You’ve probably already heard the claims. That a “biweekly mortgage” can save you thousands of dollars.

And that biweekly mortgage payments can shave years off the life of your loan and help you accrue equity in your home super fast.

Well, it’s true! Pardon the exclamation point. You probably thought I was going to say it was a bunch of baloney like most gimmicks you hear about.

But no, it’s legit, and it’s pretty straightforward too. It’s just basic math, which we’ll get into below.

It’s also fairly easy to set up a biweekly mortgage plan, which requires a payment every two weeks as opposed to every month.

In short, biweekly mortgage payments are a sort of accelerated mortgage payoff system that allow you to make an extra monthly payment each year and in turn save money on interest and pay your mortgage faster.

As noted, the way it works is rather simple.

How Biweekly Mortgage Payments Work

Monthly mortgage payment: $2,000

Total paid annually: $24,000

Biweekly payment (payment made every 2 weeks): $1,000

Total paid annually: $26,000

Result: One extra payment made each year!

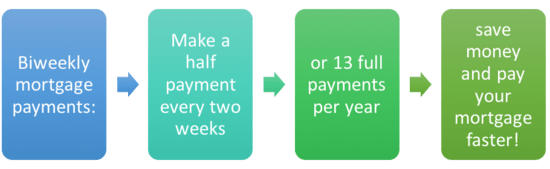

Instead of making a single monthly mortgage payment each month, or 12 payments per year, you make a half mortgage payment every two weeks.

And because there are 52 weeks in a year, that equates to 26 half payments annually, or 13 total monthly mortgage payments.

Let’s pretend you’ve got a 30-year fixed mortgage; if your monthly payment were $2,000 per month, under one of these payment plans you’d pay $1,000 every two weeks.

Instead of paying a total of $24,000 throughout the year, you’d wind up paying $26,000.

That extra $2,000 equates to one payment – and because it is allocated throughout the year, it pays down your mortgage balance earlier than scheduled, which saves you interest and builds home equity sooner.

Put simply, you’ll pay the bank less interest and own your home sooner, if that’s your goal.

This can be especially useful if mortgage rates are high, but less so if you’ve got a rock-bottom rate that isn’t costing you much money.

Of course, it’s not that simple. Nothing ever is. You can’t expect the bank or mortgage lender to allow you to mail in a half payment twice a month, that simply won’t fly.

Instead, you may need to enroll in a biweekly mortgage payment program of some kind.

Your bank or loan servicer (whoever handles your mortgage) will likely ask you to set-up a biweekly payment system with an intermediary, which acts as a liaison between you and your lender.

But these biweekly payment companies can get expensive, especially when they charge a set-up fee of anywhere from $200-$500 and then an additional fee for each transaction.

And at that point, it would start to defeat the intended purpose of saving money!

Fortunately, some banks and credit unions may offer the service in-house for free so you don’t have to worry about the fees.

Always inquire with your loan servicer first before seeking out an outside company. No sense is paying for a service you can get free of charge.

[Check out my early mortgage payoff calculator.]

So what are the benefits of a biweekly mortgage anyway?

– you can increase the amount of equity in your home at a faster rate

– you can save money by paying less interest on your mortgage

– you can reduce the term of your mortgage and own your home sooner

– your mortgage payments are automated and made simple

– more frequent payments decrease the outstanding principal loan balance faster

And the drawbacks…

– you put more of your hard-earned money toward the mortgage each month (and year)

– that money is now locked up in your property

– not everyone actually wants to pay down their mortgage faster (or at all)

– there may be fees associated with a biweekly mortgage program

– you might be better off making a lump sum payment early in the year instead

– you might be able to put your money to use elsewhere if you have a low mortgage rate

So you’ve thought about it and like the benefits a biweekly mortgage affords, but it seems somewhat defeatist to pay someone to help you save money on your mortgage right? Right.

Fortunately, there’s an alternative to do it yourself with a “no cost biweekly mortgage” plan, thereby avoiding those payment processing companies completely.

No Cost Biweekly Mortgage Payments

- You can do biweekly mortgage payments for free too

- Simply add 1/12th of your regular payment to your total mortgage payment

- Doing so could save you a ton of money on interest

- While also shedding years off your home loan!

Forget that fancy name. I just made it up. Here’s how the no cost system works.

Instead of having a biweekly mortgage company handle your monthly payment for a fee, or having to make 26 payments a year.

Simply take your normal monthly mortgage payment, divide it by twelve, and add that amount to your mortgage payment each month.

Then send in your increased monthly payment to the bank or lender. That’s it, you’re done.

They should accept the higher payment and put any additional funds toward the outstanding principal balance automatically.

And that will allow you to pay off your mortgage ahead of schedule. The operative word there is should.

Let’s look at an example of a do-it-yourself biweekly mortgage:

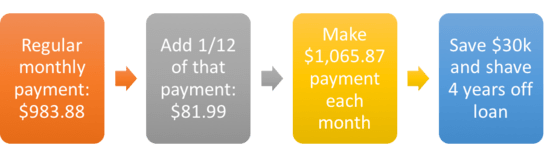

Loan amount: $200,000

Mortgage rate: 4.25% (30-year fixed)

Regular monthly mortgage payment: $983.88

1/12 of that amount: $81.99

New combined payment (paid just once a month): $1,065.87

Total savings: $30,205 in interest

Mortgage term: 309 months (loan paid off more than 4 years early)

Be sure that you note the extra amount is to go toward the principal balance!

If you don’t make this clear, some lenders will return the surplus money, apply it to your next payment, or perhaps apply it your escrow account. It’s important that this is 100% clear so the money goes to the right place.

This free biweekly mortgage method actually works in your favor for several reasons. First, you don’t pay any extra junk fees to have someone do it for you.

And second, because you make an extra payment to principal each month, your loan balance is reduced each month and home equity is accrued faster.

This reduces the total amount of interest due throughout the life of the loan. So you pay less interest in a shorter amount of time. Amazing.

Additionally, it’s easy to execute. You’re still making 12 payments per year, so it doesn’t require any extra work like actual biweekly payments.

Biweekly Mortgage Payments Require Discipline

- The one main drawback to biweekly payments

- Other than putting more money into your home

- Is that they require discipline from the borrower

- Since it’s totally voluntary unlike say a 15-year fixed that requires larger payments

The only drawback to doing it yourself is the old self-discipline issue. Can you trust yourself to make the higher payment each month? Will you remember to do it?

Luckily, these days you can set up automated payments from your checking account for free, so it shouldn’t be too much of a problem either way.

And you have the benefit of backing out at anytime if your financial situation changes for any reason.

You don’t have to nail it down to an exact science either. You can always pay an extra $100, $200, or $300 a month if you’d like. Find a number that works for you and stick to it.

Or make extra payments throughout the year based on your income fluctuations. If you’re determined to pay your mortgage off, every little bit helps. You can even round up your payments.

You don’t need to enroll in a “mortgage acceleration program” or hire a “certified mortgage acceleration specialist” to help you figure out how to make your loan amortize more quickly.

It’s really quite simple. Don’t fall for gags that require you to pay an extraneous set-up fee or a transaction fee every time you make a payment. Your goal is to pay less, not more!

And don’t confuse biweekly mortgages with “bimonthly mortgages.”

A bimonthly mortgage, or semi-monthly mortgage involves no extra payments, just two half payments a month that equate to the typical 12 payments a year.

In effect, the practice does very little if anything to save money, and isn’t offered by many banks and lenders.

Avoid Partial Mortgage Payments!

- Before you implement a biweekly payment plan

- Make sure the lender will accept partial payments

- Or that any extra payments beyond the total amount due

- Go toward the principal balance

One final note: Be careful not to make a “partial mortgage payment” to your mortgage lender as it could result in some unintended consequences.

At worst, the mortgage company may send your payment back if it’s not made in full. This could result in a late fee and a possible credit ding if you don’t make the full payment in time.

In other words, making two half mortgage payments a month probably won’t go well. But you can always call your lender or loan servicer and ask if you can pay your mortgage every two weeks just to be sure.

For the record, mortgages are generally calculated monthly (not daily), so making a half payment early won’t result in any additional savings. And 24 half payments is just 12 full payments, so you won’t do yourself any favors.

Assuming they do hang onto your partial payment, they may place it in a suspense account, where it will remain until enough money comes along to make at least one full payment.

So if you make another partial or full payment after sending the initial partial payment, they’ll only apply the funds if the total is enough to make one full payment.

This is why companies offer biweekly programs to avoid any misunderstanding with your lender if you send in two payments that are supposed to cover your full payment and a surplus toward principal.

When sending a payment that doesn’t correspond with your actual payment due, make sure it’s utterly clear that any additional amount will go toward principal and not escrow (usually you’re given a choice).

That way there’s no confusion about why you’re paying more than the amount due.

If you round up a payment, indicate where you want the excess to go. If the lender/servicer’s website doesn’t make this abundantly clear, call before you pay to ensure your payments will be applied properly.

Lastly, check to see if your monthly housing payment is impounded, where property taxes and homeowners insurance are included.

If so, you’ll want to find just your principal and interest payment for the purposes of calculating a biweekly payment. Any old loan calculator will accomplish that.

Read more: How to pay off the mortgage early.

- UWM Launches Borrower-Paid Temporary Buydown for Refinances - July 17, 2025

- Firing Jerome Powell Won’t Benefit Mortgage Rates - July 16, 2025

- Here’s How Your Mortgage Payment Can Go Up Even If It’s Not an ARM - July 15, 2025

This information is so valuable! thank you! I have one question, though. We just purchased a condo, but we only plan to stay in it for 5 or 6 years and the longest we will keep it for is ten, depending on the resale value. Do you think this method is worth it for us? How can it benefit us as short term owners, who also would like to profit of the property as much as possible?

Thank you!

Tiffany,

Making extra (or larger) payments reduces the outstanding loan balance quicker, and as that balance decreases less interest is charged over time. So when it comes time to sell, even if just after 5-10 years, the difference between the eventual sales price and the outstanding loan amount will be greater than if you just stuck to standard monthly payments.

But would it be a significant amount compared to if we just saved the extra money (we’ll say $100) rather than putting it towards the mortgage? Or do you think it would be about the same?

I’m just having trouble wrapping my head around the numbers. I will try and find a calculator online for it.

Thank you!

Tiffany,

An early payoff calculator will show you the benefits…and it’s really personal preference to put more or less toward the mortgage.

Colin,

Hello! Would you be able to tell me if some banks will actually amortize your biweekly payments biweekly or if they just hold on to the money and make a payment once a month. I’m assuming it would be more advantageous to the borrower if the biweekly payment can also be amortized biweekly. Do you know of any banks that offer this? I just got out of the military and I’m planning to use my VA home loan soon and would like to make good decisions as I make the investment. Thanks for your help Colin!!!

Hey Wade,

It would be more advantageous because earlier payments would knock out interest earlier and reduce future interest expense, but I doubt any banks would apply your biweekly payments that way because traditional mortgages don’t receive any (interest) benefit from paying earlier in the month.

Hey Colin ,

Just tagging onto the response you answered for Wade,

What would you suggest in my case . If i want to pay less on interest and save ~$100k on interest for the life of my 30yr loan of $327k. should i then do biweekly payments on my own? or should i do what you suggested and just add the extra 200+ bucks on my monthly payments ?

I guess i’m just trying to figure out how i can ” avoid ” paying the full amount on interest and pay less since i’m paying more frequently ?

Samuel,

Just input your numbers in an early payoff calculator to see how much extra you need to pay monthly to save $100k on your particular loan. Not sure biweekly will shave that much off, might need to be an extra monthly amount.

Great article, I just bought a house and was checking to see if I would need to setup a bi-weekly payment program or just add to my monthly payment and you pretty much answered it. So to be clear I have a mortgage total of 1100 a month, if I add roughly 95 a month to my payment I will get the same benefit as a bi-weekly payment program? Typically in bi-weekly payment programs do you pay a little more per payment, I always understood them to be your typical monthly payment split in half. thanks again

Bill,

A true biweekly is your regular monthly payment split in two every two weeks, aka 26 half payments, 13 full payments. Doing it yourself requires higher payments but can generate the same effect without any fees to setup a biweekly program.

ahh the bi weekly ends up 26 payments/13 months vs 12 monthly with a little extra.. comes out a wash except no bi-weekly setup fees. Thanks! You just saved me several hundred dollars!

I”ve been considering refinancing my remaining balance of 75000, originally over 87000. The loan was for 4.75%. I am enrolled in a biweekly payment plan through WF Bank. If I choose to send extra payments each month, does it matter when I send it? Would it be preferable to send it at the beginning of the month or at the end of the month. My credit rating is excellent, above 800, and I don’t have any revolving CC debt. What would be your recommendation for my best course of action?

Jose,

It depends when they actually apply the payments. Generally it doesn’t matter when you send in a mortgage payment because interest is calculated monthly, but if WF applies it right when they receive it, payments made earlier could save money. Might be best to give them a call and ask.

Thanks for this info. We set up a bi-monthly payment with our mortgage company and saw this “suspense account” thing (much to our chagrin, obviously)

Thanks to your info, we aren’t going to waste our efforts and money

When calculating the amount for the “No Cost Biweekly Mortgage” payment, do you take the payment before escrow or including escrow?

Jenn,

The amount that goes toward insurance/taxes should be fixed (since you can’t pay extra there) so you’d want to focus on the principal/interest portion.

If you were to calculate the bi-weekly payment with just the principal and interest portion, you would be short on your monthly payment amount.

Let’s say you total payment, which includes escrow, is $1000. Prinicpal and interest, for simplicity, is $800. You need to do $500 bi-weekly payments. If you only focused on the interest and principal portion, you’d be short $200.

This helped me out tremendously! I was going to pay $108 extra toward my principal per month AND do bi-monthly. Seems it isn’t necessary. I could save about $28,000 alone and cut my mortgage 9yrs just with the extra little bit. Whew!

Find a mortgage company that will still do bi-weekly. The banks are wise to this process.

As a matter of fact, when you send in the first payment it is put into a “suspension” account, no interest and no credit to your mortgage until the second payment comes in….they have your money for their use…..

Amazing……

so sending half paymentrs isnt allowed unless you enrolled?

Peter,

I doubt your lender/loan servicer will accept half payments, but you should check with them directly to be certain.

Which are the banks that actually offer this facility ?

I checked with Chase and WF and they both don’t offer it

Raj,

I think more banks used to offer it in the past but fewer today.

I set up a bi-weekly mortgage program with my home loan and an extra thirty dollar a month principal only payment as well, but I see no reflection in the loan when I look on the amortization schedule printout. It doesn’t reflect any years off the loan or savings . Could it be a mistake on the banks part?

Kelly,

Could be that the $30 isn’t enough to reduce the loan term by a year or the lender simply didn’t update your loan schedule. Probably best to ask them directly.

So if i make a payment every 2 weeks, would equal one extra payment a year. So why is the mortgage company suspending it each month. I’m ahead not behind. Is there law on this?

Wayne

Wayne,

You have to make sure the mortgage company (loan servicer) will accept partial payments, otherwise they may reject them. Or ask if they can setup your account to accept biweekly mortgage payments so they are processed properly.

Thanks this information is really helpful. Another strategy is to get an amortization statement of your mortgage, and send in a extra principal payment along with the regular mortgage or if it is on auto pay, mail in the extra payment to be “applied to principal”…for each pay you do that way will eliminate the interest for that month. It is a little tedious because you have to follow the amortization statement precisely. You don’t have to do it all the time, but doing that couple with the strategy that Colin provide really bring it down. However, this plan works best in the early stages of the mortgage because the principal starts to increase the older the mortgage.

I’ve read many different strategies for reducing your mortgage but if I send in my mortgage payments early by the 15th of each month. Would that equate to the same savings in interest and reduced payments?

Rod,

Generally, payments received on the 15th of the month or earlier go toward the previous month’s payment. If paid on the 16th or later will go toward following month. However, most mortgages don’t reward paying early in the month (on say the 16th) because they’re based on monthly interest, not daily. So if payment is due on the 1st of every month, and you pay two weeks early on the 16th, nothing would change (no savings) versus paying on the 31st or even up until the 15th of the following month.

Conversely, a simple-interest mortgage accrues interest daily, so paying early in the month would save money, but most people don’t have simple-interest mortgages.

Can you suggest a reliable Bi Saver company?

Douglas,

Some lenders/servicers will give you the option for a small fee or for free…or as illustrated, you can setup your own free version to avoid any costs.

Colin,

Thank you so much for this article, the information you provide is great. Some years back we had what was considered to be a TRUE Bi-Weekly mortgage payment option, which not only allowed us to pay 26 half payments, but also had no initial set-up fee or extra service charges. What is the difference, well as I came to understand it, is that if a mortgage company received half of your payment 15 days early, they wouldn’t just sit on it and wait for the 2nd half to come on the original due date and then post it. Instead they would post the half payment within a day or so of receiving it. So what that means is not only was I making a 13th full payment each year, but I was saving 2 weeks of interests for 12 (2 weeks early) payments (not 13 or 14 because payments 25 & 26 are principle only anyways). So my question is, yes there is one, where can I find a bank that actually does True Bi Weekly?

Brian,

Not sure many banks offer what you’ve explained, though I understand what you’re saying. It seemed to be more popular back in the day. Perhaps local credit unions offer it, but the big banks certainly don’t advertise it. I’ll dig around and see if I can find any programs from the major banks.

How long will it take for me pay off a 30 year mortgage if I pick up the twice a month mortgage after paying for 20 years?

Merteen,

It probably won’t have much effect if you’ve already been paying it for 20 years, but you can use my early payoff calculator to see.

Against the potential for ROTH IRA growth surpassing potentially 13%+/yr, it seems that taking the potential hit of interest is worth it…..hmmmmmmmm

I have been paying my mortgage and HEL bi-weekly, but my balances do not match a bi-weekly calculator, because the calculator applies the principal and interest on the transaction date, but the mortgage company keeps the first bi-weekly payment in suspense. This results in the normal monthly payment amount being applied, then the extra that I include being applied. I have an interest bearing checking account. I think I’d be better off making the monthly payment along with 1/12th of a monthly payment (which will add the extra payment per year), plus any extra amount towards principal. This would keep money in my interest bearing account instead of sitting in their suspense account. Thoughts?

Clint,

That’s the problem with partial payments (they typically can’t be applied until the full amount is there) and bolsters the argument to add 1/12th of the standard payment each month to ensure a full payment plus excess is applied ASAP. Can always call the servicer and ask what other options you’ve got, or if they can set up free biweekly option.

I’ve read everything I could find on this topic & am confident that I understand the ins & outs of bi-week, monthly & 1/12th payments.

My question is are there any banks, mortgage brokers, lenders, etc., that offer a mortgage product with either semi-monthly (i.e., 24 payments / yr) or bi-weekly (i.e., 26 payments / year) payment terms?

Based on your previous answers there is not, but I am hoping one exists. Reason being I used a Mortgage Amortization Schedule calculator and was shocked at the difference the frequency made. On a $250,000 loan semi-monthly payments cut a 30 yr term in half and bi-weekly payments shave off just shy of $100K in interest & the pay off is 14 years!!

Follow up question: if there really are none, do you have a theory as to why?

Thanks!!

Liz,

Some companies allow you to sign up for biweekly payments, but you need to reach out to them to see if it’s offered and to get it set up. And sometimes there might be a fee.