As home prices continue to flirt with record highs nationwide, the cost of property taxes and hazard insurance can be the tipping point.

For example, if you purchase a one-million dollar home these days, you can expect to pay around $15,000 or more annually for property taxes and insurance in certain states. Ouch!

On a monthly basis, you’re looking at an additional $1,250, which is what a total monthly mortgage payment might cost folks in other, less expensive parts of the country.

That’s a large chunk of change, especially considering million-dollar homes in California are the norm for many popular metropolitan areas.

Factor in that most people buying these caliber homes aren’t necessarily multi-millionaires either and things can get unaffordable in a hurry.

Simply put, if and when you buy a home, you need to consider these additional costs instead of merely looking at the mortgage payment.

Taxes and Insurance Can Account for a Big Chunk of Your Mortgage Payment

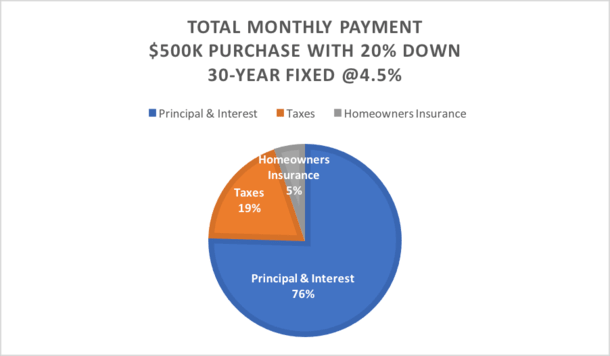

Let’s look at a hypothetical $500,000 home purchase in California. Yes, there are still homes offered at that price, I think?

Anyway, assuming our imaginary borrower could muster a 20% down payment, they’d be left with a $400,000 loan amount.

If they obtained a mortgage interest rate of 4.5%, their monthly principal and interest payment would be $2,026.74. Not too bad, right?

But wait, there’s more! We have to dial in the property taxes and homeowners insurance, which will change the equation.

Let’s add $6,250 annually for property taxes and $1,650 for a decent homeowners policy.

Assuming you pay these costs monthly as many homeowners do thanks to an often required mortgage impound account, it’ll add roughly $660 to your total outlay.

We’ve now got a monthly housing payment (not just the mortgage folks) of about $2,700, of which nearly 25% can be attributed to taxes and insurance.

Quickly our $2,000 payment jumped to close to $3,000. Factor in other costly utilities like water, electricity, gas, etc. and you could be at $3,500.

This is why lenders impose DTI ratio limits to ensure you don’t get in over your head, even if you think you can afford it.

Property Taxes Vary by State – NJ the Most Expensive, Hawaii the Cheapest

- You can’t totally ballpark estimated property taxes

- Since they vary widely from state to state

- But as a general rule

- 1.25% of the purchase price is a good estimate

The annual property tax rate does vary by state, but as a general rule you can assume 1.25% to 1.5% of the purchase price to stay on the safe side, though it can be as low as 0.3% or as high as 2.4%.

Property taxes tend to be higher than average in states like Connecticut, Illinois, Nebraska, New Hampshire, New Jersey, Ohio, Texas, Vermont, and Wisconsin.

I believe New Jersey property taxes are the most expensive, with Texas not far off.

Conversely, property taxes are relatively dirt cheap in states like Alabama, Arizona, Arkansas, Hawaii, Louisiana, Nevada, New Mexico, South Carolina, Utah, West Virginia, and Wyoming.

As far as I know, Hawaii always seems to have the cheapest property taxes of any state in the nation, which is surprising given its location in the middle of the Pacific Ocean.

To find out the property tax rate in your area, contact your county tax collector for an estimate of your fully assessed property taxes.

Or visit your county tax assessor’s website. The lender and/or escrow company should also be able to track down this info.

Most counties reassess the property tax rate each year, and the number is likely to be higher than what it was last year, or what the previous owners paid.

It should also be noted that property taxes are based on the purchase price, not the loan amount! This is one more reason to negotiate a lower sales price!

Tip: When using a mortgage affordability calculator, be sure to factor in these costs, which could make or break your loan application.

Estimating the Cost of Hazard Insurance Quickly

- If you want to estimate the cost of hazard insurance

- Simply multiply the purchase price

- By between 0.25% to 0.33% (higher end for a buffer)

- Or get an actual quote beforehand to really know where you stand

Then there’s hazard insurance, which is about 0.25% to 0.33% of the purchase price for a 12-month policy.

So if you’re looking to do a quick estimate on a home that sold for $500,000, the cost would be roughly $1,250 to $1,650 per year.

However, these premiums also vary by state and by insurance company, with the most notoriously expensive states being Florida and Texas.

These are the places where hurricanes and tornadoes can wreak havoc on properties (and the companies that insure them).

If possible, try to find out exactly how much insurance coverage you need by contacting the bank or mortgage lender directly.

It can vary, and the earlier you know, the better you’ll be able to estimate your true housing expenses/mortgage payment.

Of course, what the bank requires might not be enough for your own insurance needs, so be sure to consider both their minimum requirements and your unique insurance comfort level.

Also take the time to shop your policy since it’s one of the few things you can control to some degree.

Consider All the Costs Before You Think You Can Afford It

In summary, make sure you factor in these compulsory expenses, as well as private mortgage insurance if applicable, and any other closing costs that you are required to pay.

Just because you’re in an interest-only mortgage doesn’t mean you can avoid paying your taxes and insurance in full each month (or semi-annually if not impounded).

And even states with cheap housing might have property and insurance costs that are so high they could exceed the principal and interest mortgage payment.

Prior to the housing crisis that played out in the early 2000s, many of these costs were overlooked or ignored when overzealous borrowers bought into homes they later found out they couldn’t afford.

Make sure you do your homework to avoid defaulting on your mortgage or worse, foreclosing and losing your home.

Remember, the ads you see mortgage companies and lenders pitch with the super low monthly payments typically don’t include taxes and insurance.

The takeaway here is that homeownership comes with a lot of costs, not to mention maintenance and any unforeseen repairs that could rear their ugly head once you close and in the years ahead. Be sure you can afford it!

Read more: How much mortgage can I afford?

(photo: Marco Verch)

- Kevin Warsh Throws Cold Water on Lower Mortgage Rates - July 1, 2026

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026

Wait, so property taxes are based on what the market value of your home is? Just because it’s a hot market you’ll be stuck paying a larger amount of tax? I thought they were based on assessed value, which was determined by your city or state. I also thought it was very common for assessed value to be much lower then market value.

Andrew,

In California, the county assessor assigns an assessed value which is the purchase price. So they “assess it” based on what someone paid for it. Whether that’s really assessing is perhaps a debate for another day. A hot market may actually result in a lower tax basis if home prices continue going up after purchase.