I’ve already written about it not being the best time to buy a home right now, at least from a pure investment standpoint.

In short, home prices are expensive relative to incomes, mortgage rates have more than doubled, and there’s little quality inventory.

And now we can quantify just how long it takes to break even on a house, per a new analysis from Zillow.

Hint: it’s a long, long time, even if you’re able to muster a big 20% down payment.

So if you’re thinking about buying a home today, prepare to stick around for the long-haul.

How Long to Break Even on a House These Days?

– 3% down payment: 13 years and six months to make a profit.

– 5% down payment: 13 years and three months to make a profit.

– 10% down payment: 12 years and seven months to make a profit.

– 20% down payment: 11 years and three months to make a profit.

A new Zillow analysis tried to determine how long you’d need to own your home before you could sell it for a profit.

This factors in the closing costs associated with the home purchase, the mortgage interest paid, home maintenance costs, and the sales costs once it came time to list the property.

Specifically, they assume 3% closing costs at purchase, 1% home maintenance fees, and 6% in closing costs at the time of sale, along with all that mortgage interest.

In reality, it could be even higher. It’s not unusual for real estate agents to charge 5-6% of the sales price.

So if you’re putting down just 3%, you’re already in the hole, especially once you consider those closing costs as well.

To offset all those expenses, you need to make regular payments to principal each month and hope the property appreciates in value over the years as well.

The rule of thumb says it normally takes about 3-7 years to break even on a home purchase, with perhaps five years the average.

But that number has risen sharply lately thanks to a combination of sky-high asking prices and equally expensive mortgage rates.

How long you ask? Per Zillow, home buyers today can expect to spend approximately 13.5 years in their house before being able to sell at a profit!

In other words, you better really like your house unless you want to sell for a loss, or worse, be forced to do a short sale.

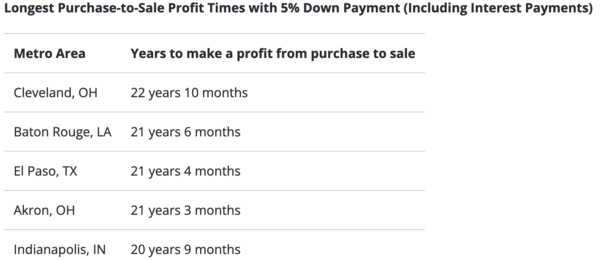

It Takes More Time to Turn a Profit in Affordable Housing Markets

And here’s the irony. It actually takes longer to turn a profit in more affordable housing markets.

Those purchasing a home in places like Cleveland, Baton Rouge, El Paso, Akron, or Indianapolis might need to wait at least 20 years to reach this crucial profit point.

As for why, it’s because of the slower historical growth rate in these more affordable areas.

Without home price appreciation doing most of the heavy lifting, it takes a lot more time to build home equity.

Simply put, principal payments are a lot less impactful than increases in property values, especially on a high-rate mortgage where most of the payment goes toward interest.

It’s the worst in Cleveland, where Zillow says it can take a whopping 22 years and 10 months to turn a profit.

Similar timelines can be seen in the other metros mentioned, meaning it’s not always advisable to buy a home just because it’s cheap.

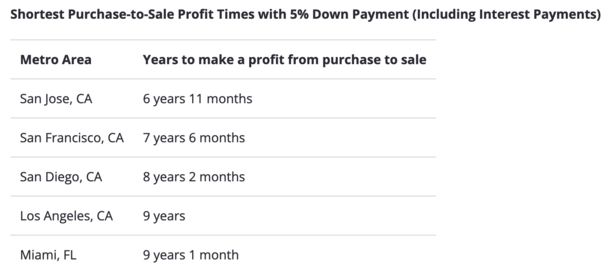

There’s a Faster Road to Profit in Expensive Housing Markets

Again, while seemingly counterintuitive, it’s actually easier to turn a profit if you buy a home in an expensive metro.

Of course, the barrier to entry will likely be higher, but it’s one of those rich get richer stories.

For example, in notoriously expensive Bay Area metros such as San Jose or San Francisco, California, the break-even timeline to profit is a much shorter 7 to 7.5 years.

This is still a long time historically speaking, but it is considerably less than in those “cheap” housing markets.

Similar short purchase-to-sale profit timelines can be found in San Diego, Los Angeles, and Miami.

As you can see, these are highly-sought after cities where demand always tends to be strong, and supply always low. And because of that, home prices are often rising.

But there’s a big barrier to entry, whether it’s the high asking price or the large down payment required.

Either way, this data tells us it might not be the best time to purchase a home at the moment, even if you can muster a 20% down payment.

It could be advantageous to wait for a better combination of lower asking prices, cheaper mortgage rates, and better inventory.

Of course, there are reasons to buy a home other than for the investment. But you still need to be prepared to stick around for a while.

Read more: Pros and cons of renting vs. buying a home

- Can You Get a 4% Mortgage Rate Still? - August 10, 2026

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026