Mortgage Q&A: “Are closing costs included in a mortgage?”

There seems to be a great deal of confusion when it comes to closing costs and mortgages, so let’s clear the air and make sense of it all.

Simply put, home loans come with closing costs, similar to how most products and services come with associated fees.

No one works for free, even if it doesn’t hit your pocket directly.

The interest alone isn’t enough for lenders to originate mortgages, and a lot of hands are involved, so every party must get paid to participate.

There’s no way around that, but how you pay is certainly up to you.

Typical Closing Costs with a Mortgage

- Lender fees such as admin/underwriting/processing and origination charges

- Third-party costs like home appraisal, home inspection, and notary fee

- Title and escrow fees

- Prepaid items (property taxes, homeowners insurance, HOA dues, etc.)

Closing costs include things like the loan origination fee, mortgage points, credit report fee, home inspection fee, appraisal fee, loan processing fee, application fee, title insurance and escrow fees, and so on.

There’s also the potential for recording fees, courier fees, wire fees, subescrow fees, endorsements, and more.

So it’s clear there are a lot of fees, and based on the number of said fees, the price tag can certainly add up pretty quickly.

This is why it doesn’t make sense to serially refinance your mortgage, just like it doesn’t make sense to buy and sell a home over and over and pay costly real estate agent commissions.

The costs can be quite substantial, and it takes time to recoup those costs via a lower interest rate, assuming you execute a rate and term refinance.

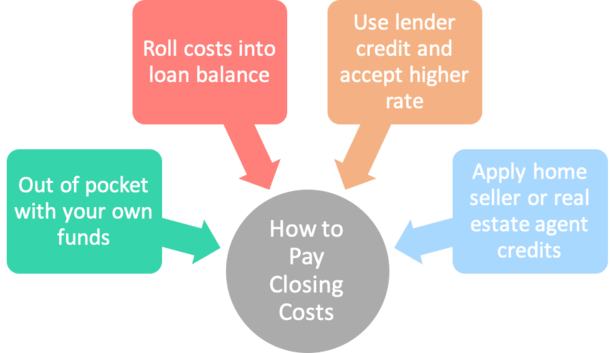

Ways to Pay Mortgage Closing Costs

- Pay them yourself with your own funds at closing

- Use a lender credit to offset some or all the fees

- Use a credit from the home seller or real estate agent to cover fees

- Roll fees into the loan balance and pay down over time with the mortgage

The good news is you’ve got plenty of options when it comes to paying your closing costs.

As seen in the illustration above, there are a variety of different ways to handle the many costs associated with a home loan.

You can pay them yourself, use a credit from the lender and/or real estate agent, or ask for a seller concession in exchange for a slightly higher purchase price.

There’s also the option of rolling the fees into the loan amount, lender permitting.

Be sure to give it some thought before just going with whatever the real estate agent or broker/lender tells you to do.

You Will Pay the Fees in Most Cases

- Regardless of how your home loan in structured

- You will most likely pay closing costs one way or another

- Whether it’s out-of-pocket at closing when the loan funds

- Or indirectly via a high interest rate during the life of the home loan

Ultimately, somebody has to pay all these fees, and unfortunately that someone is you, the borrower/homeowner.

While the fees may certainly vary from lender to lender, or from state to state, the way you pay them is another story.

It could be via a slightly higher negotiated sales price, a larger loan amount, a less attractive mortgage rate, or simply out-of-pocket in cash.

Often, borrowers don’t have the necessary funds to pay these costs, as evidenced by the poor savings habits of most Americans.

This explains why many borrowers choose to kick the can down the road.

One method is to include closing costs in the mortgage, that is, pile them on top of the loan balance so they don’t have any out-of-pocket expenses.

Of course, you’ll wind up with a higher monthly mortgage payment and pay more interest if you roll the closing costs into the mortgage, as the loan amount will be larger, and the costs will be financed throughout the loan term.

Keep in mind that a salesperson may encourage you to roll the fees into the loan balance to make the deal seem sweeter; but in reality, you’re just paying those fees over time at a higher cost.

For the record, this isn’t always an option depending on the type of loan and down payment/loan-to-value ratio.

Remember that when including closing costs in the mortgage, the loan-to-value ratio will increase, as will the loan amount.

This can trigger both a higher interest rate and a larger loan amount you may not be qualified for (or one that exceeds the conforming limit), so tread carefully.

A popular alternative these days is to have the bank or mortgage broker actually pay your closing costs and not include them in the loan balance, though you’ll be stuck with a higher mortgage rate to offset those costs.

This is accomplished via a lender credit. If a borrower chooses or is encouraged to do this, it’s considered a no cost loan, though perhaps no out-of-pocket cost loan would be more accurate.

There is a cost via a higher mortgage rate, which equates to a higher monthly mortgage payment. But it can still make a lot of sense, especially if you don’t keep the mortgage for very long.

Anyway, you can decide if you want to pay the closing costs upfront, take a higher interest rate, or roll them into the loan and pay them down over time.

In the case of a home purchase, the seller may also agree to pay some of the closing costs by offering you a credit, known as a seller concession or interested party contribution (IPC).

Of course, they aren’t really paying, they’re just adjusting the sales price higher and providing a credit.

Your real estate agent may also offer an outright credit if you negotiate with them.

A final way to cover closing costs is via credits for repairs from the seller, which can be applied to closing costs.

Then you can pay for the repairs later via other methods. All the more reason to get a quality home inspection before closing on your purchase.

Decisions, Decisions: To Pay or Not to Pay

- If you think you’ll keep your mortgage for a long time

- It could make a lot of sense to pay closing costs out-of-pocket

- If you believe you’ll sell your home or refinance relatively soon

- Having the lender pay your fees might be a good move

Generally, if you think you’ll hold onto the mortgage for a long duration, paying the closing costs upfront may be wiser than financing them.

If you do so, less interest will be paid because you’ll either have a smaller loan amount or you’ll have a lower interest rate for a long period of time.

Assuming you only hold the loan for a year or two, it could make sense to let the lender cover the fees and take the higher rate because you won’t be subject to that higher monthly payment for very long.

Just try to figure out what your loan timeline might look like beforehand to help guide your choice.

However, if you feel your money could be invested elsewhere at a better return than the interest rate on your mortgage, it may make sense to include the closing costs in the loan.

The same is true for those who receive a credit for closing costs in exchange for a slightly higher interest rate.

You may even be able to get the best of both worlds by shopping your mortgage and finding a lender willing to pay your fees while providing you with a low interest rate relative to the competition.

If you’ve got the money to pay for closing costs, and feel you won’t do any better putting the money elsewhere, it may be wise to pay the closing costs yourself and keep your loan balance and/or interest rate as low as possible.

Of course, some borrowers may have no choice but to go with the other options available, assuming they’re just scraping by in the liquid assets department.

These days, the lender credit is the most popular option for borrowers looking to avoid closing costs, or at least not pay them directly.

Either way, your mortgage broker or loan officer should be on top of this, so don’t fret too much, just take the time to explore all of your options and do the math before you proceed.

Read more: How to reduce closing costs on your mortgage.

- UWM Launches Borrower-Paid Temporary Buydown for Refinances - July 17, 2025

- Firing Jerome Powell Won’t Benefit Mortgage Rates - July 16, 2025

- Here’s How Your Mortgage Payment Can Go Up Even If It’s Not an ARM - July 15, 2025