Last week, Zillow hosted its fifth housing forum in the nation’s capital to discuss current real estate matters.

The panel of reporters, real estate gurus, and policymakers discussed a number of issues, ranging from why people move to mortgage rates and affordability.

But perhaps the most controversial comment came from Lawrence Yun, the outspoken chief economist of the National Association of Realtors.

When the WSJ’s Nick Timiraos questioned whether the mortgage credit box was too tight, Yun took the opportunity to express his discontent with the FHA and its new sky-high premiums.

Are FHA Loans a Bad Deal?

He prefaced his comment by saying he might upset the lobbyists in Washington, but went ahead and said, “essentially they are ripping off the consumers,” when speaking of the FHA and its pricey premiums and fees.

Yun noted that FHA loans have historically been aimed at first-time home buyers and moderate-income buyers, so charging premiums that he refers to as “outrageous” almost warrants action from the Consumer Financial Protection Bureau (CFPB).

Sure, he was chuckling when he made that last comment, but it’s clear he’s not happy with their new premium structure, and has made it one of his priorities to whittle them back down to more reasonable levels.

The FHA has raised the upfront and annual insurance premiums multiple times over the past several years, mainly because they had no other choice but to raise capital to stay in business.

Additionally, many FHA borrowers now pay annual premiums for the life of the loan, further increasing the costs of homeownership.

That has certainly pushed the FHA loan share down in recent months, with conventional loans snagging a larger share of mortgages these days.

So When Are FHA Loans the Better Option?

In a related report from the Urban Institute, a nonpartisan think tank in D.C., the thinkers determined when FHA loans made more sense than conventional loans, and vice versa.

They assumed a purchase price of $250,000 with a five percent down payment, along with a mortgage rate of 4.29% on a conforming loan and 4% on an FHA loan.

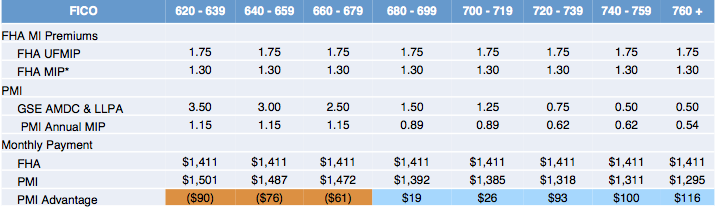

Even with FHA premiums as high as they are today, a borrower with a loan-to-value of 95% would be better off with an FHA loan when their FICO score is below 680, as seen in the chart above.

If their credit score is above 680, they’re better off going the conforming/private mortgage insurance route.

So in that sense, the FHA is still serving that underserved portion of the population, at least with regard to low credit score and lack of a down payment.

Yes, there are borrowers who lack the necessary funds for a large down payment, but have good credit scores, and these people are essentially stuck paying more.

But that’s pretty much the consequence of having standards that were too loose prior to the housing bust. I don’t really see the FHA budging anytime soon.

A recent survey from NAR also indicated that 5.7% of originations were lost because of the higher FHA fees.

For the record, people move mainly to buy a larger home or for a new job (according to Lawrence Yun, grain of salt), and a lot of the panelists seem to think interest rates will be closer to 5% next year.

They also discussed interest-rate lock-in, which again Yun dismissed for the reasons mentioned above. Still, other panelists fear fewer homeowners will be willing or able to list their homes as interest rates rise. But only time will tell.