A new home loan program is being rolled out this July by Freddie Mac, known as “HomeOne Mortgage,” which features a 3% down payment and no income restrictions.

While Freddie Mac already offers a similar 3% down program via its Home Possible Advantage loan, this new product doesn’t restrict borrower eligibility by income or geography.

To accompany this launch, the existing Home Possible line of mortgages will see their income limits revised (capped) to 100% of area median income (AMI) for all loans other than those in low-census income tracts.

This is being done to better serve low- and moderate-income borrowers via that program.

In other words, HomeOne will be a broader 3% down home loan program, though the underwriting requirements are fairly similar.

Let’s learn more about this exciting new home loan financing option.

Freddie Mac HomeOne Requirements

- Must be an owner-occupied property

- Includes 1-unit single-family residences, condos and townhouses

- Must be a purchase transaction or rate and term refinance (no cash out)

- At least one borrower must be a first-time home buyer

- If all borrowers first-timers, must complete homeownership education

- Max loan-to-value ratio (LTV) of 97%

- Must be a fixed-rate mortgage

- At least one borrower must have a usable credit score

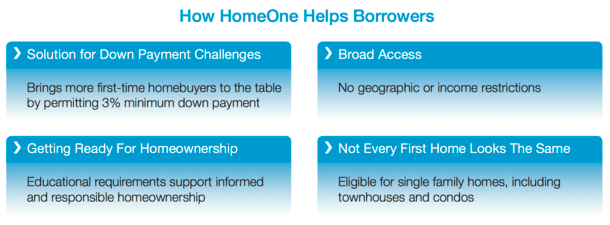

The highlight of the new HomeOne loan program is its 3% minimum down payment, along with the lack of income restrictions. They actually allow a combined loan-to-value (CLTV) of 105% if you use an Affordable Second mortgage to go with it.

But most home buyers will probably be limited to 97% LTV, meaning a 3% down payment will be necessary.

The property must be a primary residence, one you intend to occupy, and it is limited to one-unit single-family residences, or condos and townhouses. No manufactured houses are allowed.

A usable credit score is required, and I suspect the minimum credit score will be 620. This differs from the Home Possible program, which allows an LTV up to 95% without a credit score.

One Borrower Must Be a First-Timer Buyer

- First-time buyers account for nearly half of home purchases

- HomeOne aims to help more of these borrowers achieve their goals

- By eliminating the large down payment generally required

- And no minimum borrower contribution is necessary

The goal of HomeOne is to get more first-time home buyers in the door, literally. As such, at least one borrower must be a first-time home buyer, generally defined as not owning a residential property in the prior three years.

Aside from the relatively easy 3% down payment, my understanding is that no minimum borrower contribution is required. That means gift funds can be used for down payment and closing costs, and no reserves are required.

However, if all borrowers on the loan are first-time buyers, they must participate in a homeownership education course.

Freddie Mac offers a free online program known as CreditSmart, though borrowers may also use other acceptable programs as well.

If you already have a mortgage that is owned or securitized by Freddie Mac, you can also refinance your loan via HomeOne, as long as you don’t take any cash out.

In either case, the loan amount will be maxed out at the conforming loan limit – no so-called super conforming mortgages are permitted.

Additionally, the loan program is limited to fixed-rate mortgages, so no adjustable-rate mortgage options are available. And the maximum loan term is 30 years.

HomeOne will require the borrower to pay private mortgage insurance, and LTVs greater than 95% will require standard coverage of 35%.

Lastly, the mortgage must be automatically underwritten via Freddie Mac’s Loan Product Advisor underwriting system with a Risk Class of “Accept.” No manual underwriting is permitted.

HomeOne Mortgage will officially launch on July 29th, 2018, and income limits for the existing Home Possible programs will also be updated on that day. In the meantime, Fannie Mae already has a similar 3% down loan program available.

- Mortgage Rates Saved by Coolest Inflation Report Since 2020 - July 14, 2026

- Mortgage Rates Look Headed Back to War Time Highs - July 13, 2026

- Despite Headwinds, Odds of a 7% 30-Year Fixed in 2026 Are Super Low - July 9, 2026