With mortgage rates at or near record lows, a lot of existing homeowners are probably asking themselves, “Is refinancing worth it?”

The problem is there’s no absolute right or wrong answer to this question, though with interest rates a lot lower than they were a year or two ago, the answer to this question will often be YES.

Simply put, if there’s a larger spread between your existing mortgage rate and current refinance rates, it’s that much easier to save money.

Conversely, if rates haven’t budged much since you last obtained a home loan, you’re going to have to get knee-deep in the math to ensure it makes sense financially.

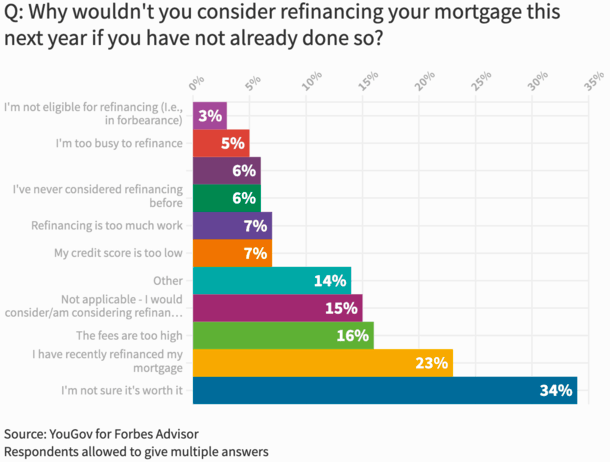

This Is the #1 Reason Homeowners Don’t Refinance

- If you’re questioning whether a refinance is worth it you’re not alone

- It’s actually the top reason why homeowners don’t bother refinancing

- 34% said so in a new survey from YouGov for Forbes Advisor

- But instead of wondering, take action and determine if a refinance can save you money

As noted, lots of homeowners are probably mulling over a mortgage refinance, even those who just refinanced last year, or perhaps even earlier this year.

The top reason they haven’t yet is because they’re not sure it’s worth it, followed by a good chunk saying they just recently refinanced (how soon can I refinance?). Others are concerned about fees, rightfully so.

A mortgage requires work – it isn’t a set it and forget it situation. Since mortgage rates can change tremendously over time, you’ve got to be an active participant.

Or, you can simply say forget it and miss out on substantial savings. But why would you continue to pay a 30-year fixed set at 5% if you could snag a rate in the 2% range or lower?

Just for quick illustration, the monthly mortgage payment on a 30-year fixed set at 5% is $1,610.46 for a $300,000 loan amount.

If you were to refinance that same loan amount down to a 2.75% rate, all of a sudden your monthly payment is $1,224.72.

That’s a savings of roughly $385 per month, which could afford you a pretty nice car every month. Or go toward your retirement savings, or simply boost your emergency fund.

There’s plenty you could do with an extra ~$400 per month, but there aren’t a lot of ways to easily generate those types of savings nearly overnight.

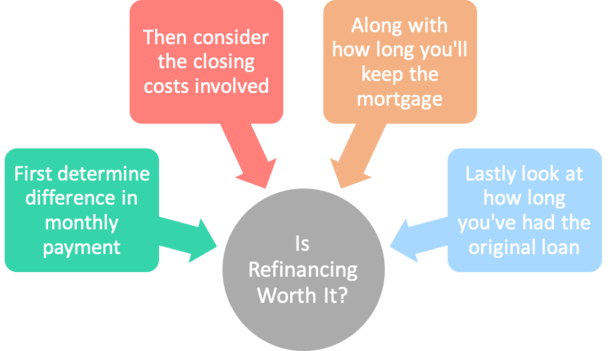

Refinance Savings Can Be Incredible, But Don’t Forget the Closing Costs

- Once you take into account the difference in monthly payment on the old and new loan

- You need to consider the closing costs required to fund your refinance loan

- Along with your expected tenure in the property (and how long you plan to keep the mortgage)

- Also pay attention to loan term to ensure you don’t regretfully reset the clock

Before we get ahead of ourselves, it’s not simple enough to merely compare before and after mortgage payments. I wish it were, but it’s not.

You’ve got a few more things to consider before submitting your refinance application.

One of the biggies is closing costs, which can amount to thousands of dollars. Going back to our example, imagine it costs $8,000 to complete that refinance.

Yes, lots of different parties need to get paid for refinancing your loan, including loan officers, processors, underwriters, appraisers, title and escrow companies, and so on.

All of a sudden, you’re in the hole. The good news is each lower mortgage payment will extinguish that debt, and each payment will pay down more principal since you’ve got a lower interest rate.

So while it may not take long to get back in the black, it could still take a year or two to get there depending on the savings.

And if we’re talking about narrower margins, unlike our example above, it could take 3-5 years to break even on those refinance costs.

That’s why you also have to consider your expected tenure in the property. What happens if you refinance your mortgage, then decide to move a year later?

Well, if you paid a bunch out-of-pocket, you may have lost money, and the refinance actually wasn’t worth it.

The same could be said about a situation where mortgage rates drift even lower, and you find yourself refinancing just six months or a year after your prior refinance.

Is It Worth Refinancing for 0.5% in Rate Savings?

People throw out lots of rules regarding whether a refinance is worth it or not. But it’s hard to apply a blanket rule to thousands of different scenarios.

No two borrowers are the same, whether it’s a different loan amount, credit score, property type, loan type, or financial plan.

Let’s look at an example of a mortgage rate just 0.5% lower than your existing rate.

Does it make sense to refinance to go from a rate of say 7% to 6.5%? Well, it depends on all the inputs.

If we assume a $500,000 loan amount on a 30-year fixed, the difference in payment would be only $166 lower per month.

Once we factor in closing costs of say $2,500, it would take 15 months to break even on the upfront cost.

But what if the closing costs were $5,000? Now it’s 30 months. Will you keep the loan that long? Or the house for that matter?

So closing costs matter, as well as your plan for the property.

Another scenario could be a borrower refinancing out of an ARM into a fixed-rate loan. In this case, it’s about more than just the $166 in monthly savings.

Simply put, it’s important to do the math and not just look up what someone else said is the minimum required for the loan to make sense.

Don’t Spend a Lot on Your Refinance Unless You’re Sure You’ll Keep the Loan

In short, keep your closing costs low unless you absolutely know you’ll keep the refinance loan for a long time.

The good news is there are options to avoid losing money if your plans take an unexpected turn.

I’m referring to a lender credit, where the bank pays all or most of your closing costs in exchange for a slightly higher mortgage rate.

This is how a no cost refinance works, and could be a good compromise for someone who isn’t sure how long they’ll stick with the mortgage/house, but wants to take advantage of the savings on offer.

While your rate may not be the lowest out there, if there’s a sizable margin, you could still make out pretty well.

One last thing to consider is resetting the clock – that is, restarting your loan amortization if you refinance from a 30-year fixed to another 30-year fixed, or to any home loan that extends your aggregate term.

This essentially sets you back in terms of when your mortgage will be paid off, which if it’s a goal of yours, can get in the way of your plans.

The good news, once again, is you always have the option of paying more each month on the refinanced loan.

So if you don’t want to commit to a shorter-term mortgage, such as a 15-year fixed, you can still make 15-year fixed sized payments each month and stay on track.

Of course, some folks are happy to extend their loan term and put their hard-earned money to work elsewhere where it can generate a better return, such as the stock market.

With mortgage interest rates in the 1-2%, it doesn’t take much to beat the market, and a mortgage can be good debt.

As for refinance rules, I don’t buy into them because everyone is so different and your unique situation needs a little more thought than a blanket rule.

Refinancing Pros and Cons

The Good

- Can lower your monthly payment (via lower interest rate)

- Can reduce your total interest expense

- Can shorten your loan term and allow you to pay off the mortgage sooner

- Can put cash in your pocket if you need it for other expenses

- Can pay off other higher-cost debt you may have

- Can allow you to switch loan programs (e.g. ARM to fixed)

The Bad

- Can increase your monthly payment (if taking cash out)

- Can increase your interest expense (longer loan term and/or higher balance)

- Can push out your loan maturity date and take longer to pay off your loan

- Subject to closing costs that can amount to thousands of dollars

- May harm your credit score (at least temporarily but likely minimal)

- Have to go through the lending process (not fun for most people!)

Read more: The Refinance Rule of Thumb

(photo: Quinn Dombrowski)

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

- Mortgage Rates Are Having a Good Day as Oil Prices Fall to Pre-War Levels - June 24, 2026