Mortgage Q&A: “Is now a good time to refinance my home?”

If you’re one of the few people asking this question right now, the short answer is most likely no.

And the reason it’s a no is because mortgage rates have skyrocketed over the past 18 months or so.

But like everything else in the mortgage world, the answer does depend on the situation.

Not everyone has the same mortgage rate, nor do they have the loan product, or the same needs.

Very Few Homeowners Benefit from a Refinance Right Now

- A refinance typically only makes sense if you can obtain a lower mortgage rate in the process

- This is very difficult to accomplish at the moment with rates averaging 7%+

- Most homeowners already refinanced a couple years ago when rates were priced around 3%

- Refinancing will make sense again once rates fall and/or more borrowers take out mortgages at today’s higher rates (giving them a future refinance opportunity)

First things first, there are two main mortgage refinance options available to homeowners, including the rate and term refinance and the cash out refinance.

There is also the streamline refinance, which is a fast-tracked type of rate and term refinance.

For simplicity sake, a rate and term refinance allows a borrower to lower their interest rate, change their loan term, and/or switch loan products.

The cash out refinance allows a borrow to tap their home equity and perhaps change their rate, term, and loan product as well.

At the moment, very few borrowers are applying for rate and term refinances because interest rates aren’t favorable.

Conversely, everyone and their mother was applying for one back in 2020 and 2021, when mortgage rates hit record lows.

This made perfect sense because you could swap your existing 4-6% mortgage rate for one in the 2-3% range, or even in the 1% range if it was a 15-year fixed mortgage.

Rate and Term Refinances Are Virtually Nonexistent

Times have changed, and now that mortgage rates are closer to 7%, there’s very little reason to pursue a rate and term refinance.

A new report from ICE revealed that only about 5,500 rate and term refinances have been originated per month, on average, over the past year industrywide.

To put that in perspective, there have been roughly 650,000 rate and term refis funded each quarter going back 15 years.

Today, it’s closer to 16,500 per quarter, which is record low territory. It’s also a pretty clear sign that a rate and term refinance doesn’t make sense for most people.

As a rule of thumb, if you can’t lower your existing mortgage rate by say 1% or more, it doesn’t make sense given the closing costs, the time, and the hassle.

And resetting the clock on your mortgage in the process. So unless your current mortgage rate is say 8.5% or higher, it likely doesn’t make sense.

The one caveat is someone who is removing a co-borrower or spouse from their loan out of necessity. But even this is being avoided if at all possible due to the great rate disparity today.

The bulk of these types of refinances is coming from legacy vintages, aka older home loans.

Eventually when interest rates fall, those with today’s 7-8% mortgages will make up the bulk of rate and term refis.

[When to refinance a home mortgage]

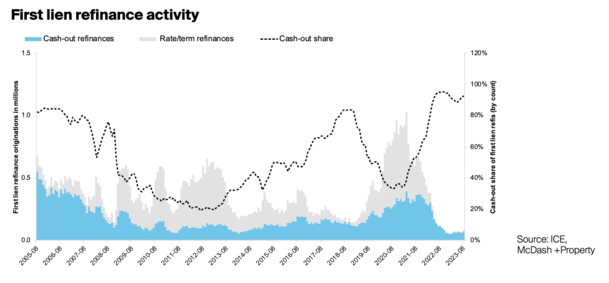

The Cash Out Refinance Share Is Nearly 100%

On the other side of the coin, we’ve got a cash out refinance share that has hit record highs lately.

Per ICE, it grabbed a staggering 96% market share in the fourth quarter of 2022, the highest level on record, and hasn’t really changed much since then.

Ultimately, the only reason to refinance a mortgage right now is to tap equity, often because the homeowner needs cash.

This explains why virtually every refinance originated today includes cash back to the borrower.

Because most homeowners have very low mortgage rates, often locked in for the next 30 years, there has to be a compelling reason to give that up.

And that reason is a dire need for cash, even if it means losing their ultra-low mortgage rate in the process.

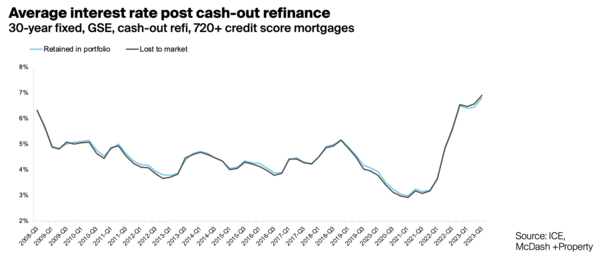

As you can see from the chart above, the post-cash out refi mortgage rate has increased significantly.

But while the cash out share is extremely high, the volume of cash out refinances remains low relative to prior years.

Despite tappable equity being close to its 2022 highs, less than $8B was withdrawn from the housing market via a cash-out refinance in August.

While it might sound like a large number, it’s about 70% below the highs seen last year, a consequence of those higher interest rates.

In other words, the overall volume of cash out refis is also way lower than it has been in past years, again because of the high mortgage rates available.

Instead, those who need money are likely opening a second mortgage, such as a HELOC or home equity loan.

Both options allow the homeowner to keep their first mortgage untouched, meaning they don’t lose the low fixed rate.

[How to Lower Your Mortgage Rate Without Refinancing]

Who Would Refinance Their Mortgage Today?

So let’s walk through some different scenarios to see who, if anyone, could benefit from a refinance right now.

Imagine a homeowner who purchased a $500,000 property in 2021 when 30-year fixed mortgage rates were 2.75%.

The property is now worth $600,000 and they want cash to pay for other expenses.

There’s basically no way they’re going to give up their 2.75% rate, so a second mortgage would be the only deal that made sense.

Now imagine a homeowner who purchased a property for $300,000 in 2004 that is now worth $650,000. They need cash and their remaining mortgage balance is only around $130,000.

They might consider refinancing and pulling out cash because their existing loan is small and their old rate may have been 6% anyway.

It might not be ideal, since they were only a decade from being free and clear, but at least they aren’t giving up a low rate on a big loan balance. And again, they need cash.

When it comes to a rate and term refinance, we’ll likely need mortgage rates to come down a bit more from current levels to appeal to recent home buyers.

If these buyers have been taking out mortgages with rates in the 7-8% range, it’s possible they’ll be able to save money by swapping the old loan for a new one at say 6%.

In the meantime, homeowners can pay extra each month to reduce the interest expense, assuming they have the means to do so.

Read more: Alternatives to Refinancing a Mortgage

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

- Mortgage Rates Are Having a Good Day as Oil Prices Fall to Pre-War Levels - June 24, 2026

- You Can Still Get a Sub-6% Mortgage Rate, But Is It Worth It? - June 23, 2026

Our 7-1 ARM expires in June, and our interest rate will increase from 3.125% to 8.125%. In June, we will both be retired. We have a balance of $270k and 23 years on the term. We have the funds in our IRA to pay down or even pay off the balance. We’re thinking of paying down the balance to either $220k or $170k (if the lender will recast the loan to try to reduce the monthly payment) while we wait for interest rates to drop to the point where we can refinance and maybe buy down the rate further. Biggest unknown is whether we can refinance with both of us retired.

Any thoughts on this scenario?

Your blog posts have been super helpful and informative, but I didn’t see the retirement aspect addressed. Thanks.

Hi Janet,

May want to explore your eligibility now if you both plan on being retired, as that will require retirement income to be used to qualify. Retirement assets can also be used to qualify if sufficient.

This will help determine if you can get a mortgage (refinance) at that time if needed. That way you’ve got options if rates improve.

You may also want to double-check your paperwork to see what the caps are on the ARM. Sometimes they limit how much the rate can go up upon first adjustment.

Good luck and happy retirement!