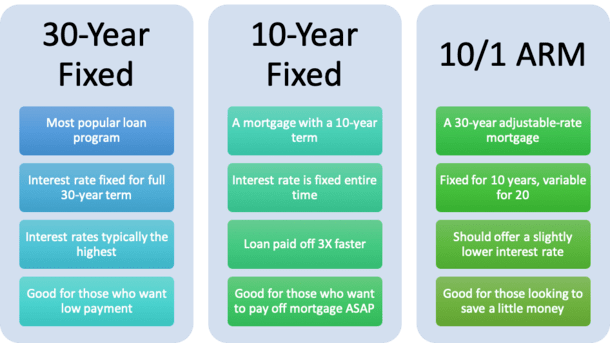

It’s time for another mortgage match-up folks. Today, we’ll look at 10-year mortgages versus the 30-year fixed mortgage to see how these home loans stack up against one another.

My guess is the more 30-year fixed mortgage rates rise, the more consumers will be looking into alternative loan products like these.

But before we get started, it’s important to note that there are two very different types of 10-year mortgages out there.

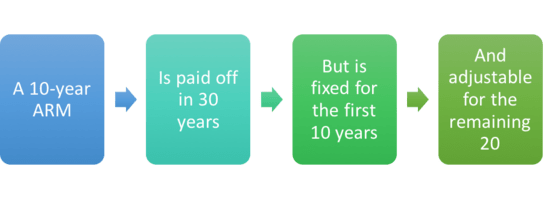

One is a fixed-rate mortgage that is paid off in just a decade, and the other is an adjustable-rate mortgage, which takes three full decades to pay off.

So clearly you need to pay real close attention here to ensure you know what you’re getting yourself into.

Two Very Different Types of 10-Year Mortgages

- There are two types of 10-year mortgages available to homeowners today

- The 10-year ARM (it’s fixed for the first 10 years and adjustable for the remaining 20 years of the loan term)

- And the 10-year fixed-rate mortgage (it features a fixed interest rate for the entire 10-year loan term)

- Be sure you know what you’re actually getting when comparing loan programs

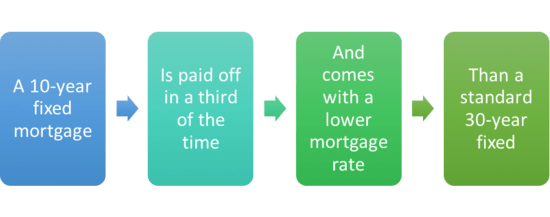

There are 10-year fixed mortgages, which have a mortgage term of 10 years. Yep, just a decade and they are paid off in full.

Then there are 10-year adjustable-rate mortgages, which have a term of 30 years. Huge difference for a number of reasons.

The first type of mortgage is pretty straightforward. It’s similar to a 30-year or 15-year fixed mortgage, only shorter. As mentioned, the loan duration is just 10 years.

What this means, if you happen to be brave enough to go with this loan program, is that your monthly mortgage payment will be quite high since you only get 120 months to pay it off.

After all, if you only get 10 years to pay off your entire mortgage balance, as opposed to 30, you’ll need to come up with some sizable monthly payments to get it down to zero in a hurry.

As such, this loan type isn’t for the faint of heart, nor is it for the borrower with no money in their savings account.

However, 10-year loans will save you a ton of money in interest. And that’s exactly why someone would choose this type of mortgage. To save lots of money!

If you don’t believe me, grab a mortgage calculator and lower the term from 360 months down to 120 months. You’ll be amazed. That doesn’t mean it’s a no-brainer, as I pointed out in my prepay the mortgage or invest article.

And most folks probably can’t even afford such high payments, or simply don’t want to pay down their mortgage that aggressively.

So this type of home loan won’t be an option for the borrower with a low down payment, nor will it likely suit a first-time home buyer.

For example, FHA loans and VA mortgages probably don’t come in this flavor, but it will likely be an option for a jumbo mortgage.

The “other” 10-year mortgage you’ll see out there is the “10-year ARM,” which is fixed for the first 10 years, and adjustable for the remaining 20. Simply put, it’s a 30-year loan with an initial 10-year fixed period.

It can be a 10/1 ARM, which adjusts once annually starting in year 11. Or a “10/6 ARM,” which is fixed for the first 10 years, and adjustable every six months beginning in year 11.

This makes it a hybrid ARM because of its fixed/adjustable nature. It also means the monthly payments have the ability to adjust both higher and lower once those first 10 years are up.

We’re basically talking about two loan products on opposite ends of the spectrum.

One that pays down the entire home loan balance in a third of the time (typically it takes 30 years), and one that’s an ARM, which some consider higher-risk than traditional fixed mortgages.

So, are either loan programs a better choice than the classic 30-year fixed mortgage when buying real estate? Let’s see.

10-Year Fixed Mortgages Only Last Ten Years

- A 10-year fixed mortgage only lasts for a decade

- It is paid off in full in that time but monthly payments are very high

- You only get a third of the usual time to pay off you home loan

- While payments are steep, you can save a ton of money and be free and clear in no time!

If you’re really, really serious about paying off your mortgage fast, the 10-year fixed could be the loan for you. You’ll gain home equity hand over fist in no time at all.

Just note that your mortgage payment will be huge relative to other, more traditional options that give you more time to pay off your balance.

If you have student loans and credit card debt, you may want to go with something a little more conservative. So use an affordability calculator first to determine if you can qualify, let alone handle the payments.

For example, on a $250,000 loan amount, a 10-year fixed mortgage with an interest rate of 3% would come with a monthly mortgage payment of $2,414.02.

Compare that to a monthly payment of $1,787.21 on a 15-year fixed at 3.5%, and a payment of $1,193.54 on a 30-year fixed at 4%. It’s about double the 30-year payment.

Notice how I even factored in the lower mortgage rate afforded to the 10-year fixed and 15-year fixed and the payment is still significantly higher.

Well, while the payment on the 10-year fixed is quite a bit higher, you’d only pay about $40,000 in interest over those 10 years of loan repayment.

On the 15-year fixed, you’d pay about $72,000 in interest, and on the 30-year fixed you’d pay nearly $180,000 in total interest. Yes, you read that right. Nearly five times the amount of interest versus the 10-year loan!

This illustrates why someone would opt for the shorter term 10-year fixed. A lower mortgage rate and much less interest paid.

And a home purchased with one of these loans will be free and clear much more quickly, if that’s your goal or you’re close to retirement.

Speaking of, it could be a good choice for the homeowner who got a late start, as a means of playing catch-up.

But it only makes sense if you really want to pay off your mortgage fast, and have the means to do it without breaking the bank.

10-Year Fixed Mortgage Rates Are Lower

- Another advantage of a 10-year fixed is the lower interest rate

- They are cheaper than 15-year and 30-year fixed mortgages

- How much cheaper may depend on the bank/lender in question

- Perhaps .25% lower than a 15-year fixed and .75-1.00% lower than a 30-year fixed

Speaking of interest rates, let’s talk about what you might expect to receive on a 10-year fixed loan.

First, not all lenders offer the program. It’s somewhat of a specialty loan program, so be sure to ask about it specifically when speaking to a loan officer or seek it out directly when comparing current mortgage rates.

It’s certainly not as common as a 30-year or 15-year fixed. So once you find a lender that does offer the loan, you might see that 10-year mortgage rates are an .125 (eighth) better than a comparable 15-year fixed. Maybe a quarter lower…

| Loan Type | Mortgage Rate |

| 10-Year ARM | 6.25% |

| 10-Year Fixed | 5.625% |

| 15-Year Fixed | 5.875% |

| 20-Year Fixed | 6.00% |

| 30-Year Fixed | 6.50% |

In other words, if the 15-year fixed is priced at 5.875%, the 10-year fixed mortgage rate might be offered at 5.625% or 5.75%. It’s not going to be a huge difference.

Some mortgage lenders may not even price the two types of loans differently. The only difference might be lower closing costs on the 10-year fixed.

Meanwhile, a similar 30-year fixed might go for 6.50%, so you’re looking at about a .75% discount, more or less. That’s pretty significant.

Tip: The difference between a 15-year fixed mortgage rates and 10-year fixed mortgage rates may be marginal or even nil.

So taking the longer term on the 15-year fixed could provide you with some much needed breathing room. You can always make larger payments each month to pay it down quicker.

10-Year Fixed Mortgage Pros and Cons

The Good

- Pay off your mortgage in just 10 years!

- Get a lower interest rate than a 15-year or 30-year fixed

- Pay much less interest over the shorter loan term

- More of your monthly payment goes toward principal balance

- Own your home much faster

- Could be a good choice for a home buyer who got a late start

The Bad

- Monthly payments will be much higher

- May not qualify for an expensive home

- May limit your purchasing power

- Could get into payment trouble if your income drops

- Your money might be better served elsewhere

10-Year ARMs Are a Different Beast

- A 10-year ARM is an adjustable-rate mortgage

- It is fixed for the first 10 years and adjustable for 20 years

- It has a 30-year loan term just like a 30-year fixed

- But is subject to annual or biannual rate adjustments after the first 10 years

Here’s where things can get confusing, or even misleading. Some mortgage companies advertise 10-year ARMs as if they’re fixed mortgages, which just isn’t the case. Or at best half the story.

They basically use that initial 10-year fixed period to their advantage when putting together marketing materials. But they’re not 10-year loans. They are 30-year loans, end of story.

In the case of a 10/1 ARM, the loan is fixed for the first 10 years and adjustable for the remainder of the 30-year loan term (20 years). It can adjust once per year.

Its cousin the 10/6 ARM works the same way, except the loan adjusts twice per year for the 20 years it is adjustable.

Mortgage lenders can make 10-year ARMs appear more attractive to homeowners by touting the lower interest rate that accompanies them.

After all, an ARM will pretty much always be priced lower than a 30-year fixed mortgage because they will eventually become adjustable.

So you can see why a customer may think the 10-year ARM is the better choice hands down.

But the fact of the matter is that these loans are still adjustable-rate mortgages in fixed-rate clothing.

And when it comes down to it, they generally aren’t that much cheaper than a traditional 30-year fixed because they’re fixed for a full decade.

10-Year ARM Rates May Come at a Slight Discount

- While interest rates will vary over time and by mortgage lender

- Expect a 10-year ARM to price slightly below a comparable 30-year fixed

- Perhaps just .125% to .25% cheaper in rate depending on the company

- The discount is marginal because 10 years is still a long time to offer a fixed interest rate before the first adjustment

- Most mortgages are only kept for 10 years, despite being 30-year loans, so lenders price them almost the same

Now let’s discuss 10-year ARM rates, which generally come cheaper than 30-year fixed rates.

However, the interest rate may only be .125% or .25% cheaper because you get a fixed rate for a full decade before any adjustment takes place.

Many folks don’t even stay in the same home or keep their mortgages for a decade, so the 10/1 ARM or 10/6 ARM could make sense and save you some dough with little to no downside.

However, this also explains the lack of a large discount relative to the 30-year fixed.

If you’re not comfortable with a loan program that features adjustable rates, steer clear. The savings may not be worth the stress.

Assuming you plan to move within 10 years (or refinance your mortgage for some reason), going with a 10-year ARM should provide you with a discounted fixed rate for a significant period of time while you figure things out.

Of course, if you know you won’t stay even five years, it could be even smarter to look to the 5/1 ARM instead, which will come with an even lower interest rate.

Tip: Some local credit unions offer bigger discounts on 10/1 ARMs (and 10/6 ARMs) so put in the time to shop around if you’re interested in this type of loan. The savings can be significant.

For example, LAFCU out of Lansing, Michigan was recently offering a 10/6 ARM priced at 1.25% below the 30-year fixed rate.

10-Year ARM Pros and Cons

The Good

- Lower interest rate than a 30-year fixed

- Long fixed-rate period (120 months)

- Most homeowners move or refinance in less than a decade’s time anyway

- So you may never actually have to face an interest rate adjustment

The Bad

- The interest rate may not be much cheaper than a 30-year fixed

- Rate can adjust higher after 10 short years

- Could face payment difficulty if rates adjust significantly higher

- Or be forced to refinance at unfavorable terms if rates rise during that time

In summary, pay close attention to these very different loan types so you know which type of 10-year mortgage you’re actually getting…

Read more: 30-Year Fixed Mortgage vs. ARM

- UWM Launches Borrower-Paid Temporary Buydown for Refinances - July 17, 2025

- Firing Jerome Powell Won’t Benefit Mortgage Rates - July 16, 2025

- Here’s How Your Mortgage Payment Can Go Up Even If It’s Not an ARM - July 15, 2025