After the Fed steered mortgage rates lower via quantitative easing, the housing market got the boost it needed to get back on track.

In fact, housing became so cheap that the buy vs. rent argument wasn’t even an argument anymore; buying a home was a no-brainer.

At the same time, the low rates allowed scores of both above-water and underwater homeowners to refinance their existing mortgages, creating a bonanza for banks and lenders nationwide.

So there was a lot of good that came of the low interest rates, but many are now wondering what the consequences will be.

Unfortunately, that refinance boom has since come and gone, and now many would-be buyers are questioning home purchases as well, leaving banks with the dilemma of finding business elsewhere or easing underwriting guidelines.

Both interest rates and home prices are up significantly from 12 months ago, which should give anyone pause who takes the time to think before they act.

I noted a few months ago that the refinance boom was so good that there might not be anything left when it’s all said and done. And I later added that the Fed ruined mortgage rates forever by pushing them beyond historical norms.

The obvious downside is that consumers now see long-term fixed mortgage rates below 5% as the new normal, but can they really remain that low over time?

Rising Interest Rates Have the Ability to Lock Homeowners In

- Do you live in a so-called “locked-in household”

- Whereby the super low mortgage rate you’ve got

- Is forcing you to stay in your property

- And not even consider a move

Another less obvious side effect of the artificially low interest rate environment is that it may influence homeowners to keep their homes longer than they normally would.

You see, if you’ve got a 3.5% 30-year fixed rate (or 2.5% 15-year fixed mortgage), not only would it seem foolish to trade it in for a 5%+ rate, but it could also be difficult to qualify for, especially for a traditional move-up buyer.

How can someone move up if their interest rate jumps a few percentage points and home prices are markedly higher?

Well, if their current home appreciated handsomely, that would solve the down payment issue for the most part. But without an increase in income, the interest rate piece of the equation could be a bit of a roadblock, or at minimum a deterrent.

That’s exactly what a new working paper from the Institute for Housing Studies at DePaul University is concerned about.

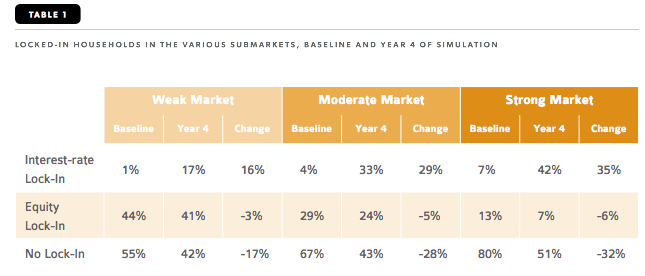

Researchers Patric Hendershott, Jin Man Lee, and James Shilling point out that those who took advantage of the low rates will be reluctant to accept a new mortgage with a higher interest rate, designating them a “locked-in household.”

Do You Fear Losing Your Low Rate? Hope You Love Your Home

- Millions of Americans nationwide have ultra-low fixed mortgage rates

- That they’ll probably never be able to obtain again

- As such they may be reluctant to sell their homes or refinance their mortgages

- This could hurt inventory and throw off the housing ecosystem

They argue that the recent refinancing boom created throngs of these so-called “interest-rate lock-ins,” whereby homeowners won’t sell their homes for fear of losing their low rate.

From 2009-2012, roughly 22 million homeowners refinanced their mortgages.

Combine these homeowners with those stuck with negative or near-negative equity positions and you’ve got a lot of trapped homeowners.

While that might sound good for inventory, thus keeping the supply/demand picture in better shape, it could hurt the overall economy that relies heavily on housing.

With less housing turnover, aka sales, the researchers claim the ongoing housing recovery could be put in jeopardy, along with broader economic gains.

After all, with fewer home sales there is less consumer spending, and if homeowners don’t sell the homes they’ve got, there won’t be as many starter homes available for first-time buyers. This can certainly throw the housing market out of whack.

The last time severe interest-rate lock-in occurred was in the late 1970s and early 1980s, when the 30-year fixed surged from around 10% to nearly 18%.

Clearly the current environment isn’t so severe, but it does make you wonder what will happen once interest rates really begin to rise.

In the meantime I hope you enjoy your home.

I sure as heck am not refinancing anytime soon!