If you recently took out a mortgage, or have been thinking about purchasing real estate, you may be wondering when your mortgage payments will be due each month, among other things (like how late Ikea is open).

Well, mortgage payments are generally due on the first of the month, every month, until the loan reaches maturity, or until you sell the property.

So it doesn’t actually matter when your mortgage funds – if you close on the 5th of the month or the 15th, the pesky mortgage is still due on the first.

The only difference is when the first mortgage payment is due, which I’ve explained in my when mortgage payments start post.

Mortgage Due on the 1st, Late on the 16th?

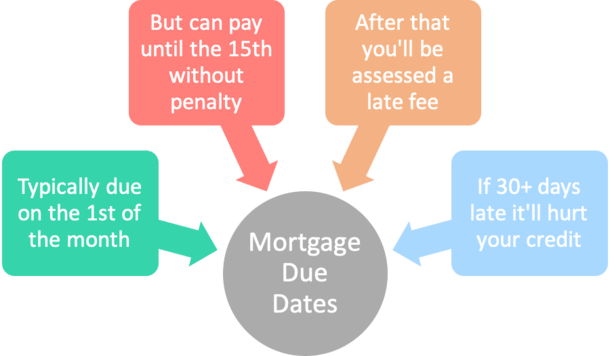

- Mortgages are typically due on the first of the month

- But mortgage lenders generally provide a grace period

- Of up to 15 days to pay without any fee or penalty

- Meaning it’s only late if paid after the 15th of the month

Most people probably know that mortgage payments are due on the 1st of the month, but many loan servicers (those who collect your payments) will allow you to pay 15 days “late” each month.

So even though your mortgage payments are technically due on the first each month, you can pay as late as the 15th every month without any kind of penalty.

No late fees, no credit report dings, no issues whatsoever.

This is known as the “mortgage grace period,” similar to other grace periods you see with all types of other loans.

Some “savvy” consumers may even set up automatic payments to be sent mid-month, instead of paying on the first to maximize their cash flow.

But this can be a dangerous game, especially if your mortgage payment doesn’t make it to the servicer on time, for whatever reason.

Nowadays, this may be less of a problem thanks to speedy and generally reliable online payments, but it’s still a risk not worth taking.

The loan servicer may also harass you if you consistently pay late into the grace period.

What If I Pay My Mortgage Late?

- As noted, you get a generous grace period of 15 days in most cases

- If still late after that you’ll be assessed a late fee, which can vary by lender

- Usually a small percentage of the monthly P&I payment

- Only counts as a delinquency on your credit report if 30+ days late

As seen in the Closing Disclosure (CD) screenshot above, payments are typically only considered late if they’re more than 15 days late.

Check your own paperwork (on page 4 of the CD) to see if the same terms apply to your home loan.

Just note that if you play this “pay at the last minute game” each month, you could eventually get burned and wind up paying a mortgage late fee.

These fees can vary, but are often pretty steep. We’re not talking a $20 late fee and a slap on the wrist.

We’re talking a percentage of the mortgage payment, such as 5%. So if your monthly mortgage payment is $3,000 a month, that’s $150 smackers.

And if you wait too long to make a payment, typically 30+ days beyond the due date, it could eventually be reported to the credit bureaus as a late payment, which will really hurt.

The result could be a substantial credit score ding, and greater difficulty obtaining subsequent mortgages in the future, a major issue if you need/want to refinance your home loan for some reason.

Or if you want to buy more real estate in the near future.

After all, lenders aren’t too fond of homeowners who don’t make their mortgage payments on time.

What If I Pay My Mortgage Before the Due Date?

- In most cases there’s no benefit to paying the mortgage before the due date

- Because they’re calculated monthly using simple interest

- Meaning you won’t save money or lose money on interest

- So it shouldn’t matter if you pay on the 1st or the 15th, as long as the payment is made on time

Okay, so we know paying late isn’t too smart, but what about paying the mortgage before the due date?

You might be thinking, “Hey, I can save money on interest if I make my payments on the 20th or 25th of each month, instead of the first of the next month.”

Not the case. Your loan servicer may accept payment on that date, but it won’t mean you’ll pay less interest.

The interest is already figured out for the month using the previous month’s balance, so it doesn’t matter if you pay a few days early.

This differs from credit cards and other types of loans, such as HELOCs, where the interest is calculated daily.

If you actually want to pay less in interest on a traditional mortgage, you need to make extra payments to principal.

So if you pay an additional $100 on top of your monthly mortgage payment, your loan balance will be $100 lower for the subsequent month, and that means less interest paid over the life of the loan.

This will also reduce the loan term, meaning your mortgage will be paid off in less time.

Just note that the monthly mortgage payment will stay the same, regardless of whether you make larger payments for a few months here and there.

Tip: Be careful when making extra principal payments. If you send in a payment that is below the monthly mortgage payment, such as two smaller biweekly payments, even if they exceed the total amount due, they may not be credited properly.

How to Make Mortgage Payments

Lastly, let’s talk about how to make a mortgage payment to your loan servicer.

First things first, note that I said loan servicer, not lender or broker or any other entity.

The “loan servicer” is the company that actually collects your mortgage payment each month, and may not be the individual or company that originated your loan.

So pay close attention to who this is, and note that mortgage loans are often transferred from one servicer to another, especially shortly after closing.

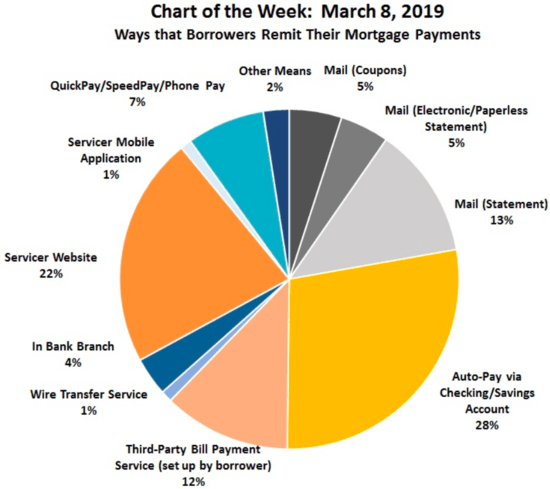

In terms of paying, we see from the graphic above (from the Mortgage Bankers Association) that lists the most common ways to pay a mortgage.

The top three are auto-pay, via the servicer website, and by mail.

Less common ways are in-branch, wire transfer, phone pay, and other means, which probably includes paying the mortgage with a credit card.

In summary, speak with your loan servicer once you take out your mortgage to ensure your payments are processed properly. Rules vary and it’s best to get all the answers straight from the horse’s mouth.

(photo: adactio)

I wish people would look at this! Working for a mortgage company people do not understand this concept! Thank you for the information!

Chase will post all money above payments for that calendar month as principal. Bank of America seem to post all extra money as the next months payment unless specified otherwise as principal.

Having an early due date like the 1st or 2nd and banking with Chase can be tricky paying your mortgage payments around a weekly pay period. If your payment gets there on the 31st (intended for the 1st), bam, you just posted a principal-only payment and you now owe another mortgage payment the next day, or risk foreclosure proceedings to start in 30 days.

Randall,

Thanks for sharing that info. The takeaway is that you need to know your lender’s policy to avoid any missteps. And it’s usually wise to notify your lender if any extra payment should go toward principal.

I was with the understanding that due on the first meant it is due on the first but the lender or department store must allow 15 days before it is marked late….. I just got off the phone with Kohls and I have a late fee of 35.00 every month for the past 5 months….. I pay all my bill on the first week of the month and never had much of a problem…. Kohls is just making this because they can get extra money for nothing….

I spend a couple of hundred dollars every other month at Kohls… NO More, their loss…. I need to find what the government rules are… do you know the site I should go too… hope so Roger Fossette

Conversely, can a lender subsequently change the payment date without informing a customer in writing? If they do not inform the customer in writing what steps can the customer take?

Philip,

I would assume they would have to let you know, but I don’t know their terms or why they would change your payment due date.

My wife is a school teacher, no income over the summer. We pay the summer months mortgage payments ahead (conventional escrowed month to month mortgage.). I realize that there is no benefit by paying early (paying for June, July, August and September’s payments in May, but if I pay additional principle with each of these payments (+$50 with each mortgage pmt) will the additional principal added to the mortgage payment be applied to the principal balance due as of May when the payments are sent in or when each of the actual payments is actually due?

Also, let’s say as of May 1, 2015 I have paid my mortgage up to September 2015. I decide on July 1, 2015 to make a principal only payment of $500. Will that principal payment be applied as of the date rec’d (in July) or will it be applied when my next mortgage payment is actually due, October 1, 2015, because I paid ahead?

Ronnie,

No point in speculating – best to ask your servicer directly how payments will be applied. The extra principal payments are better served by being applied as soon as possible to lower interest expense in subsequent months.

We sent in our first mortgage payment which is due on the 1st of the month. How long typically will it take for your lender/bank to cash your mortgage payment? the First payment had to be mailed in. Should I expect to see the withdrawal by the middle of the month?

Chris,

It depends on the bank really. But it generally shouldn’t take more than a few business days after sending it.

Thank you for the information here on “late” payments. I had looked into my loan paperwork for my mortgage and it says that I will be charged at late fee after 15 days. My question is if I pay my mortgage 6 days after its due date once will there be a mark on my credit report for it?

Dave,

Late payments don’t generally show up on credit reports until you’re 30+ days late…

My mortgage is with WF and as indicated in previous posts my mortgage is due on the 1st of every month and as shown on the statements received the latest I can pay my mortgage is the 16th of the month before being penalized with a late payment fee. (This is my first encounter on being late thus, my biggest concern is the affect it may have on my credit) I just ran into emergency expenses this month thus, I cannot make a payment on the 16th but will have funds 2-3 days after. Will paying my mortgage then drastically affect me?

Ella,

Generally paying a few days late won’t result in any credit hit (usually this takes place only after being 30 days late), but you’ll probably be subject to a late fee. It’s still good practice to pay before the grace period ends to avoid any uncertainty.

My one question is “why are mortgages as a financial tool, not covered by federal guidelines whereas all lending institutions must adhere to common practices.

Thanks

Art

Art,

There are federal guidelines in place now with the Ability to Pay and Qualified Mortgage rules.

Bank of America policy can not be paid more then thirty days in advance . Just got off phone with them I have always paid a month in advance well in sept a check arrived to early which made it 32 days advanced so they applied to principal then sent statement requesting two months payments for dec and jan with a 65.00 late fee.

I phoned had them apply to payment and not a extra principal payment as indicated on the coupon

Now they removed the late fee and the next pmt is due February one !

I think since the coupon clearly stated to apply to payment and the month , this is a tricky way to punish a person for paying early an adding bogus late fees ! I did get it corrected but fail to understand there math !

I really feel like they tried to pull a scam !

My husband has a home. We had to get a second mortgage because taxes, how can we change banks and have them mortgage our home, also since we got married over a year ago they won’t put my name on his house why and does my credit matter. Thanks, Debbie B

Debbie,

There’s a difference between being put on title vs. being put on the loan. If the loan is already closed you can’t be added unless you refinance the loan. A quit claim deed can get you on title.

I will pay off my mortgage next month. I still owe $4,700.00, but the Chase bank teller tells me that by April’16 I will have to pay $4,800.00 to finish paying it off. I have been paying for 20 years, so that’s 10 years early. After paying all that interest I will still owe more for paying it early? I’m confused how they came-up with that amount. Anyone have any idea how they came-out with that figure?

Marc,

Perhaps interest accrued during the month that is paid in arrears.

SWBC Mortgage generated a statement 29 January 2016. Due date is 1 Feb 2016. I received the statement 6 Feb 2016 via USPS at my home address.

This has been a common problem for 3 months and, as well, i tick the address change box, noting the post box address but nothing changes.

I called but they insist I tell them on the phone my full SS #. …which I am not willing to do. what is going on here?

thanks.

Wayne,

Not sure what you’re trying to do…change your mailing address or receive your statement earlier? In any case, you’ll have to figure out how to verify your identity with the company so you can make the required changes. Perhaps they can verify in a way other than asking for your Social.

I pay on the 16th, online, and pay an extra $100. toward principal. However, I noticed on my statement that they only credit $97. to principal and the rest to current payment. Why is that?

Jean,

Not sure, probably best to ask the servicer directly.

I have a question. Can my bank post my mortgage payment on the next business day and charge late fees, even though they got is on the due date?? It was paid at 3:37 PM after checking/savings accounts will not post. But this is a bill payment????

Tanya,

That’s probably up to your bank and whatever their policy is. This is why it’s good to leave a buffer of a few days in case the payment processing time takes longer than expected. Maybe you can ask them to waive the fee in good faith as a courtesy.

hello! I have a question. if I pay my mortgage payment 6 days after my due date, are they gonna charge me a late fee for a every single day that im late or just the 35 late fee..?

Brenda,

Well, there’s usually a grace period, so it’s technically due on the 1st, but you can typically pay “late” until the 15th. After that you might be looking at a flat, one-time late fee, and if it goes too long (over 30 days) you get into more trouble with a late on your credit report. Best to call your actual loan servicer directly to inquire about late fees and when they’re assessed.

Now last month my bank (bb&t) just give me a late change for something that happen in 2011. Is that legal?

They took over my mortgage in 2015

Christine,

Hmm, you may want to check with them directly to clear that up…seems odd.

Thanks for the helpful advice, Colin!

I bill pay my mortgage payment. The bank electronically makes the payment. The bank processed and confirmed payment on the 16th, but mortgage company posted payment on the 17th (1 day late and $95 fee). According to the banks policy, it processes payments at 12:00 AM and 10:00 AM PST. According to the mortgage company, payment must be received no later than 5:00 PM PST.

My math says that the money was transferred either 17 hours or 7 hours before the 5 PM cutoff.

Do I have a legitimate argument that I’m being penalized for the mortgage company’s delayed processing time?

Wayne,

I’m sure you could call and ask for a refund for the late fee in “good faith,” at least just this one time if they’re at all reasonable.

Colin, thank you for all of this info.

You mention that you don’t pay less interest if you pay your mortgage early, but do you pay more interest if you pay during the Grace period (after the 1st)?

Thank you again for an excellent and informative article.

Have a great holiday weekend.

Victor

Victor,

You shouldn’t because the grace period essentially gives you extra time to make an on-time payment. It’s always best to ask your loan servicer directly to be sure. Have a great weekend as well, thanks!

My daughter has had a mortgage with good payment record for 4 years. Today she realized her June mortgage payment was never made by her husband and immediately made the payment.

She is also in the process of selling her present house and buying a new one.

Will this late payment be on her credit report and will it hurt their chances for a mortgage on the new house they are buying?

Anna,

Generally, payments need to be 30 days late to be reported as late on a credit report, so hopefully she is okay.

Colin, please help. We have had the same mortgage company for 12 years. Last year my mother fell ill, my husband and I traveled with our 10 children to care for her and my father during Christmas. We had not realized our mortgage payment due on the 15th did not go through. We immediately paid it the first week in January and were assured by the bank it would not go on our credit score. We tried to refinance this year to make some much needed upgrades and repairs on our home, only to find it had been reported as 30 days late. After calling the bank we were told they report to the credit agencies the 3rd of each month regardless. I wrote a letter of goodwill with a denial. My question for you is, the payment was not 30 days late though it was reported as so. I am not denying we were late, but do I have a case for dispute. We have never been late in twelve years with the exception of this one incident.

I got a home loan thru my bank 21 years ago and the payment coupons always showed the late date (first was the 15t then the 18th) plus the penalty fee. The bank sold the note to Freddie Mac long ago so now just services the account. I’ve been having problems this year and got two months behind once then have been late with the rest except once. Just received my new coupon book which doesn’t show a late payment date nor penalty for one. My loan agent always seems to be out when I call about so don’t know what to make of it. Does that mean I no longer have a grace period or are they cutting me some slack? The bank obtained an insurance policy to cover the balance of the note since my previous carrier wouldn’t renew the policy due to needed exterior repairs (bad wood, peeling paint and the roof). Since then I have taken care of the wood and paint then replaced the storm damaged shingles. I’m trying to sell the house by owner and the bank knows it. Just wondering if Freddie Mac will call in the note if I continue to make late payments since the balance is $32K and the property worth as-is to be over $130K.

Bill,

Probably best to ask the current loan servicer directly to clarify on due dates and grace period.

Suzanne,

If you feel it is being misreported you can file a dispute with the credit bureaus (Experian, Equifax, Trans Union) online. Hopefully they won’t fight it and you can get the lates cleared up.

Ok guys,

My question is I recently moved from Indiana to Missouri and bought a home. This required me to switch from chase to Bank of America with no chase bank in Missouri. I always pay my mortgage earlier then the grace period which is the 16th. This month I moved money accidentally out of my secondary account with B&A instead of my primary. This caused my check for my mortgage to bounce! I saw it today and moved money back to the correct account and paid it again! My question is my mortgage will clearly be paid before my grace period of the 16th . Will this affect my credit? Or mess anything else up? Thanks!

Jean,

Not sure, you may want to ask your servicer directly to see if the amounts are off or if they allocated incorrectly.

Todd,

Generally mortgages are only considered late if delinquent for 30 days and reported to the credit bureaus as such only after that amount of time has passed. A payment that is a few days late is typically just hit with a late fee and no credit hit.

If I pay my mortgage today (September 13th) and its due October 1st, will it be applied correctly? Im not trying to save money on interest…I just want to make my payment now while I have the money and before I forget. I don’t know how soon in advance I could make a mortgage payment. Thank you!

Veronica,

Generally payments made before the 15th of the month go to the prior month’s payment and after the 15th go toward the next. Not sure you’ll save any money paying early because mortgages are typically calculated monthly, not daily.

My lender just sold my mortgage The maturity date was 2028

The new lender states on monthly payment the maturity date is 2022. Payment amount did not change Not sure whats going on When I call they tell me the computers are down.

Sue,

Hmm…maybe it’s an error, but probably best to keep pressing them on it to ensure it’s fixed or resolved. Good luck.

Hi Colin,

If my payment is due on the 17th of each month and I get paid on the 1st and 15th, is it OK to make 2 payments prior to the due date? For example my payment is $1200, so the first I pay $600 and the 15th I pay $600…?

Paula,

You’ll have to ask the loan servicer directly how they handle multiple payments…do they consider the first payment “short” and reject it, or set it aside as insufficient? Or do they allow multiple payments as long as they add up to the full payment amount and then process it? Best to ask your servicer directly to avoid any unwanted surprises.

Does anyone know of any mortgage companies that will take any payment received and apply it to the loan IMMEDIATELY? I’m looking to pay every 14 days, but all companies I’ve found will only apply payments to the loan once a month. Thank you!

I have mortgage with PHH. Just noticed that a few years ago they started applying my extra payments to the next month due date. It used to be current month for a while so I stopped checking on it. They did it without notified me. Is this legal to do? It already cost me a few hundreds of extra interest paid.

Customer service tried to convince me that it does not matter how they apply the extra payment.

Olga,

Not sure about legality, but it certainly sounds frustrating. You may want to clarify in the future when sending extra payments. Some borrowers will write on the check something like “pay to principal balance” so the lender knows to apply it there instead of just holding it and applying it to the subsequent month’s payment.

I pay $700 over the payment amount of $1,300 for my mortgage ($2,000 total). I pay all that on the due date via automatic payments through my bank to the mortgage site (Quicken/Rocket).

I’m wondering, however, if there would be any benefit or risk in sending that extra $700 in principle reduction at any time other than the 1st of the month.

So would sending that $700 principle reduction, say, mid month, the 15th, post as principle reduction, or would doing that cause the $700 to post as partial payment for the next upcoming payment due?

Thus far I’ve shaved four years of payments off my mortgage, according to QL/Rocket, which is a bit more than $40,000. Gotta love that! I hope I live long enough to appreciate that savings, LOL!

They’d likely hold the partial amount until receiving the full amount, then apply it on the normal due date. So it probably wouldn’t change things other than leaving your bank account earlier and possibly costing you some lost interest earnings.

Hi

New Rez mortgate charges me a late fee of $5 for 5-9 days after due date, 1st of month, $10 10-15 days late and $10.00 if 10 or more days late – on top of a $91 late fee charge at day 16. Is this legal?

Jen,

While many loan servicers allow payments to be made until the 15th, they are typically due on the 1st of the month, so it’s possible they are able to charge a late fee. Probably best to contact them directly for their specific policy.

Hi,

Thank You for the extremely useful info. I have an ARM Loan that my rate should be fixed for 10 years! I pay for an instance mortgage payment that is due on April 1st $4,300 on March 7 and then as soon as I receive my next paycheck, I make an extra $7000 towards principal my principal only is submitted only towards the end of the month like 28th-30th. The reason being is that I don’t want to have a late fee or late in any records! I realized that the loan service company do not include my $7000 extra payment on my next bill and I still need to pay higher interest on the previous loan balance before the $7000! Is this normal and lawful to charge interest on money that you no longer owe?

Per my calculation, since it adds up each month so far in the last 11 months duration of my loan, if they had added my extra principals correctly, I should have been $1232.32 ahead! I have created an excel amortization model from banks that I follow and I am 100% sure of it accuracy. What do you suggest? How can I follow up?

Thank you for your educational site.

Angi,

The issue may be that the loan servicer doesn’t apply any extra funds to principal until you make a payment each month, and anything received in between payments is likely set aside until the next payment becomes due a month or so later. Paying before the due date generally does nothing to save you money, but paying extra WITH your normal monthly payment can reduce interest in future months. You may want to call your servicer directly to communicate your desire to make additional payments to principal and how best to go about it so they apply it correctly.

Not true mine like everyone’s is due on first by the 15th I have paid at night of the 15th and early morning 16th and I am dinged for 3 30-day payments over the last 8 years. One day past the 15th equals to late fee and a 30-day late ding on all three credit bureaus . So what should I do?

Lee,

It’s possible your payment didn’t clear during the grace period (typically up until the 15th) and thus was assessed a late fee. And that may have eliminated future grace periods, which could have resulted in a 30-day late. Ultimately, the paperwork generally says payments are due on the 1st, but most servicers I’ve come across allow on-time payments until the 15th if your account is in good standing. Once you go beyond that, any grace period might cease to exist until you get back on track. But the best place to get clarity would be directly from the loan servicer’s billing department.

Hello, thanks for allowing people to write to you regarding mortgage payment questions, here’s my hiccup. I’ve purchased 2 homes in my past and have been in my 3rd home now for 11 years and have always relied on the 15 day grace period. I have always paid before the 30th to avoid being reported to credit bureau. I recently refinanced my home and made my first payment last month.

I got hurt on the job early this month and was out on Workman’s Compensation so I called my mortgage servicer to inform them I will be late with my October payment and was told I would be assessed a late fee which I expected since it was past the 16 day grace period. They told me that to make sure my payment was made by the 30th. I paid it on the 29th which is a Friday. When I submitted the payment on their website it said I made my payment on the 29th, but it will not post til Monday, November 1st. Does that mean they excluded weekends thus making my payment past 30 days and being reported to the credit bureau? Or does it mean my payment was considered on time but would post to clear on the 1st? It was made before the 30th which is hopefully considered on-time. Your thoughts?

Hi Rose,

Good question – and it may depend on the loan servicer. Some may process payments differently. It’s entirely possible it’ll count as paid on time (or at least not 30 days late) if it’s at least submitted before the 30 days. Ultimately I’d call the servicer directly to confirm. But this illustrates the danger of paying late as things like processing time could throw a wrench in the deal. Good luck and let us know what happened!

I completely missed a mortgage payment and the payment was 63 days late and I was charged a late fee of 5%. The next payment I made was 30 days later and they again charged a 5% late fee.

Will I forever be charged a late fee after 1 totally missed payment or can I avoid this ‘chronic late fee’ by making both the missed payment and the one that’s now due?

My mortgage company will not post a late payment to the credit bureau until after 30 days. The month of February has 28 days, how does that work?

Alee,

You may need to bring your loan completely current to avoid subsequent late fees. This means paying any outstanding fees and missed payments in full to get back on the original schedule, along with making future monthly payments on time. But a call to your servicer may confirm these details.

Charlene,

Your loan servicer may be able to clear this up – it could be reported to the credit bureaus after March 2nd if February only has 28 days and they have a hard 30-day timeline.

I made my mortgage payment on the 29th but it will not be effective until Monday the 31st. Will the 30 day late be reported to credit?

Mortgages are due in arrears. For example, the July payment is due August 1st, but many loan servicers are OK with payments made up until August 15th. But always best to call your servicer/bank directly to be sure of their policy.