A new startup called “Roam” has launched a service to make assuming a mortgage painless.

The company is backed by some prominent real estate figures, including Opendoor co-founder Eric Wu and former Fannie Mae CEO Tim Mayopoulos.

The goal is to help more home buyers take advantage of the many low-rate mortgages in existence via a loan assumption.

This includes FHA loans and VA loans, both of which are assumable by home buyers.

Roam acts as a hands-on guide for buyers and sellers to ensure the process goes smoothly in exchange for a 1% fee.

How Roam Makes It Easy to Assume a Mortgage

While many home loans are assumable, including all government-backed loans (FHA/VA/USDA), the process isn’t so straightforward.

Roam notes that the loan assumption process is “opaque and time-consuming,” and often requires buyers to fill out forms with paper and pen and fax them to the lender or loan servicer.

There’ also uncertainty for the home seller, who might not be sure if they’re still liable for the loan post-assumption.

To alleviate some of these pain points and ensure the process is done correctly, Roam manages all the operational details on behalf of the buyer, seller, and real estate agents.

They don’t approve the loans, but act as a facilitator and provide guidance/support throughout the process.

In addition, Roam makes it easier to find homes for sale that feature an assumable mortgage.

Once you sign up via their website, they’ll compile a set of for-sale listings that feature an assumable, low-rate mortgage.

These listings will also be tailored to fit your other criteria, such as location, home price, number of bedrooms and bathrooms, and so on.

At the moment, it seems only FHA loans and VA loans are included, not USDA loans.

What’s neat is a non-veteran has the ability to assume a VA loan, and can even buy the property as an investment or second home.

If you come across a property you like, they will work with the lender and loan servicer to begin the loan assumption process.

As noted, this includes obtaining a release of liability of the loan for the home seller, which should ease their concerns as well.

Bridging the Gap Between Old Loan Amount and New Purchase Price with Roam

One sticking point to a loan assumption is the shortfall between the sales price and the remaining loan balance.

For example, the existing loan balance might be $450,000, while the new sales price is $550,000.

The buyer could come in with the difference, but it’s unlikely they’ll have the funds unless they have very deep pockets.

In this case, Roam has “preferred partners” that can provide additional financing, typically in the way of a second mortgage.

Together, this should still provide a blended rate that is well below current market rates.

If we consider a 2.5% first mortgage at 70% loan-to-value (LTV) combined with a second mortgage for an additional 10% at a rate of 8%, the blended rate is roughly 3.2%.

At last glance, the 30-year fixed is priced around 7.25%, so that represents quite the discount.

To that end, only mortgages with rates below 6% are included in the Roam listings.

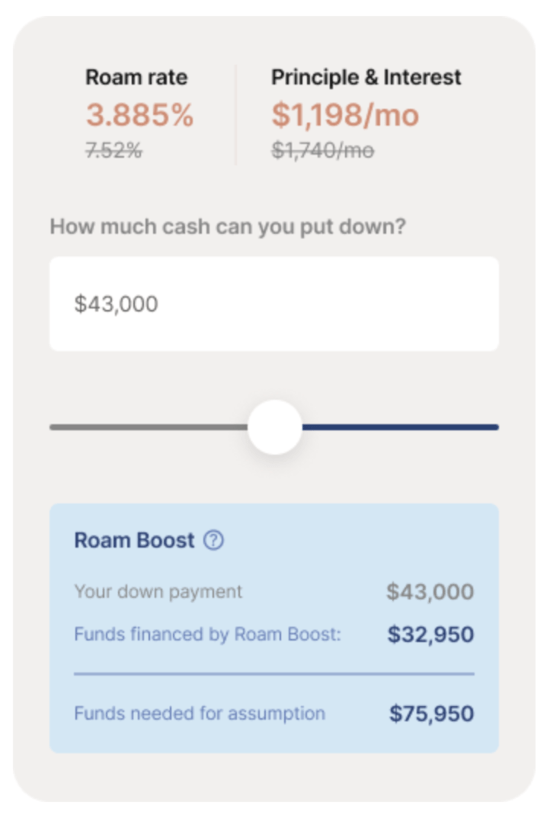

Roam Boost Offers Second Mortgages From Partner Lender Spring EQ

In May 2024, the company rolled out “Roam Boost,” which allows for lower down payments and increased purchasing power (ignore the fact that they spelled principal wrong!).

To bridge the gap, a home buyer can come in with a smaller down payment and supplement it with a home equity loan backed by Spring EQ.

Together, a buyer can purchase a home at up to 85% CLTV, meaning only a 15% down payment is needed.

And because of the way the loan is structured, no private mortgage insurance will be required because the first loan will be at/below the key 80% LTV threshold.

These loans are offered in a variety of terms from 5 to 30 years with loan amounts from $25,000 all the way to $500,000.

How Much Does a Roam Assumable Mortgage Cost?

While this service sounds pretty great, there is a cost to use it. At the moment, Roam is charging 1% to the home buyer via closing costs.

The 1% fee is based on the new sales price of the property, not the assumable loan amount.

In exchange for this fee, Roam says it will “coordinate every detail on behalf of sellers, buyers, and agents,” including connecting buyers and sellers, handling paperwork, and overseeing the financing.

Additionally, you don’t have to pay for an appraisal because the assumption doesn’t require it. So you can save some bucks there as well.

Home sellers do not need to pay anything to take part and Roam will ensure the seller’s name is removed from the mortgage.

This means sellers will not be associated with the mortgage or held liable once the process is completed.

That should provide peace of mind to the seller, who might be concerned about their credit score being affected by the buyer’s subsequent mortgage payments.

If it’s a VA loan that is being assumed, Roam can help find a qualified military buyer if the seller would like to free up their entitlement.

This allows military homeowners to take out a new VA loan when it comes to their next home purchase.

Roam may also make money from their second mortgage partners, though they are fine with home buyers using the lender of their choosing.

Same goes with real estate agents. If the home seller doesn’t have a listing agent, Roam can recommend one. This may also earn the company a fee.

But the company can work alongside any listing agent, loan servicer, or mortgage provider to complete the process.

Roam Offers a 45-Day Closing Guarantee

To take uncertainty out of the equation for both the home seller and the home buyer, Roam now offers a 45-Day Closing Guarantee.

If Roam isn’t able to close your assumable loan within this time period, they’ll cover the seller’s mortgage payments until it does.

This provides peace of mind to sellers, who may not be incentivized to let a buyer assume their mortgage. After all, it can be a slower process relative to a traditional home loan.

So they won’t want to take chances if it costs them money in the process.

On the buyer side, it means the deal won’t fall through if Roam takes care of the seller while any delays are sorted out.

The 45-day window starts from the date of offer acceptance and sellers must sign the Roam Seller Closing Guarantee.

In addition, sellers must provide proof of mortgage payments made during the period to ensure “prompt and accurate reimbursement.”

Roam Lets You Buy a Home with Bitcoin

A new feature rolled out in mid-August 2025 allows Roam users to buy a home with bitcoin.

And they can do so without actually liquidating their bitcoin holdings.

Instead, they take out a BTC-collateralized loan offered by a company called Lava, which has partnered with Roam.

This results in an advance of anywhere from 10% to 50% of a home buyer’s BTC holdings in USD value.

The loan can then be used to fund the earnest money deposit, down payment, and/or closing costs needed for the purchase.

Importantly, the home seller is paid in U.S. dollars, and the buyer gets to keep their BTC holdings in place to enjoy possible upside.

However, there are risks for the buyer if BTC drops by a significant amount and triggers a margin issue.

Per the Lava website, fixed interest rates start as low as 5% and loan amounts don’t seem to have any cap, not that you’d need an excessive amount to close the assumption gap.

Lava is backed by some major players, including Founders Fund and Khosla Ventures.

This combination of a low mortgage rate plus the ability to use crypto could appeal to a certain type of home buyer.

Is the Roam Assumable Mortgage a Good Deal?

Over the past couple decades, assumable mortgages weren’t a thing because mortgage rates were constantly falling.

In fact, mortgage rates hit record lows in 2021 and have since nearly tripled in just over two years.

This has finally made the assumable mortgage a thing, and a potentially very powerful thing.

If a home buyer is able to obtain the seller’s mortgage, possibly in the 2% range, it would be a huge feat, even with a 1% fee.

For example, take a $500,000 home purchase that has a $400,000 outstanding loan balance set at 2.5%.

The $400,000 loan amount would be about $1,580 per month. But let’s suppose the home buyer needs a second mortgage to bridge the gap with the new purchase price.

A $50,000 second mortgage set at 8% would be another $367 per month, or about $1,950 all in.

Compare that to a single new mortgage at $450,000 with an interest rate of 7%, which would be roughly $3,000.

And it could be subject to mortgage insurance as well if it’s one loan at 90% LTV.

The only thing you’d really need to watch out for would be an inflated purchase price if the seller believes they can charge more thanks to their assumable mortgage.

But even then, the property would need to appraise (if taking out a second mortgage and it’s required) and the savings could still eclipse a slightly higher price, as explained in the scenario above.

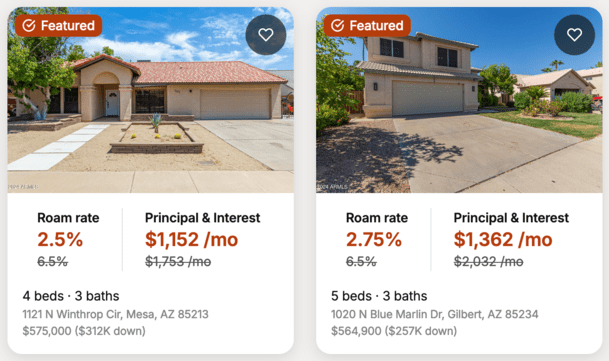

On the other hand, the sheer size of a second mortgage could also be a bridge too far. As seen in my screenshot above, the down payment on the two properties in Phoenix, AZ are $312,000 and $257,000.

Those are arguably large enough loan amounts to be considered mortgages on their own!

Roam is initially available in the states of Arizona, California, Colorado, Florida, Georgia, Illinois, Indiana, Maryland, Michigan, Missouri, North Carolina, Oklahoma, South Carolina, Tennessee, Texas, and Virginia, with other markets expected soon.

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

- Mortgage Rates Are Having a Good Day as Oil Prices Fall to Pre-War Levels - June 24, 2026

- You Can Still Get a Sub-6% Mortgage Rate, But Is It Worth It? - June 23, 2026

Arizona, Colorado, California

Their PR said Roam’s service is initially available in GA, AZ, CO, TX, and FL.

The only issue I see is that they say they will work with the seller’s agent. A seller that has a VA assumable doesn’t need a real estate agent. If that were the case why use a service like ROAM? I can just have my agent list it on the MLS and agree to pay him 3% to do so for marketing purposes. Why not give the seller the power to do that on the platform with all the free tools they offer the agents?

I received an email from your company and as a seller’s agent, have a listing on a VA assumable loan at 2.5% I want to know if you connect buyers and sellers. I prefer to speak to someone rather than go on your site to try and figure this out.

Per Roam, they simply provide free marketing materials to RE agents who sign up on their website, including personalized open house flyers, enhanced listing photos, updated public remarks, and lawn signs.

Why doesnt a listing on realtor.com list a property as assumable, but ROAM does? Causes me to question the legitimacy and/or accuracy of ROAM.

Does Realtor show some as assumable and some not? Or none at all?