Now that mortgage rates have jumped, it might be time to consider alternatives to the 30-year fixed, such as the once-popular “5/1 ARM.”

Everyone has heard of the 30-year fixed-rate mortgage – it’s far and away the most popular type of mortgage loan out there.

Why? Because it’s the easiest to understand and presents no risk of adjusting during the entire loan term. It’s also fairly cheap, or was…

It’s basically the default home loan option whenever mortgage lenders advertise interest rates, and the pre-selected option when using a mortgage calculator.

But what about the 5/1 ARM? What the heck is that slash doing there!? While it might looks confusing, it’s actually pretty straightforward. And can save you money!

5-Year ARM Quick Facts

- An adjustable-rate mortgage with a fixed interest rate for the first five years

- Interest rate is variable for the remaining 25 years (features a 30-year loan term)

- After five years rate can adjust higher based on index + margin (fully-indexed rate)

- 5/1 ARM means it can adjust once annually beginning in year six

- 5/6 ARM means it can adjust twice each year starting in year six

- Rate caps are in place to limit movement but payments could still become unaffordable

5/1 ARM vs. 30-Year Fixed: An Illustration

Jump to 5/1 ARM topics:

– 5/1 ARM Mortgage Rates

– 5/1 ARM Example

– 5/1 ARMs Will Likely Adjust Higher

– Is a 5/1 ARM a Good Idea?

– Pros and Cons of 5/1 ARMs

– There’s Also a 5/6 ARM

– 5/1 ARM FAQ

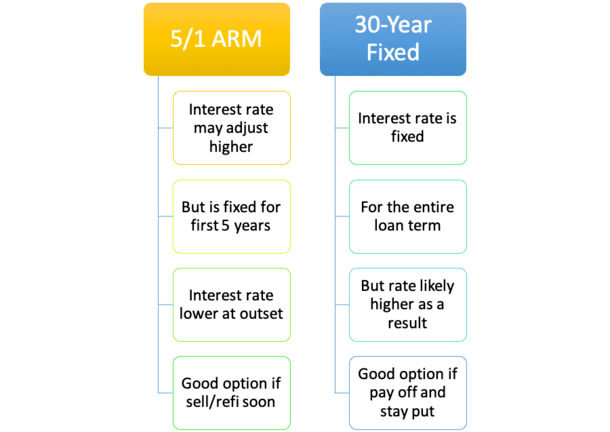

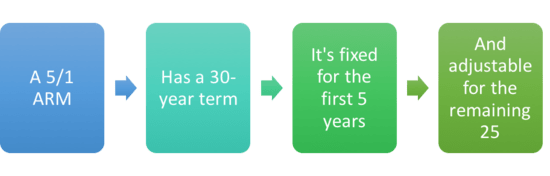

What Is a 5/1 ARM?

- It’s an adjustable-rate mortgage with a 30-year loan term

- The interest rate is fixed (does not change) for the first five years

- And adjustable (the rate can rise or fall) during the remaining 25 years

- It adjusts once each year after the first five years of the loan term

A 5/1 ARM is an adjustable-rate mortgage with a 30-year loan term that has a fixed interest rate for the first five years and an adjustable interest rate for the remaining 25 years.

During years one through five, the interest rate never changes. If it starts at 4%, it remains at 4% for 60 months. Nothing to worry about there.

But after the first five years are up, the interest rate can adjust once annually, either up or down. That’s where the “1” comes in, as in one adjustment per year.

This means it’s a hybrid ARM – partially fixed, and partially adjustable.

Whew! There you have it, the 5/1 ARM broken down into simple terms we can all understand. Oh, and don’t get hung up on that pesky slash.

While not as common as the 30-year fixed, it’s a pretty popular adjustable-rate mortgage product, if not the most popular. And as such, just about all mortgage lenders offer it.

It’s an option for conventional loans, FHA loans, and VA loans (but not USDA loans). So you won’t have any trouble finding it. This should make comparison shopping quite easy too.

5/1 ARM Mortgage Rates Are Lower. That’s the Draw

- 5/1 ARM mortgage rates are cheaper than comparable 30-year fixed rates

- You get a discount because your rate is only fixed for a short period of time

- And it can increase significantly once the loan becomes adjustable

- The interest rate spread might vary from as little as .25% to 1%+ over time

The biggest advantage to the 5/1 ARM is the fact that you get a lower mortgage rate than you would if you opted for a traditional 30-year fixed.

You get a discount because your interest rate isn’t fixed, and is at risk of rising once the initial five-year period comes to an end. Of course, if you refinance your mortgage at that time you can avoid the rate changing.

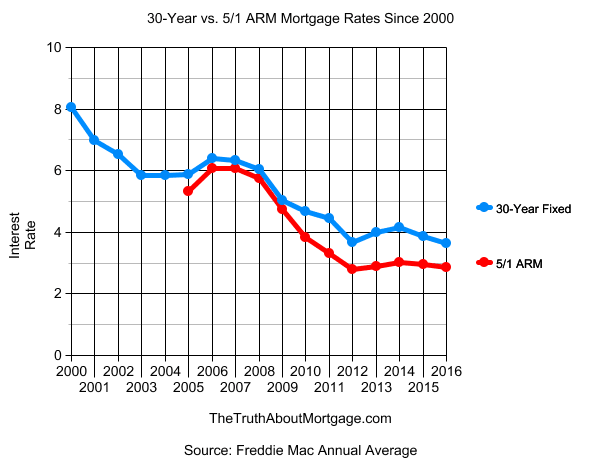

As you can see from the chart I created above, the 5/1 ARM is always cheaper than the 30-year fixed. That’s the trade-off for that lack of mortgage rate stability.

But how much lower are 5/1 ARM rates? Currently, the spread is only about 0.50%, with the 30-year fixed averaging roughly 6.875% and the 5/1 ARM coming in at 6.375%, per my own independent research.

Freddie began tracking the five-year ARM back in 2005, and the spread has been as small as 0.27% and as large as 1.30% in 2011. They stopped tracking the 5/1 ARM in early November 2022.

What’s Low Enough to Consider a 5/1 ARM vs. the 30-Year Fixed?

If the spread between the two loan programs was only 0.25%, it’d be hard to rationalize going with the uncertainty of the ARM.

At .50%, it would depend on the five year plan for the property.

Conversely, if the spread were a full percentage point or higher, it’d be pretty tempting to choose the 5-year ARM and save money for at least 60 months.

Remember, you’d save money via both a lower monthly payment and faster principal pay down. More of each payment would go toward principal with the lower-rate ARM.

Note that my rate assumptions and those of Freddie Mac (before they stopped) only cover conforming loans.

The spread might be a lot different for jumbo loans, depending on market conditions. And a jumbo loan amount can result in a big payment difference, even with slight interest rate adjustments.

Either way, take the time to compare lenders since rates (and loan payments) can vary considerably on ARMs, even more so than more commoditized fixed interest rates.

Let’s look at an example of the potential savings of a 5/1 ARM:

| $300,000 Loan Amount | 5/1 ARM | 30-Year Fixed |

| Mortgage Rate | 6.125% | 6.875% |

| Monthly P&I Payment | $1,822.83 | $1,970.79 |

| Total Cost Over 60 Months | $109,369.80 | $118,247.40 |

| Remaining Balance After 60 Months | $279,590.97 | $282,013.96 |

| Total Savings | $11,300.59 |

Assuming you can snag a 0.75% lower rate on the ARM vs. the fixed product, you could potentially save more than $11,000 over the first five years, not taking into account tax deductions.

That’s a pretty big win, though you do have to consider what happens in month 61. Does the rate (and payment) on the ARM jump significantly at that time, and begin eating into those initial savings?

Or do you have a plan to avoid that, such as a home sale or refinance? As you can see, the savings can be tremendous, but there’s risk involved too as we won’t know where rates will be five years into the future.

This lower-payment mortgage may also free up cash to pay off credit card debt, student loans, an auto loan, or any other higher-APR debt you hold, or for home improvements.

You’d also pay down your mortgage faster because more of each payment would go toward principal as opposed to interest.

So you actually benefit twice. You pay less and your mortgage balance is smaller after five years (more home equity and a higher net worth).

After five years, the outstanding balance would be $279,590.97 versus $282,013.96 on the five-year ARM. That’s another $2,400 or so in savings for a total benefit of more than $11,000.

Discussion over, the ARM wins! Right? Well, there’s just one little problem…

It might not always be this good. In fact, you might only save money for the first five years of your 30-year loan.

After those initial five years are up, you could face an interest rate hike, meaning your 5/1 ARM could go from 6.125% to 8.125% or higher, depending on the associated margin, the rate caps, and the mortgage index.

And most importantly, the adjusted rate may not be affordable, which can lead to a lot of trouble.

5/1 ARMs Are Cheap But May Adjust Higher

- While the start rate on a 5/1 ARM can be enticing versus a 30-year fixed

- Expect the interest rate to be higher in year six and beyond once it adjusts

- ARMs typically adjust higher, not lower once the initial period comes to an end

- But if you only keep it for a short time while it’s fixed it can be a big money-saver

Currently, both ARMs and related mortgage indexes are relatively high, though rates could go even higher if inflation persists or worsens.

This means your ARM could adjust higher once the five years are up. So you should always prepare for a higher interest rate adjustment if you’ve got an ARM.

In fact, during the loan application process mortgage lenders typically qualify you at a higher expected rate to ensure you can make more expensive mortgage payments in the future should your ARM adjust higher.

To that end, qualifying shouldn’t be any easier relative to fixed-rate mortgages as the rate isn’t guaranteed beyond month 60.

That’s also the big risk with the 5/1 ARM. If you don’t plan to sell or refinance before those first five years are up, the 30-year fixed may be the better choice.

Although, if you sell or refinance your mortgage within say seven or eight years, the 5/1 ARM could still make sense given the savings realized during the first five years.

And most people either sell or refinance within 10 years despite taking out fixed loans with 30-year terms.

The big question is where will refinance mortgage rates be when it comes time to make your move? And home prices.

If you came in with a low down payment and home values drop and it’s difficult or impossible to refinance, you could be trapped if you don’t sell your home. That’s the great unknown of going with an ARM – and trying to time the real estate market is nearly impossible.

Is a 5/1 ARM a Good Idea?

- It really depends on what your plan is for the property

- If you know you won’t keep it for five years it could be a no-brainer to save money

- But if you plan on keeping your home for the long-haul and interest rates rise

- There’s a chance it could cost you more money if your rate adjusts significantly higher

If you do decide to go with a 5/1 ARM, or any ARM for that matter, make sure you can actually handle a larger monthly mortgage payment should your rate adjust higher. Paying the mortgage with your credit card isn’t a good strategy.

Also realize that refinancing won’t always be an option; you may not qualify if your credit score goes down or your income takes a hit, or refinance rates may be too expensive to justify a refi. It’s never a guarantee.

If you actually plan to pay off your mortgage, an ARM loan could be a bad idea unless you seriously luck out with rate adjustments. Or you serially refinance before the ARM adjusts and pay extra each month to shorten the amortization period.

Otherwise, there’s a good chance you’ll pay a lot more than you would have had you gone with the 30-year fixed rate mortgage.

Why? Because each time you refinance to another ARM, you’re getting a brand new 30-year term. That means more interest is paid over a longer period of time, even if the rate is lower. If you don’t believe that, grab a mortgage calculator and do the math.

However, if you’re a savvy investor and have a healthy risk-appetite, the 5/1 ARM could mean some serious savings, despite the potential of the rate changing, especially if the extra money is invested somewhere else with a better return for your money.

Just know what you’re getting into first with this loan type and how high the rate can climb during the life of the loan.

Your financial advisor probably won’t recommend it, but that doesn’t mean it’s not a good deal. In reality, a ton of home buyers could probably benefit from an ARM because they don’t hold their mortgages for more than a few years anyway. So why pay more?

Five years not enough for you? Check out the 30-year fixed vs. the 7-year ARM, which provides another two years of interest rate stability compared to the 5/1 ARM. The rate may not be as low, but you’ll get a little more time before that first rate adjustment.

Or go the other way and check out the 3/1 ARM, which gives you two less years of fixed-rate goodness but might come with a slightly lower interest rate.

What Is a 5/6 ARM?

- In recent years many lenders have started offering 5/6 ARMs as well

- They are also ARMs that are fixed for the first five years before becoming adjustable

- But after month 60 they can adjust twice annually instead of just once

- This means once they become adjustable you’ll see an adjustment every six months

Lately, mortgage lenders have been pitching ARMs that adjust every six months instead of annually.

So you may come across a “5/6 ARM” as opposed to a 5/1 ARM, with the former adjusting every six months after the initial five-year fixed period.

It might not matter if you don’t keep your loan beyond month 60, but if you do, you’ll have to contend with two rate adjustments per year for the remaining 25 years.

This could be potentially good or bad, as rates have the ability to move in both directions.

But as you might suspect, rate adjustments tend to go up as opposed to down. Just something to take note of if you see both the 5/6 ARM and 5/1 ARM advertised.

Pros and Cons of 5/1 ARMs

The Good:

- Cheaper than 30-year fixed mortgages

- Interest rate won’t change for a full 60 months

- Rate can adjust lower or not at all

- Might be able to refinance or sell before it adjusts higher

- Could be a good choice if you have bad credit and want a lower rate

- Can switch loan products once you’re more financially fit and have excellent credit

The Potential Bad:

- The interest rate can adjust much higher

- Five years can go by very quickly

- Housing payments may become unaffordable

- No guarantee you can sell your home or refinance before that time

- Might cost you more money vs. taking a slightly higher fixed rate at the outset

- Could actually be harder to qualify depending on what rate is used (fully indexed rate or the note rate)

5/1 ARM FAQ

How much cheaper is the 5/1 ARM vs. the 30-year fixed?

As noted above, it depends on the spread between the two loan programs at the time you apply for a mortgage.

It can be quite minimal, just 0.25%, or more than 1% lower, depending on the interest rate environment and the lender in question. It’s very important to know the spread to determine if it’s worth the risk.

Is the 5/1 ARM due in full in just five years?

No, the five-year part just refers to the amount of time the interest rate is fixed. It’s still a 30-year loan. The rate doesn’t change during the first five years, but is annually adjustable for the remaining 25 years.

Can I get a 5-year mortgage?

I haven’t heard of a home loan with a term as short as five years, but that’s not to say it doesn’t exist, somewhere…

However, you can get a 10-year fixed, or simply pay extra each month to effectively pay off your loan in five years or less, if you wish to do so.

What happens when the first five years are up on my 5/1 ARM?

Your interest rate will become adjustable, based on the lender-assigned margin and the mortgage index it’s tied to.

At that time, you can do nothing and simply accept the new fully-indexed rate (and corresponding monthly payment), or refinance your loan into something new. Some homeowners may sell before the five years are up as well.

Can a 5/1 ARM be refinanced?

Yes, assuming you qualify for the refinance. You can start with an ARM and move into a fixed-rate mortgage later, or go from an ARM to another ARM if you wish.

A 5/1 ARM refinance is really no different than refinancing any other mortgage, it’s just that the interest rate could adjust higher at an inopportune time and a refinance might not be all that attractive.

For example, I know people who took out 5/1 ARMs and kept them too long, at which point the 30-year fixed rose from 3% to 7%.

Granted, they arguably should have refinanced sooner. But this illustrates why you need to keep a close on mortgage rates if you take out an ARM.

Another consideration is you might not always qualify for a mortgage, so if you take out an ARM, be sure you have high confidence that you’ll qualify for a refinance in the future if needed!

Can I get another 5/1 ARM after the first five years are up?

You sure can, again, assuming you qualify. Of course, you have to consider if rates are favorable at that time to do so. Also note that you’ll restart the clock with a fresh 30-year term if you do.

Can you pay off a 5/1 ARM early?

Like any other mortgage, you can pay more than the amount due and whittle down your outstanding balance and loan term.

It could even be a good idea if you want a lower balance at the time your loan is first scheduled to adjust. For example, the smaller balance might make it easier/cheaper to refinance thanks to a lower LTV.

Is this a risky loan program? Should I just stick with a 30-year fixed?

This is an age-old question that can’t be answered universally. For someone who plans to pay off their mortgage in full, a fixed-rate loan might be a better call.

Conversely, if you plan to sell or refinance in a relatively short period of time, the 5/1 ARM can be a real money-saver. The key is having a plan and knowing the risks involved, namely that the rate can increase, sometimes significantly.

What’s the difference between a 5/1 ARM and a 7/1 ARM?

The only difference is the 7/1 ARM is fixed for an additional two years, or 84 months total versus just 60 months for a 5/1 ARM.

While it provides a longer fixed-rate period, the interest rate may be higher on the 7/1 ARM to compensate the lender for taking on added risk.

- Trump Wants Interest Rates Cut to 1%. What Would That Mean for Mortgage Rates? - June 30, 2025

- What the Fannie Mae and Freddie Mac Crypto Order Really Means - June 26, 2025

- Powell Says They’d Still Be Cutting If There Weren’t Tariffs, and Chances Are Mortgage Rates Would Be Lower Too - June 25, 2025

Are these details valid in Canada?

Hi Myrna,

This article applies to 5-year ARMs in the United States.

Hello my name is Edgar, I purchased a home in Lewisville Tx for the price of $225,000 using a hard money lender. The house has been renovated and thinking if will refinance for $300,000 – $315,000. Will you be able run a soft check for both 30 year fixed and 5/1 ARM? Please let me know at your earliest convenience.

Thanks!

Hi Edgar,

I am not a lender. But the difference between 5/1 ARM rates and 30-year fixed rates is quite small at the moment with most banks/lenders.