support when it comes to filling in any gaps on closing and my processors have been VERY slow. Very frustrating. I am a small business owner and I only make money when I complete jobs or close loans, the personnel above me that process get paid a salary and do not have that sense of urgency because they get paid no matter what happens.

Hey Colin,

Great article! I got my MLO license a year ago. I use to work as a Real Estate Sales Associate, worked in the industry for approximately 5 years. Still have my license active. Decided to switch Mortgage Industry and try myself in more consistent profession. Had a few clients since than. While working on the loans I faced difficulties to get them proper loan programs, inputting their information into the point software, getting conditions approved from the lender, and getting them close on time.

I came to a conclusion, that the best experience is to work for the broker as a loan processor for some time and you will learn all pros & cons. In my opinion the foundation of being a good MLO is having experience as a Loan Processor.

Please correct me if I am wrong.

Vitaliy,

I agree, loan processors are the unsung heroes of the mortgage world and often know the guidelines, necessary conditions, and potential red flags for most loan files inside and out. It’s probably a great way to learn a lot quickly.

Hello! I was recently offered a position as a Loan Officer with a mortgage broker. I will have the course paid for and leads provided (this is what was told). Question, I will be getting only commission, 37bps initially, after 4 closed loans, it increases to 50bps. Is this a good initial commission structure? Is there a standard amount? Also, I was told my current real estate license cannot be active because it will be a conflict of interest. Is this true? Thanks in advance! I am trying to make an informed decision as I am a recent mom and like the flexibility I can have working from home most of the time.

Zoraida,

Do the math to determine if it’s a good deal for you. Multiply the bps by your expected monthly volume to see if the commission is acceptable for you, or shop around to see what other companies offer. As far as giving up real estate license, it might be a state requirement or the lender’s way of avoiding any scrutiny for, as you mentioned, a possible conflict of interest.

How many basis points should an inside loan officer be paid? And how does a draw work?

Kimberley,

It really depends on the company. I suppose you can always counter whatever a company offers, and/or do the math to see if the bps they offer per loan will be enough income for you using some future production estimates. A draw is sometimes offered to LOs to tide you over until you’re actually producing. It’s basically an income advance that is paid back via future commissions.

Is an MLO a good job for someone with social anxiety? I’m a transexual (pre-op) and have many social issues. My friend told me I should become an MLO so as to be able to work at home.

What do you think?

Candy,

It depends if you feel comfortable working with people one-on-one, which is generally what loan officers do. You probably won’t have to speak in front of large groups (e.g. do presentations), but lots of one-on-one either in person or over the phone or both. Some companies may allow you to do more email communication if that’s more comfortable for you. Good luck.

I really appreciate the insight here in this post and confident it’s going to be helpful to me and many others. Thanks for sharing all the information.

I’ve been looking for a way to make more money and have considerable real estate experience in appraisal and inspection. But not mortgage. I’m in Socal and honesty can’t afford to live here any more… Generally Realtors/agents, don’t like me. I was a boy scout and have ethics and morals; I find it repulsive when a realtor will lie to a customer (withhold information) and they usually don’t call me back because I point out the house is infested or leaking… when they were trying to hide it. Is lying a prerequisite for success? Is there a personality test online that one could take to see if this is a good investment in time before making the $1000 investment in getting licensed? Thanks

Colin,

Great article! I’ve been looking to becoming an MLO. I have a Bachelor’s of Science in Business Administration with a concentration in finance. I worked a few years for mutual fund companies as a client service representative before making a career change to teaching. Now, I want to get back into the business world and would love to sell mortgages but I’m no one wants someone who has no experience. I am very teachable/coachable, I’m a quick study, I am personable, and I am comfortable with terms and definitions in finance, but no one seems to want to give me a chance. How do I get over that hurdle?

Ted,

It sounds like you’re well-suited for the position. Is it one type of company, like a big commercial bank, where you’ve been denied, or have you tried a variety of different types/sizes of banks? My guess is that someone will hire you, despite the lack of experience. You’ve got to be tenacious and keep trying, just like you would be as an MLO. Good luck!

What would be a fair compensation plan for a person that is both a Loan Officer and Loan Officer Assistant? Thanks…

Kyle,

There’s not a necessarily “fair” compensation as it can vary tremendously between company and experience of the LO. Best way to know what’s out there is to shop around and see who pays what.

To whom it may concern,

I have been a sales consultant for high value purchases for about 5 plus years now and am looking to advance into a more fruitful position. I really would like to get into either a loan officer or loan originator position. I understand you have to be licensed and I’m assuming the classes will help guide us along to what steps have to be taken to continue after the exams etc.

My question is…Where would someone like myself look to get their start?

In August of this year I will have an Bachelors in Psychology with a Minor in Business Administration, along with an Associates in Sciences.

I am a career firefighter and looking to dive into this area as a side job due to flexible schedule. Looking at retiring within 8 years and moving from northern Illinois to Tennessee. Anything I should be aware of getting into this line of business. I have associates and bachelor degrees in fire science administration. This position would not not be my main income.

Richard,

Just the stuff already noted in the article, such as the stress and ups and downs in business volume. But you probably already knew that, and as a side gig those downsides might be less of an issue. There’s also the question of how lucrative it’ll be if volume goes down in coming years since most everyone already refinanced at record low rates.

This is an awesome informational website, seriously!! I am signing up for the education this weekend, with all the openings I have seen being remote, which is what I want, do you have any idea which state would be the best to be licensed in first? I live in Florida, but have no plans or desire to go to an office. I have worked remote for 20 years and I am spoiled. Thank you!! Sue

Compliments on the article. Very informative. Seeing comments that go back 5yrs seems to realistically inform/reinforce the points made.

Actually in the process of building/buying my second home and I feel like I did a lot to educate myself this time around. I feel like my LO is solid, and she has been a pleasure to work with on this home as well as a previous refi. But as a consumer, it’s always hard trusting “salespeople” whose prime motivation is to sell me something… which is how I got to this article.

Ironically, the home buying process has inclined me to learn more about the whole industry and as a retired veteran, I believe that my desire to advocate for other veterans and interest and desire to learn more about the whole process and educate others could potentially put me on a path to becoming an LO myself. Though, I’ve always found that the most successful people are the ones that have the best mentors. How does someone that’s uninitiated seek out a mentor and find a jump off point in this field?

Great question and perhaps a difficult one to fulfill. But like anything else in the world, when you actually get your hands dirty and spend some time doing what it is you want to learn more about, the experience is invaluable. Much more so than reading about it. And along the way, hopefully you find that right person to guide you, or you simply become the guide yourself by learning who to follow and who to avoid. I like the idea of being an LO advocate for other veterans. Good luck on your quest!

I just passed the state exam. How do I start as a MLO? What are good companies to work for in CA? Any advice for a new MLO?

Thanks for this article, and your responsiveness over the years is impressive!

I have been in aircraft sales for two decades but with the current state of the industry I am considering MLO side work—I am lucky enough to have an opportunity here with a Florida company.

Can you recomend the best and/or most credible online licensing course? Google search gives me mainly ads or biased information….

Many thanks in advance!

Hi Jen,

Thanks for the kind words – I honestly don’t know much about the courses, but if obligatory, you’ll obviously need to select one. Perhaps a fellow loan officer can help you decide. Beyond that, a month on the actual job is worth years of training, it’s where you truly learn as real-life scenarios unfold fast. Good luck with your new career!

Hi Colin,

Great article and it’s even more amazing that you respond to all the questions. Thank you!

I’m curious if you still think the job will become more automated/obsolete in the upcoming future. I have asked some current LOs who don’t seem that worried and have mentioned they don’t typically lose a deal to an online company (probably b/c of upfront fees).

Also do you recommend any books for new LOs?

Hey Liam,

I know that website says the LO job is on the brink of extinction, but that doesn’t mean they’re right. And even if they are, it could be another decade to disrupt, and LOs may serve a different, complementary role at that time. In the meantime, I assume LOs are making hand over fist and we’ll worry about what happens next later. In terms of a book, I’d honestly say a week on the job would be better than any book out there, and a month on the job better than a pile of books. That being said, I don’t know of any books offhand…good luck whatever path you take!

Thank you Colin! I’m going to be jumping into the business in a couple months. I know it’s going to be a transition and tough but hopefully it won’t be too long.

Love the website and I’m sure I’ll be using it as a reference.

Hey Colin,

I’m an MLO but I have a huge difficulty finding qualified leads. What are institutions’ that give you leads called? Wholesale brokers? I’m looking to swap companies.

Thanks, J

Thank you Colin! This is a great article. I am a new mlo in Houston, TX. I have read all of the comments and I see that some people ask for advice on how to go about preparing to get licensed. I just want to share that I came across an awesome program in my opinion, Affinity Real Estate & Mortgage Training with Artricia Woods, who may rest in peace. Disclosure: I do not work for this company, but it is an awesome program for those who are trying to get their license. Good luck to everyone!

Hi Colin,

I have a BS in Finance and am very interested in becoming a LO, but I was previously denied employment from a fiduciary because of a shoplifting charge from 2009 (11 years prior). I was told the banking institutions they work with require that they not hire anyone with any degree of theft on a criminal record, no matter how small or how long ago.

I have no other arrests but I am very concerned that I am frozen out of anything to do with financial services due to such policies. You mentioned a background check and fingerprinting, do you know what would prevent an applicant from being accepted based on a background screening?

Sitting in Limbo,

Jon

Considering taking the MLO licensing exam. Is it worth it with the housing market in Northern California, specifically in Sacramento? Does anyone know what the typical salaries are?

Hi Colin.

with a very successful career first in auto sales and then auto finance I believe the skill sets transfer well to LO. it can be a very tough business like yours. customers are informed, demanding and not loyal. do you have any contacts for my transition in south florida? I am near completion of real estate licensee coursework and can take the NMLS right away. commission based pay does not scare me. thank you for any help.

Thank you for your article. I have wanted to become a loan officer for three years; but have been afraid because I had a friend whose husband made no money as a loan officer; he didn’t have leads and etc.. I keep hearing about those company called Obsidian and they have really great reviews. I really want to change my life. I also had someone tell me that its better to know someone who works the field; I’ve been teaching for 20 yrs., how do I do that? I currently teach and know I could do more with my life, I’m also not afraid to work and I also know how to listen, talk and I love to help people. I think I’m going to try. But should I wait and try to get hired over the summer in case I’m terrible I can just teach again after the summer? Or??? take the leap after I get licensed? What do you think?

Some new LOs will part-time it to get their feet wet before fully taking on the role, which as you said allows one to see if they’re cut out for it. One additional headwind right now is that with higher mortgage rates, volume is beginning to drop and it’ll be harder to get leads and close loans. But if you work hard and team with a good company, it could still be very profitable.

a lot of these comments are awful!!! come on, we bust our and it can be rewarding!

“being a loan officer is the best kept secret in my opinion”

anyone reading this, run your own race forget about the negative comments, they are subjective and some may just upset about what is going on in their life, career…

if being a loan officer is what you want, go for it.

just always think about…..integrity, character, and ethics!

i agree, it will not always be rainbows and sunshine…know your programs, guidelines, and look to your manager, and of course use your account executive (this person represents the lender you submit your loans to) they are there to help you!!!!

Hi Colin, what a blessing that your article has been around for over 7 years and is STILL offering loads of value to people who come across it!! My niece recently got into real estate. I know, this seems like an odd time as the thought of recession is on everyone’s minds. In an effort to make the “team” a family affair I’ve been looking into the MLO. Obviously, I’m not going to quit my day job, but I’ve been looking for a way to leave the corporate environment I’m in and have income while I also pursue writing. My question is if the recession hits, as a new MLO, what will this landscape look like and what should I be prepared to see in the real estate industry? I’m really, really new to all this. Thx!

Denna,

Starting up when things are slow can actually be a good time to test the waters. That way you’re primed and seasoned once the good times roll again. That being said, we’re in an extremely tough environment with very few potential mortgage candidates at the moment. So it’ll be difficult to generate a lot of business, likely for the next several years. But the mortgage biz is cyclical and will boom again at some point. In the meantime try to familiarize with all aspects of the industry, key terminology, and so on. And learn about real estate, buying/selling, home prices, and that piece as well. Not sure how many companies are hiring MLOs at the moment, and if they do, likely won’t provide base pay, but rather a draw to ensure volume comes through the door. Good luck!

Hi Colin,

Very informative article, thank you!

I currently work as a underwriter for a CU, and also worked for 4 years as a MLO Until the 2008 financial crisis hit, so I have done it before and did reasonably well. I know the industry has changed, but I am considering loan origination again, only that I would like to keep my current job while I get started. Would I be allowed to do this? Is there a regulation that prevents me from working with 2 companies in the same industry but at different capacities ?

Thank you Colin for sharing your thoughts on this.

Hi David,

Not sure if there’s a regulation, but the two employers may take issue with you working two jobs…