Mortgage Q&A: “Does refinancing hurt your credit score?”

Everyone seems to be obsessed with their credit scores and what impact certain actions may have on them.

Perhaps the credit bureaus are to blame since they’re constantly urging us to check our scores for any changes.

Let’s cut right to the chase. When it comes to mortgage refinancing, your credit score probably won’t be negatively impacted unless you’re a serial refinancer.

Like anything else, moderation is key here. And the savings could easily outweigh any drop in scores, which will likely be minimal and temporary anyway.

A Mortgage Refinance Will Result in a Credit Pull

- A refinance is treated as a new line of credit (since it’s a new loan!)

- It will also involve a credit report pull (possibly several if you shop around)

- And the closure of the old loan that is being paid off via the transaction

- All three of these actions MAY reduce your credit scores, at least temporarily

When you refinance your home loan, the bank or mortgage lender will pull your credit report and you’ll be hit with a hard credit inquiry as a result.

It’ll stay on your credit report for two years, but only affect your scores for the first 12 months.

What’s more, it will show up on all three credit reports with all three credit bureaus. This includes Equifax, Experian, and TransUnion.

The credit inquiry alone might lower your credit score 5-10 points. But if you’re constantly refinancing and/or applying for other types of new credit, the inquiries could be even more impactful.

As noted, moderation is the name of the game here. If they add up to a point where they’re deemed unhealthy, the credit hit could be larger.

The credit score scientists found out long ago that individuals who apply for a ton of new credit are often more likely to default on their obligations.

But that doesn’t mean you can’t apply for mortgages and other types of credit if and when you feel it’s necessary.

You Could See a Credit Score Ding When Refinancing Your Mortgage

- All 3 of your credit scores may fall temporarily due to a mortgage refinance application

- But the impact is usually quite minimal, perhaps only 5-10 points for most consumers

- And the effects are often fleeting, with score reversals happening in a month or so

- So it’s typically just a temporary credit hit that won’t have any material impact

Because a mortgage refinance is technically a new credit application (it’s a new loan after all), your credit score(s) could see a bit of a ding.

But it probably won’t be anything substantial unless you’ve been applying anywhere and everywhere for new credit.

By a “ding,” I mean a drop of 5-10 points or so. Of course, it’s impossible to say how much your credit score will drop, or if it will at all, because each credit profile is completely unique.

Simply put, those with deeper credit histories will be less affected by any credit harm related to the mortgage refinance inquiry, while those with limited credit history may be see a bigger impact.

Think of throwing a rock in an ocean vs. a pond, respectively. The ripples will be a lot bigger in the pond.

But in either case, the ripple shouldn’t be much of a ripple at all, and nowhere close to say a late payment because it’s not a negative event in and of itself.

It’s more of a soft warning to other creditors that you’re currently seeking new credit.

[What credit score is needed to buy a house?]

You Get a Special Shopping Period for Mortgages

- FICO ignores mortgage-related inquiries made in the 30 days prior to scoring

- And treats similar inquiries made in a short period (14-45 day window) as a single hard inquiry

- Instead of counting multiple inquiries against you for the same loan

- This may help you avoid any negative credit impact related to your mortgage search

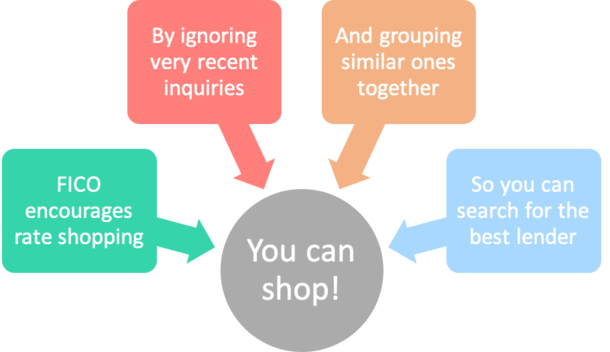

First off, note that when it comes to FICO scores, mortgage-related inquiries less than 30 days old won’t count against you.

And for mortgage inquiries older than 30 days, they may be treated as a single inquiry if multiple ones take place in a small window.

For example, shopping for a refinance in a short period of time (say a month) may result in a large number of credit pulls from different lenders (if you shop around).

But they will only count as one credit hit because the credit bureaus know the routine when it comes to shopping for a mortgage.

And they actually want to promote shopping around, as opposed to scaring borrowers out of it.

After all, if you’re only looking to apply for one home loan, it shouldn’t count against you multiple times, even if your credit report is pulled with multiple lenders.

It’s Different for Other Types of Credit

This differs from shopping for multiple, different credit cards in a short period of time. This could hurt your credit score(s) more because you’re applying for different products with different card issuers.

So someone going nuts trying to open three credit cards in the span of a month could see their scores tank (I’m looking at you credit card churners).

Even if you shop for a mortgage refinance with different lenders, if it’s for the same single purpose, you shouldn’t be hit more than once.

However, note that this shopping period may be as short as 14 days for older versions of FICO and as long as 45 days for newer versions.

If you space out your refinance applications too much you could get dinged twice. Even so, it shouldn’t be too damaging, and certainly not enough to prevent you from shopping different lenders.

The potential savings from a lower mortgage rate should definitely trump any minor credit score impact, which as noted, is short-lived.

The mortgage, on the other hand, could stay with you for the next 30 years!

You Lose the Credit History Once the Old Mortgage Is Paid Off

- When you refinance your mortgage it pays off the old loan

- That account will eventually fall off your credit report (in 10 years)

- And closed accounts are less beneficial than active ones

- But the new account should make up for the lost history on the old account

Another potential negative to refinancing is you lose the credit history benefit of the old mortgage account, as it would be paid off via the new refinance.

So if your prior mortgage had been with you for say 10 years or more, that account would become inactive once you refinanced, which could cost you a few points in the credit department as well.

Remember, older, more established tradelines are your credit score’s best asset. So wiping them all out by replacing them with new lines of credit could do you harm in the short-term.

Additionally, it could affect the average age of all your credit accounts (credit age), which is also seen as a negative.

But the savings associated with the refi should outweigh any potential credit score ding, and as long as you practice healthy credit habits, any negative effect should be minimal.

[Does having a mortgage help your credit score?]

Cash Out Refinance Means More Debt, Possibly a Lower Credit Score

- A cash out refinance could hurt your credit scores even more

- Since you’re taking out a new, bigger loan in the process

- Larger amounts of debt and higher monthly payments naturally increase default risk

- So it’s possible your credit scores may be impacted more if you tap your equity

Also consider the impact of a refinance that results in a larger loan balance, such as a cash-out refinance.

For example, if your current loan balance is $350,000, and you take out an additional $50,000, you’ve now got $400,000 in outstanding debt.

The larger loan balance will increase your credit utilization, and it could result in a higher monthly payment, both of which could push your credit score lower.

In short, the more credit you’ve got outstanding, the greater risk you present to creditors, even if you never actually miss a monthly payment.

Refinance Savings Should Outweigh Any Credit Score Dings

In summary, a refinance should have a compelling enough reason behind it to eclipse any credit score concerns.

Focus on why you’re refinancing your mortgage first before worrying about your credit score.

Ultimately, I’d put it on the no-worry shelf because chances are the refinance won’t lower your credit score much, if at all. And score drops related to new credit typically reverse very quickly.

So even if your credit score fell 20 points post-refi, it would probably gain those points back within a few months as long as you made on-time payments on the new loan.

And most people are only concerned about their credit scores right before applying for a mortgage, so what happens shortly after your home loan funds may not matter much to you.

But to ensure you don’t get denied as a result of a credit score drop, it’s helpful to have a buffer, such as an 800 credit score in case your score does drop a bit while shopping around.

If you’re right on the cusp of a credit scoring threshold and your score dips slightly, you could wind up with a higher interest, or at worst, be denied a mortgage outright.

Read more: When to refinance a home mortgage.

- Soft Jobs Report Takes Pressure Off Mortgage Rates - July 2, 2026

- Kevin Warsh Throws Cold Water on Lower Mortgage Rates - July 1, 2026

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026