It’s been tough sledding for mortgage rates over the past month.

They were actually on a roll to start off 2023, falling for the entire month of January before things took a nasty turn.

Without getting too long-winded here, strong economic data pushed rates back toward decade highs.

The culprits were a CPI report and a jobs report, both of which came in hotter than expected.

Those basically derailed the argument that inflation had peaked. Still, you might come across 5% mortgage rates when the news is telling you they’re 7%. Why?

How It’s Still Possible to Offer 5% Mortgage Rates

The latest weekly survey from Fannie Mae put the 30-year fixed at 6.65%, it’s highest level of 2023. And its highest level since November 2022.

Prior to that, 30-year fixed mortgage rates didn’t exceed 7% since April 2002. Yes, it was a good 20-year run folks.

In early February of this year, rates were back below 6%, albeit just barely, but it was still a sign that we had possibly turned a corner.

Then there was the January jobs report, followed by the CPI report in mid-February, which turned rates on their head.

All that progress from November was gone in a flash. Today, you’re probably seeing headlines that say mortgage rates are back at 7% (and above).

But if you do comparison shopping on mortgage websites, you might still come across rates in the 5% range? How? The answer is simple; discount points.

If You Pay More at Closing, You Can Get a Lower Rate

Simply put, lenders that are still advertising mortgage rates in the 5% range (call it 5.99%) are likely tacking on discount points.

These are a form of prepaid interest, and that interest paid upfront at closing means you pay less during the loan term.

Typically, paying points is totally optional, but because of the muddled mortgage market, lenders are often requiring points be paid.

Anyway, those who pay more now can save later. So while the going rate for a 30-year fixed might be 7%, you might still be able to snag a rate in the 5s.

However, you’ll have to pony up some serious cash at the closing table. Or ask for seller concessions to get there.

Often, you’ll need to pay a couple discount points to push your rate down below 6%.

On a hypothetical $500,000 loan amount, we’re talking $10,000 just to cover the points.

You’ll likely have other closing costs to worry about too, such as a loan origination fee, along with third-party fees like title insurance and a home appraisal.

It can get pretty expensive. And worst of all, you might not recoup that money. If you don’t keep the loan long enough, you might not hit the break-even point on those upfront costs.

Low Advertised Mortgage Rates Remind Me of Car Lease Specials

If you’ve ever shopped for a car, specifically an auto lease, you might see a low advertised monthly payment.

For example, $299 to lease X car for 36 months. That sounds awesome and might be much lower than competitors.

But if you read the fine print, you could find that the low payment requires a $3,000 down payment.

All of a sudden, the $299 doesn’t look as appealing. Using simple math, if we add that $3,000 back equally over 36 months, the payment is $382. Then you add the tax and you’re at $400+.

The difference with a mortgage is you can actually save money by paying points upfront. After all, you get a lower interest rate as a result.

And a lower rate results in less interest paid each month. The key is actually keeping the loan long enough, as noted.

But if there’s an expectation these 7% mortgage rates are going to settle back down, you might not want to go all in on that 5.99% rate.

Speaking of, be careful chasing rates below a key threshold. It might be comparatively cheaper to accept the 6.125% rate as opposed to the 5.99% rate.

And the difference in monthly payment negligible.

Shop More When Mortgage Rates Are Higher

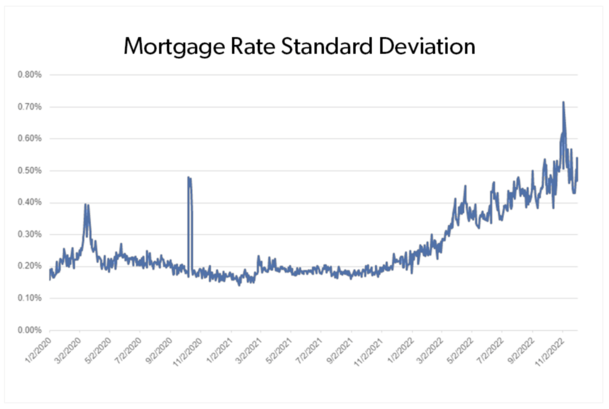

Freddie Mac ran a recent study to track “daily dispersion of mortgage interest rates” over time.

In short, “similar borrowers may receive notably different rates” on the same exact day, based on the lender they spoke with.

By similar borrowers, they mean those with near identical loan scenarios, including same type of loan, same credit score range, property type, loan amount, LTV, etc.

Despite comparable credit risk, average mortgage rate dispersion climbed roughly 50 basis points (0.50%) and surpassed 0.70% in October and November of 2022.

That’s the last time mortgage rates were over 7%. Prior to that time period, the typical mortgage rate dispersion was less than 20 basis points (.20%) from 2010 to 2021. See chart above.

In other words, mortgage rates weren’t much different from one lender to the next. So if you didn’t shop, it may not have mattered.

But in late 2022, dispersion skyrocketed, meaning picking the right lender price-wise was more difficult.

And your chances of landing that better rate correlated with the number of quotes received.

Back in the months of October and November 2022, borrowers who received two rate quotes could have saved up to $600 annually, while those who got 4+ quotes could have saved $1,200+.

Even when mortgage rates were averaging 6%, similar borrowers may have received quotes of 6.5% one day and 5.5% the other, depending on the lender.

Because mortgage rates change daily, gathering quotes over a span of days or even weeks may increase your chances of timing it right.

Sure, you could get lucky on your very first quote. But why leave it to chance?

In short, shop more when mortgage rates are high.

- Can You Get a 4% Mortgage Rate Still? - August 10, 2026

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026