Mortgage Q&A: “What is a gift letter?”

A reader recently inquired about mortgage gift letters, so instead of simply answering their question, I figured I’d write an entire post on the subject to help others better understand this topic.

If you’ve been browsing real estate listings lately and have big plans to buy a big house, but your down payment isn’t so big, you might have heard that you can get a gift for the down payment.

You may also opt for a gift simply to get the loan-to-value ratio (LTV) down to 80% to obtain a favorable mortgage interest rate and/or avoid private mortgage insurance on a conventional loan.

The same strategy might help you win a bidding war if the sellers aren’t all that impressed with your 3% down payment.

Whatever the reason, you’ve got options if you have a wealthy donor willing to help you out. But gifting money isn’t without its own requirements.

Gift for Down Payment

- If you don’t have your own down payment funds

- It’s possible to get a gift from a qualified donor

- Such as a family member or domestic partner

- This option is available on many different types of loans, but rules vary

While mortgage loan underwriting requirements vary, most mortgage lenders will allow you to use gift money for a down payment if you’re purchasing an owner-occupied property, one you plan to occupy as your primary residence.

It can also be an option for a second home, such as a vacation property, but won’t be an option for investment properties (non-owner occupied homes).

Additionally, gifts can be used in conjunction with all types of home loans, including conventional (Fannie Mae and Freddie Mac), FHA loans, and jumbo loans.

Both USDA loans and VA loans already allow 100% financing, but gifts may still be provided to cover closing costs, or to cover any shortfall in property valuation.

Along with the down payment, this gift money can be used to cover any closing costs you need to pay out of pocket.

And it can even be used for asset reserves, which when required, ask that you set aside X number of months of PITI mortgage payments to demonstrate your ability to repay the loan.

The takeaway here is that even if you can’t get your hands on a zero down mortgage, you might effectively still be able to buy a home with no down payment if a donor is willing to help you out.

Similarly, those buying their parents house can utilize a gift of equity if they need help in the down payment department.

Minimum Borrower Contribution Sometimes Necessary

- Even if you are using gift funds

- Sometimes you may need to bring in your own money

- To satisfy any minimum borrower contribution

- Which shows the lender you have some skin in the game as well

While it’s often possible to get gift money for the down payment and closing costs, there is sometimes a minimum contribution required from the borrower’s own funds.

For example, if you happen to be purchasing a duplex that you plan to live in, but are only coming up with a 10% down payment (including the gift money), Fannie Mae requires a minimum borrower contribution of 5% from your own funds.

If the home price were $300,000, the borrower would need a least $15,000 from their own bank account, and the gift funds could then complement the borrower’s funds to cover any other costs like down payment, closing costs, and reserves.

One loophole is if the donor has been living with the borrower for the past 12 months, or is from a fiancé or fiancée, then the gift funds can be considered the borrower’s own funds even if they aren’t.

Another way around this is to stick to owner-occupied one-unit properties or put down 20% on the home purchase.

If it’s a second home, you’ll generally need at least 5% of the purchase price to come from your own funds.

Be sure to consider both the acceptability of gift funds and any minimum contribution required by the borrower to check all the boxes.

You Must Use an Acceptable Donor

One important caveat to gift money is that it must come from an acceptable donor, not just anybody willing to give you money.

The acceptable donor list includes the following individuals:

- Spouse

- Parent

- Child (or another dependent)

- Fiancé/fiancée

- Domestic partner

- Anyone related by blood/marriage/adoption or legal guardianship

As you can see, the list is fairly extensive, so you shouldn’t be too limited in who you can receive a gift from. In fact, it can even come from your own child, assuming they’re rolling in dough for some reason.

When it comes to government financing such as USDA loans, VA loans, and FHA loans, the borrower’s employer is also an acceptable source.

As is a labor union, a charitable organization, a government agency that provides homeownership assistance, and even a close friend with a “clearly defined and documented interest in the borrower.”

Conversely, Fannie Mae and Freddie Mac don’t allow gifts from friends and employers, but borrowers may use donated gift or grant funds from churches, municipalities, and nonprofit organizations (excluding credit unions).

Or rely upon employer assistance in the way of a grant or repayable/forgivable second mortgage or unsecured loan.

However, regardless of loan type your donor can’t be an interested party to the transaction, someone who stands to benefit by giving you the gift money.

This includes the home seller, real estate agents, home builders, real estate developers, and so on. Any inducement to purchase is prohibited.

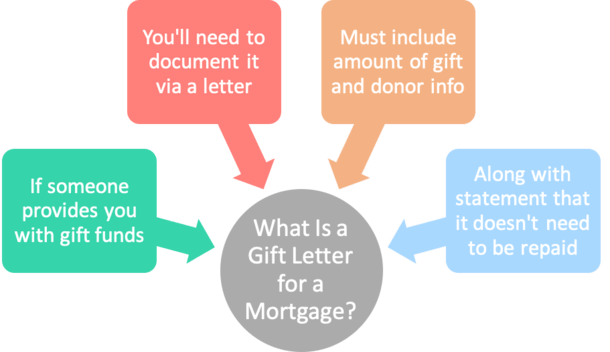

Mortgage Gift Letter Requirements

Assuming you have an acceptable donor and an acceptable property type, and need some assistance in the way of closing funds, you’ll need to procure a “mortgage gift letter” along with any other loan conditions that must be fulfilled.

The good news is that the gift letter is pretty easy to fill out. There are lots of sample gift letter templates on the web, typically provided by mortgage lenders as a courtesy.

You’re also free to ask your loan officer or mortgage broker for guidance, and they’ll probably have a form readily available.

The gift letter must include the following information:

- The dollar amount of the gift

- The date the funds were transferred

- The donor’s contact information

- The donor’s relationship to the borrower

- A statement from the donor that no repayment of the gift is necessary

It’s pretty straightforward. You state that you’re getting a gift along, along with who’s providing said gift, and then provide some pertinent details like contact info, bank account info, and so on.

It’s a Gift, Not a Loan…

- Remember, it’s called a gift

- So that means it is NOT a loan

- In other words, it doesn’t need to be paid back

- If it did, it would have to be included in your liabilities and would reduce your purchasing power

Most importantly, you need to have the donor state that the funds are truly a gift. I don’t think you need me to define the word gift.

Simply put, gifts are given with the expectation that nothing is due in return. In other words, it doesn’t need to be paid back, ever.

This is key because if it is actually a loan, it would count against you in terms of your DTI ratio, limiting how much mortgage you can actually afford.

Once the funds have been transferred to your account, you’ll also need to provide proof of the transaction, which may include a copy of the donor’s check and a deposit slip from your own checking account.

In short, you need to prove that the funds actually came from the donor in question by paper trailing the money.

Otherwise, the lender could question the source. After all, you could say you received a gift but really just took out an unsecured loan or a credit card cash advance.

So both the mortgage gift letter and the proof of funds transfer are key to satisfying this loan condition.

For the record, it’s also possible to receive gift money as a wedding gift and then apply it to your mortgage.

However, you’ll need to furnish a copy of your marriage license, verify the funds in your account, and show that the money was deposited into your account within 60 days of the big day.

In summary, a gift is a great way to increase your purchasing power and/or receive a lower rate on your mortgage, and may even win you a home if there’s competition that has the ability to come in with large down payments.

But like everything else, you have to be diligent and make sure you satisfy all the conditions related to the gift funds to ensure everything runs smoothly.

(photo: Many Wonderful Artists)

- Can You Get a 4% Mortgage Rate Still? - August 10, 2026

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

a gift letter s a joke !!!

when the person that gives you a gift letter is lying

and you are unaware and take it for face value

you are going to get hurt I was sued for the repayment of a gift letter and have found out that there is no agency to report the action too even with all the statements in the letter about no expected repayment The courts do not honor it and call it a real-estate document so too all never except a gift letter

is there any more info on eric’s case? i have a gift letter with a promise of repayment and am now being stiffed.

I believe that Eric is incorrect. A gift letter is exactly that, a gift. A donor of the gift letter cannot seek a benefit or be a “lender” as they would become an “interested” party. The FBI may investigate these white collar crimes as will other federal agencies. State agencies may also investigate such transactions against the “donor” as many states have laws against these type of actions.