While Fed rate hike forecasts indicate the worst is behind us, mortgage rates are still going up.

In fact, they hit a new 52-week high this morning, surpassing the brief highs seen back in October.

That puts the 30-year fixed at its highest level in more than 20 years, averaging around 7.5%.

This will likely grind the housing market to a halt, which was already grappling with affordability woes prior to this most recent leg up in rates.

The question is why are mortgage rates still increasing if long-term signals indicate that relief is in sight?

The 30-Year Fixed Mortgage Is Now Priced Close to 7.5%

Depending on the data you rely on, the popular 30-year fixed is now averaging roughly 7.5%, up from around 6% to start the year.

If we go back to the start of 2022, this rate was closer to 3.5%, which is a shocking 115% increase in little over a year.

And while mortgage rates in the 1980s were significantly higher, it’s the speed of the increase that has crushed the housing market.

Additionally, the divide between outstanding mortgage rates held by existing homeowners and prevailing market rates has created a mortgage rate lock-in effect.

In short, the higher mortgage rates go, the less incentive there is to sell your home, assuming you need to buy a replacement.

Aside from it being extremely unattractive to trade a 3% mortgage for a rate of 7% or higher, it can be out of reach for many due to sheer unaffordability.

As such, the housing market will likely enter the doldrums if mortgage rates remain at these 20-year highs.

But Isn’t the Fed Done Hiking Rates?

As a quick refresher, the Federal Reserve does not set consumer mortgage rates, but it does make adjustments to its own federal funds rate.

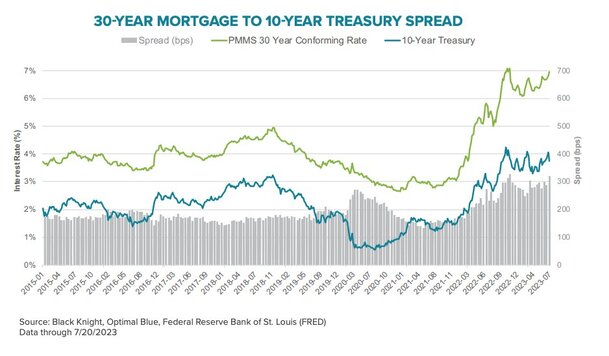

This short-term rate can dictate the direction of longer-term rates, such as 30-year mortgages, which track the 10-year Treasury pretty reliably.

Mortgage-backed securities (MBS) and 10-year bonds attract the same investors because the loans generally last the same amount of time.

Typically, investors get a premium of about 170 basis points (1.70%) when they buy MBS as opposed to government-guaranteed bonds.

Lately, these mortgage spreads have nearly doubled, to over 300 basis points, as seen in Black Knight’s graphic above, thanks to general volatility and an expectation these loans will be refinanced sooner rather than later.

But what’s strange is both the 10-year yield and mortgage rates have continued to rise, despite the Fed’s tightening campaign being seemingly over.

To illustrate, a recent Reuters poll found that the Fed is likely done raising interest rates, “according to a strong majority of economists.”

And we’re talking strong. A 90% majority, or 99 of the 110 economists, polled between August 14-18, believe the federal funds rate will stand pat at its 5.25-5.50% range during the September meeting.

And about 80% of these economists expect no further rate hikes this year, which tells you we’ve already peaked.

Meanwhile, a majority among the 95 economists who have forecasts through mid-2024 believe there will be at least one rate cut by then.

So not only are the Fed rate hikes supposedly done, rate cuts are on the horizon. Wouldn’t that indicate that there’s relief in sight for other interest rates, such as mortgage rates?

Mortgage Rates Need Some Convincing Before They Fall Again

As I wrote last week in my why are mortgage rates so high post, nobody (including the Fed) is convinced that the inflation fight is over.

Yes, we’ve had some decent reports that indicate falling inflation. But declaring victory seems foolish at this juncture.

We haven’t really experienced much pain, as the Fed warned when it began hiking rates in early 2022.

The housing market also remains unfettered, with home prices rising in many areas of the country, already at all-time highs.

So to think it’s job done would appear crazy. Instead, we might see a cautious return to lower rates over a longer period of time.

In other words, these higher mortgage rates might be sticky and hard to shake, instead of a quick return to 5-6%, or lower.

At the same time, the argument for 8% mortgage rates or higher doesn’t seem to make a lot of sense either.

The one caveat is if the Fed does change its mind on rate hikes and resume its inflation fight.

But that would require most economists to be wrong. The other wrinkle is increased Treasury issuance thanks to government spending and concurrent selling of Treasuries by other countries.

This could create a supply glut that lower prices and increases yields. But remember mortgage rates can tighten up considerably versus Treasuries because spreads are double the norm.

To sum things up, I believe mortgage rates took longer than anticipated to reach cycle highs, will stay higher for longer, but likely won’t go much higher from here.

Now that short-term rates seem to have peaked, as the Fed watchers indicate, long-term rates will need to slowly digest that and act accordingly.

In the meantime, we’re going to see even less for-sale inventory hit the market at a time when supply has rarely been lower. This should at least keep home prices afloat.

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

- Mortgage Rates Are Having a Good Day as Oil Prices Fall to Pre-War Levels - June 24, 2026

- You Can Still Get a Sub-6% Mortgage Rate, But Is It Worth It? - June 23, 2026