Mortgage Q&A: “Do mortgage inquiries affect credit score?”

When preparing to take out a mortgage, you may have concerns about your credit report being pulled numerous times within a short period of time.

This can occur while shopping for that perfect mortgage with multiple mortgage lenders or mortgage brokers over the span of a few weeks or even months.

But while mortgage inquiries can certainly add up, they won’t necessarily lower your credit score or affect your ability to obtain home loan financing.

It’s Totally Fine to Shop Around for a Mortgage!

- You should definitely shop around for your home loan

- This ensures you explore all options and obtain the lowest rate possible

- Fortunately FICO has an algorithm designed specifically for mortgage inquiries

- Doesn’t penalize mortgage shopping in a specified window of time

The developers of the FICO score know how mortgage shopping works and have adjusted their super secret algorithm accordingly.

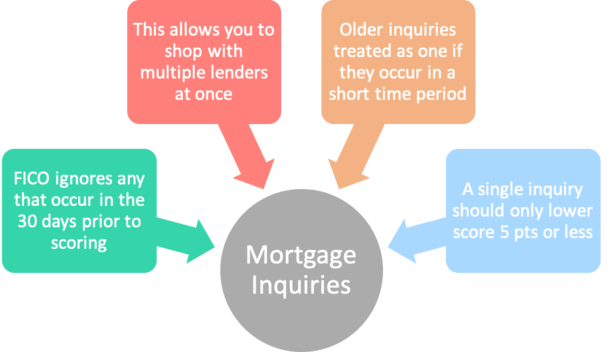

First off, FICO ignores any mortgage inquiries made in the 30-day window prior to scoring, meaning those recent credit pulls shouldn’t adversely affect your credit scores.

For example, if mortgage lender A pulls your credit, then you decide to get quotes and/or pre-approved with mortgage lenders B and C in the same week, they wouldn’t count against you.

This allows to you shop without worry of your credit scores going down each time you do.

Additionally, FICO counts multiple mortgage inquiries in a certain time span as a single inquiry.

The FICO Mortgage Shopping Period

If your mortgage shopping spans a few months, it will look back at older inquiries grouped together in those specified shopping periods and treat them as just one inquiry.

So if you shopped with mortgage lenders A, B, and C in a 14-day period two months ago, but didn’t actually close your loan, then decide to restart the process, those three credit pulls would only count as one.

Unlike a credit card application where you apply just once, a home loan may involve multiple credit pulls with a variety of different lenders.

Instead of making it appear like you’re on a debt rampage, they bundle these similar inquiries into one group if they occur in a designated time period.

Ultimately, you could have your credit pulled by 10 mortgage lenders in a week and it would only count as a single inquiry.

This shopping period can range from 14-45 days, depending on which version of the FICO scoring formula is being used.

The latest FICO version allows a 45 day shopping period, while the oldest just 14 days. Unfortunately, many mortgage lenders use older versions of FICO.

Either way, one credit inquiry will likely only lower your credit score by five points or less, so it may not even be a concern if you already have a solid credit score.

Of course, mortgage inquiries can and will affect consumers differently based on their credit profile, so there’s no absolute rule in terms of impact.

For those with limited and blemished credit history, a mortgage inquiry will probably have a larger, negative impact, while doing very little to affect a consumer with years of solid credit history.

This is yet another reason to strive for the best credit score possible. You might need a little buffer just in case your scores do drop as the result of some hard inquiries.

For example, shoot for a 760 FICO score even if you only need a 740 FICO score to obtain the lowest mortgage rate available.

Do Mortgage Quotes Affect Credit Scores?

- You can request free mortgage quotes from lenders without them pulling credit

- This will have absolutely no effect on your credit scores since you’re only giving them a verbal estimate

- They may tell you that your credit scores could differ but it’s a perfectly fine starting point

- Once you’ve gathered several quotes you can take things a step further and let them run your credit if you wish to move forward

We’ve discussed mortgage inquiries, but what about simple mortgage quotes?

Well, as long as the lender doesn’t actually pull your credit, or uses a service that only results in a soft inquiry, it won’t affect your credit in the slightest.

Assuming you’re just calling around and comparing rates from lender to lender, or broker to broker, your credit will remain untouched.

There’s nothing wrong with just giving these folks a ballpark FICO score and seeing what rates they quote you.

Sure, your actual credit scores may fluctuate if and when you apply, but it’s pretty easy to check your credit for free these days and use that as an estimate.

Your actual scores shouldn’t be too different since these free services come straight from the credit bureaus, so this is a fine alternative to shop without letting lenders dig into your actual credit report and scores.

Once you have a better idea of which mortgage lender you want to move forward with, you can let them pull your actual credit report and lock in pricing.

What If Your Credit Score Goes Down Before Applying for a Mortgage?

- It’s possible to be negatively impacted by a credit inquiry such as a mortgage application

- It can push you below a key credit scoring threshold, such as from 625 to 619

- This could make you ineligible for a home loan or increase your interest rate

- In this case you could ask for an exception or take action to boost your scores

There are cases where a credit score just a few points lower could actually result in a higher mortgage rate, or completely jeopardize your loan application.

For example, a 620 FICO score is the general cutoff for Fannie Mae- and Freddie Mac-backed mortgages.

If for some reason one of your scores dropped from 625 to 619 just as you applied, you could be out of luck.

Assuming you find yourself right below a certain credit scoring threshold, you may be able to use an older credit report if all the information is the same other than the mortgage inquiries.

Or you can ask for an exception from the lender if there’s a clear and compelling reason.

After all, it wouldn’t be fair to penalize you simply for shopping around for the lowest mortgage rate, now would it?

Alternatively, you could take a few quick actions to boost your scores, such as paying off some debt to reduce your credit utilization.

Then look into a rapid rescore. Your loan officer or mortgage broker should have skills in this department to help.

Healthy Credit Habits Are Way More Important Than a Few Mortgage Inquiries

I personally think FICO should expand their shopping period across all versions and make it 100% clear that prospective buyers and existing homeowners won’t be punished for rate shopping.

However, keeping outstanding credit balances low and paying bills on time is far more important than worrying about a few mortgage inquiries.

And your main concern should be securing the best possible mortgage, not fretting about a few points on your credit score.

To avoid unwanted surprises, know all three of your FICO scores before you begin shopping for a mortgage.

Pulling your own credit will not lower your score because you’re not applying for new credit, even if you see an inquiry on your credit report. It’s only visible to you.

As noted, a buffer above what is absolutely necessary can be helpful in the event your scores do take a small hit.

One final note – Do not apply for any other form of credit (credit cards, auto loans, etc) before or during the mortgage shopping process.

Doing so can definitely drag down your credit scores, potentially knocking you out of the running for that mortgage. And may increase your debt-to-income ratio if it involves a new purchase!

Read more: What credit score do you need for a mortgage?

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

Not true on the length of time that mortgage inquires stay on your report. Just talked to Transunion (8/10/2020) and they stated that they stay on for two years. I had 4 mortgage inquires made in two weeks and they are still on my report almost a year later. Someone needs to get their facts straight.

Kenneth,

Yes, all inquiries stay on your credit report for two years, no one has disputed that. But just because they all appear on your credit report doesn’t mean they’re all affecting you. Those 4 are probably only counted as one despite all being documented.

BS. My credit score dropped 34 points with one mortgage application