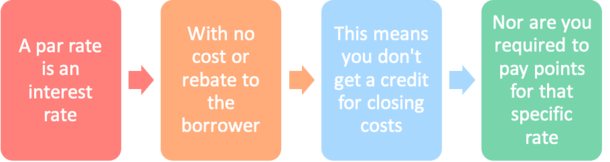

In the mortgage world, the “par rate” is the mortgage rate a borrower qualifies for assuming there is no interest rate manipulation of any kind.

This means no discount points should be paid by the borrower to get a below-market rate.

And there should not be a lender credit OR lender-paid compensation, as either would push the interest rate above the true market price.

This par mortgage rate, otherwise known as the base rate, is also determined by a borrower’s particular loan scenario.

It may include mortgage pricing adjustments for things such as loan amount, credit score, property type, loan-to-value ratio, and so on.

As such, a high-risk borrower will have a higher par rate than a low-risk borrower because of said adjustments.

Let’s look at an example of a par mortgage rate:

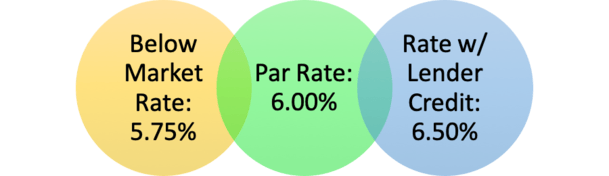

– 6.5% = -1.00

– 6.25% = -0.50

– 6% = 0.00 (par rate)

– 5.75% = 0.50

In the example above, we see a list of mortgage interest rates with corresponding fees or rebates. Let’s pretend the loan amount is $500,000.

On the surface, a rebate is a good thing because it means you get a credit toward your closing costs.

For example, -1.00 for a rate of 6.5% means you get 1% of the loan amount in money back, or $5,000. That money could be used to pay the lender and/or other third-party costs.

However, it also means the interest rate is higher than par as a result. No free lunch!

Conversely, the fee of .50% would cost you money out-of-pocket at closing, but result in a lower rate of 5.75%, which is below par.

Like golf, being below par is a good thing since it means you get a better rate, lower payment, and pay less interest.

In this case, you’d owe the lender $2,500 at closing, plus all the other costs associated with the loan! But you’d have a lower monthly payment thanks to a better rate.

For our hypothetical borrower, a rate of 6% is the par rate, assuming there are no pricing adjustments, because it has zero associated cost and no rebate (represented as 0.00 above).

This means the borrower isn’t getting a closing cost credit for obtaining that specific interest rate, nor does the borrower have to pay anything (discount points) to receive it.

Pretty straightforward, right? But wait, there’s more!

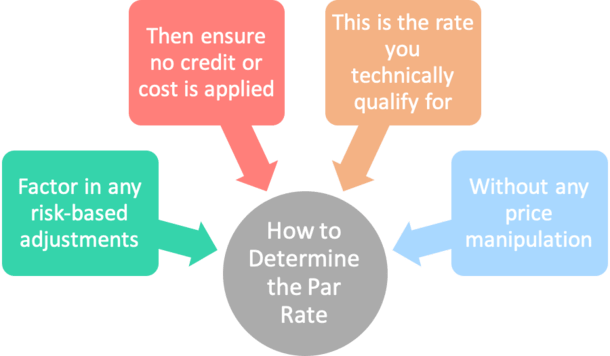

We Need to Consider Pricing Adjustments Too

- Before we get to the par rate on your home loan

- We have to tally up any risk-based price adjustments that apply

- These account for certain risk factors that might be present in your loan scenario

- They apply to credit score, occupancy, loan type, transaction type, LTV, and so on

Mortgage lenders apply all types of risk-based adjustments to home loans to ensure the price reflects the risk of default.

This is why it’s impossible for them to quote a daily rate to anyone who calls them. There are too many borrower- and property-related factors to just throw out one rate for everyone.

For example, your particular loan scenario may have a mortgage pricing adjustment of 0.25% for a DTI ratio over 40%, and a credit score adjustment of 0.25% for having a 720 FICO score.

This would make your total “adjustments to fee” 0.50%. That figure needs to be incorporated into the base rate to determine the par rate.

And it might differ from another borrower who has 670 FICO score and a smaller down payment.

How to Calculate the Par Mortgage Rate

You need to factor in price adjustments to figure out your actual, or adjusted par rate. In the example above, total adjustments of 0.50% would result in a rate of 6.25%.

Simply put, the par rate is the difference of the adjustments to fee of 0.50% and the price of -0.50, which equals zero, or par.

Now if your loan had no pricing adjustments, your par rate would be 6%, as explained above.

And if you had no adjustments, but wanted the lower rate of 5.75%, you would have to pay 0.50% in discount points.

If the loan amount was $500,000, you’d owe $2,500 at closing for that lower-than-par rate.

Conversely, imagine if you didn’t want to pay closing costs out-of-pocket. You could elect to take a higher-than-par rate of 6.5% and get a 1% credit.

Using our same $500,000 loan amount, this would result in a $5,000 credit. That could be used to offset any lender fees and third-party costs associated with the home loan.

This is how a no cost refinance works.

Get to Know Your Home Loan to Land a Low Rate

- The key to obtaining a low rate is knowing how risky your home loan is

- This means researching what price adjustments typically apply to your scenario

- Asking the loan officer or broker what adjustments your loan is subject to

- Then shopping your rate with other banks and mortgage lenders

A borrower may not know that their particular loan scenario carries few, if any adjustments. And that it will allow them to obtain a low par rate.

For example, a borrower purchasing a primary home with excellent credit and a huge down payment should receive the best pricing.

But if you don’t realize this, an unscrupulous broker and lender may tell you that your deal is trickier than it appears.

So be sure to review the mortgage adjustments section of this site to see what lenders usually hit borrowers for.

You can also check out the LLPAs from Fannie Mae. Or simply ask the bank or mortgage broker what adjustments apply to your loan.

Otherwise you could end up with a higher mortgage rate than you deserve, which will cost you big if you hold onto the mortgage for years to come.

Keep in mind that the broker/lender still needs to make money for processing and funding your loan.

So they may need to charge an out-of-pocket loan origination fee or receive lender-paid compensation, the latter of which can also bump up your rate above par.

What Is the Par Mortgage Rate Today?

Consumers always want to know what “today’s rate” is without providing further context.

As mentioned above, due to the intricacies of mortgage rate pricing, there is no universal rate for everyone.

Sure, the loan officer or broker can tell you that the average rate according to Freddie Mac is X today. But that’s just a composite rate based on a survey of dozens of different lenders.

The same is true of any weekly or daily rate you may come across. It’s just a baseline or average.

If you happen to see daily mortgage rates on a bank or lender’s website, pay attention to all the loan assumptions made in the fine print.

It will likely say something like assumes borrower has a 30% down payment, 780 FICO score, and is buying an owner-occupied single-family residence.

Anything that deviates from what is often a very vanilla and thus rate-friendly loan scenario, and the expected rate will be higher.

So again, you need to take those rates with a huge grain of salt and actually get a personalized quote for accurate pricing.

At the end of the day, the par rate doesn’t really matter. What matters is the rate you receive and the costs involved. If you can get the lowest rate with the lowest amount of out-of-pocket fees, you win.

Par Mortgage Rate Key Points

- A mortgage rate with no lender credits or costs (discount points)

- Or baked-in lender compensation (to avoid out-of-pocket costs)

- That also factors in any pricing adjustments (e.g. credit score, LTV, property type, etc.)

- This provides the true market rate for your particular home loan

- You can then decide to accept a below-par or above-par rate based on associated costs and credits

- And perhaps more easily shop your loan with other lenders knowing this base rate

- Just keep in mind there are still origination costs for taking out a mortgage (they don’t work for free!)

Tip: What mortgage rate should I expect to receive?

- Mortgage Rates Narrowly Avoid New 52-Week Highs as Bond Yields Surge Higher - July 31, 2026

- Trump Says Warsh Wants Lower Interest Rates, But Has a Political Board - July 30, 2026

- Do Mortgage Rates Need a Hike to Move Lower? - July 28, 2026

You should add that the par rate can vary by lender. I was told my base rate was 3% with one lender, and 3.5% with another, for the same exact loan. So people need to shop around.

How do you know if you’re getting the par rate vs. an inflated rate?

As long as there isn’t a lender credit or lender-paid compensation, the rate should be at par. But that means you’ll need to pay out-of-pocket for loan origination and other lender fees. Nothing is completely free, though at least you’ll be getting a market rate.

Par rate does not vary by lender, it should be the same for a given set of parameters like zip code, credit score, loan amount, and term.

Hi Colin,

I have been quoted a PAR rate of 5,625 for a loan of 150.000 on a 450.000 commercial rental property and 1% orgination fee.

I put down 300.000 myself

Does this sound right to you

Ron,

I don’t know commercial property rates…my focus is on residential mortgages. Best way to know might be to obtain other quotes and see where it falls. Good luck.

Hello. Doing a jumbo purchase loan for the first time. Not many lenders offer Jumbo loans. With a house value of $850,000, loan amount of $680,000, client paid 1%. Trying to see the best option with no cost to the borrower, above the par rate at least. Not seeing many options.