Everyone’s heard of the Priceline Negotiator, but what about LendingTree Mortgage Negotiator?

I hadn’t heard about it until last week, when a commercial popped up on my television pitching the new system. I love scrutinizing mortgage companies and their products because they’re often full of hot air.

When it comes down to it, mortgages just aren’t that exciting, and there aren’t many ways to differentiate them, other than via clever marketing tactics.

Still, it sounded interesting, so I decided to take a closer look. From what I remember, LendingTree basically asked for a borrower’s vital information, and then sent it off to a handful of lenders who proceeded to bombard the customer.

The idea was that they would fight for your business, though my guess is consumers didn’t want four banks calling them, let alone one. This was the classic model. Perhaps it’s still in use today, I’m not sure.

Anyway, this is probably why Zillow created its Mortgage Marketplace, which relies on borrower anonymity first and foremost.

How the LendingTree Mortgage Negotiator Works

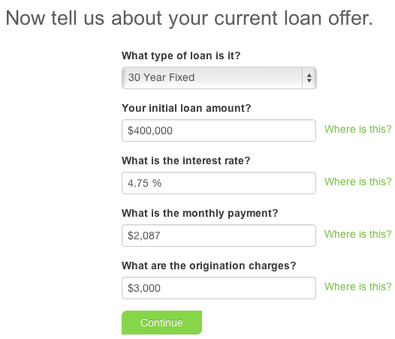

- First you enter in basic home loan details

- Including loan amount, loan type, interest rate

- And what the origination charges are

- The form tells you where to look on your GFE to ensure you enter accurate information

It looks like LendingTree may have learned something from Zillow’s successful pricing model, seeing that their new tool allows borrowers to shop anonymously while using a Good Faith Estimate for accuracy.

To start, you indicate whether the transaction is a purchase or a refinance, and enter in your property and loan information. Pretty standard stuff for a mortgage lead…

However, what makes the form a little bit more robust is that it asks for your origination charges, and even tells you where to find them using your GFE.

In other words, you should have shopped elsewhere before using the Mortgage Negotiator, seeing that you’ll be using the tool to see how your offer(s) stacks up against LendingTree’s mortgage partners.

Once you fill in the loan type, loan amount, interest rate, and origination charges, your data will be analyzed and you’ll be presented with the “best offers” from the company’s lenders.

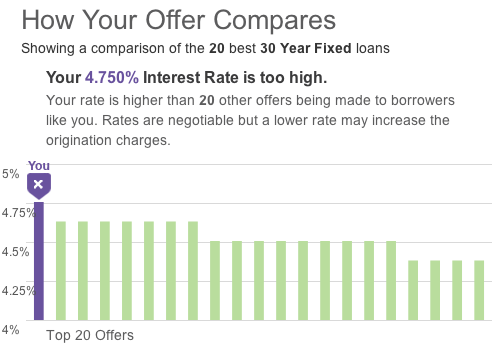

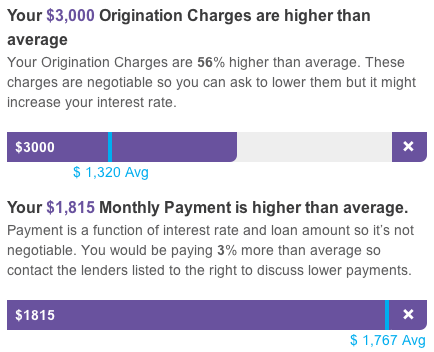

You’ll also be shown how your offer compares to the one associated with your GFE, with the interest rate, origination charges, and monthly payment all shown on a sliding scale.

As you can see from the screenshots below, when I entered a rate of 4.75% for a 30-year fixed and origination charges of $3,000, I was told both were higher than average, compared to what their lenders were offering.

Find Out If Your Mortgage Offer Is Good, Bad, or Ugly

To the right of these comparison boxes, I was shown a list of lenders with corresponding rates and fees.

Of course, these were listed as the “best offers,” and who knows if you actually qualify for the best offer. If your credit score isn’t top notch and your LTV is higher than 80%, the best offers may not be applicable.

So you’ll still have to negotiate with their lenders, assuming you bother contacting them after seeing their rates and fees.

Still, it might be a big improvement from the old system, which probably resulted in a lot of less-than-happy consumers.

I like this trend toward transparency and homeowner education. It’s nice to see companies explain to customers how to read their disclosures so they can accurately compare offers among different lenders.

By the way, their research indicates that only 51% of consumers comparison shop for mortgages, which appears to be up from 40% back in 2010.

Update: LendingTree reached out to me and resolved my credit score concern – borrowers with GFEs most likely had their credit pulled elsewhere, so information is probably entered accurately. The same goes for the LTV ratio being inputted correctly. And the results that appear are in “real time.”

Read more: How many mortgage quotes should you get?

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

- Mortgage Rates Are Having a Good Day as Oil Prices Fall to Pre-War Levels - June 24, 2026

- You Can Still Get a Sub-6% Mortgage Rate, But Is It Worth It? - June 23, 2026

Thanks so much for the review – glad to see you enjoy our new mortgage negotiator tool!