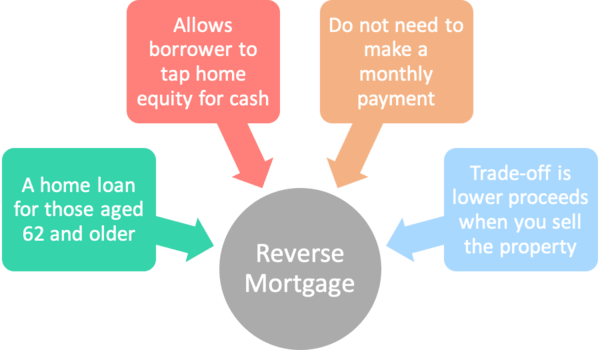

A “reverse mortgage” is a tax-exempt home loan that allows a homeowner to take cash-out of their home using their existing home equity, without taking on a monthly payment or having to sell their property.

These types of mortgage loans are only available to homeowners aged 62 or older, who occupy a property as their principal residence.

Eligible property types include single-family homes, condominiums, townhouses, and even manufactured homes built after June 1976.

Additionally, multi-unit properties are permitted, including duplexes, triplexes, and fourplexes (1-4 unit properties) as long as you occupy one of the units as your primary residence.

Reverse mortgage loans come with a variety of terms, including both fixed and variable rate plans, and with varying associated fees such as loan origination fees and servicing fees, as well as other closing costs.

With a fixed-rate reverse mortgage, you need to take your loan proceeds as a lump sum. With a variable-rate reverse mortgage, you get the option of taking your proceeds as a monthly payment, line of credit, or lump sum.

How a Reverse Mortgage Works

- It’s similar to a “forward mortgage”

- In that you borrow money from the bank

- But with a reverse mortgage you don’t have a monthly payment

- Nor does the loan need to be paid back

A reverse mortgage works in quite the opposite way of a traditional mortgage, allowing a homeowner with accrued equity in their home to pull cash out on a monthly or lump sum basis with no associated payment.

The borrower can then use the loan proceeds for any expenses they wish, such as home improvement, medical costs, or simply to pay off existing everyday bills or property taxes.

Like a normal home loan, you can only pull out equity to a certain limit, but instead of a loan-to-value ratio (LTV), this max amount is known as the principal limit factor (PLF). It is based on your age, your equity (home value minus current loan balance), and current interest rates.

In general, you need a substantial amount of home equity in order to get a reverse mortgage loan. If you’ve already got a mortgage on the property and not much of it is paid off, it probably won’t be a viable solution.

Conversely, if your home is free and clear, or you’ve got plenty of equity, it could be a practical way to tap into it.

In order to qualify, you will need to have your income, assets, and credit history verified, as you would any typical mortgage. And as noted, you need to occupy the property as your primary residence.

The main benefit of a reverse mortgage is that executing one won’t result in a monthly mortgage payment, as you’d find with a typical mortgage. And to the same effect, the loan never has to be paid back*, as it simply depletes the equity in your home.

*Once you move out of your home, you must pay back the loan plus interest and any other fees to the mortgage lender, but the remaining equity will be yours, and the debt can never exceed the value of your home. At least, that’s the theory.

Interest from a reverse mortgage may be tax deductible, but not until the loan is paid off in part or in full.

A homeowner might choose a reverse mortgage because they’re unable to qualify for a traditional, forward mortgage, due to a lack of employment and/or income.

Reverse Mortgage Alternatives

- Be sure to explore other home loan options

- Such as an asset-based mortgage

- Or a home equity line of credit

- If you need cash but are able to make monthly payments

Most home loan programs qualify borrowers by using their job history and income, something elderly homeowners may not have if they’re retired. They may have retirement accounts, pensions, and social security, but that might not cut it.

An alternative would be an asset-based loan that amortizes your assets over the loan term. These are actually backed by both Fannie Mae and Freddie Mac, not some fly-by-night lender.

Perhaps a better idea is to secure a home equity line of credit (HELOC) shortly before you retire, which you can typically draw upon for a decade before having to repay it. During the first 10 years, you generally have the option of making interest-only payments as well.

Chances are you might not even need it, and can just set aside the line of credit as a lifeline in case something does come up.

There are three types of reverse mortgages:

– Single-purpose reverse mortgages

– Federally-insured reverse mortgages (HECM loans)

– Proprietary reverse mortgages

Single-purpose reverse mortgages are generally offered to lower-income homeowners by non-profit organizations and local government agencies.

They allow a homeowner to use the proceeds for one single purpose as the name suggests, usually to payoff property taxes or for home improvements. They have low associated fees, but are limited in their offerings.

A federally-insured reverse mortgage, otherwise known as a Home Equity Conversion Mortgage (HECM loan) is less restrictive than a single-purpose reverse mortgage, though it has higher associated costs. These are by far the most popular reverse mortgages out there.

This type of mortgage is backed by the U. S. Department of Housing and Urban Development (HUD) and requires the homeowner to meet with an independent government-approved housing counselor. But any HUD-approved reverse mortgage lender can originate HECM loans.

The housing counseling will cover HECM program eligibility requirements, the financial implications of obtaining a HECM reverse mortgage, repaying the loan, and alternatives. These HECM counselors will also discuss when the mortgage becomes due and payable.

Homeowners can use this type of reverse mortgage for any purpose, or multiple purposes, and can select how they want to receive the money. HECMs will carry the same interest rates regardless of lender, but the closing costs and servicing fees can vary, so make sure you shop around.

The HECM FHA mortgage limit for 2025 is $1,209,750 and the HECM origination fee is capped at $6,000.

The HECM loan includes mortgage insurance premiums (both upfront and annual ones), third-party fees, an origination fee, interest, and servicing fees.

Mortgage lenders are able to charge a monthly servicing fee of no more than $30 if the loan is fixed or annually adjustable, or up to $35 if the interest rate adjusts monthly.

Finally, a proprietary reverse mortgage is similar to a Home Equity Conversion Mortgage, though they are privately-backed loans and usually the most expensive. They can provide more money up front than a HECM, but the initial credit line will not grow over time like a HECM.

With a HECM or proprietary reverse mortgage, a homeowner can elect to receive the money as a line of credit they can draw upon, in monthly installments, or as a combination of the two.

Reverse Mortgage Repayment

A reverse mortgage must typically be repaid in full when one of the following events takes place:

– You fail to pay property taxes or homeowners insurance (or even HOA dues!)

– You permanently move to a new principal residence.

– You, or the last borrower on the loan, fail to live in the home for 12 successive months.

– You allow the property to deteriorate without making the necessary repairs.

In other words, it’s possible for the borrower(s) to lose their home with a reverse mortgage, which is one of the main negatives and sources of controversy. The AARP has been a well-known critic.

This is even more contentious since it involves the elderly and potentially a widower. This can also complicate one’s inheritance, so it’s a weighty decision.

Reverse Mortgage Pros and Cons

There are pros and cons to reverse mortgage loans, like any other loan program out there.

While you don’t have to move out of your home if you take out a reverse mortgage, there are plenty of stories of elderly homeowners losing their properties for failure to pay property taxes and homeowners insurance.

Taking one out also means you leave less to your heirs, assuming your plan is to leave money and/or a house behind for loved ones.

So be sure you fully understand all the consequences before going the reverse mortgage route.

The Good

- Can access equity in your home without a monthly payment

- Good for someone with limited income

- Or someone unable to qualify for a cash-out refinance

- The money is tax-free since it’s simply loan proceeds

- Can stay in your home if you wish to keep it

The Bad

- Depletes your home equity

- Less or nothing is left over for your heirs

- Non-borrowing spouse and/or children at risk of losing home if/when you pass

- Reverse mortgage could be deemed payable in that event

- Could lose home to foreclosure when it comes due

- May also lose home if you fail to pay taxes/insurance/HOA dues

- Or properly maintain the property

Make sure you use a reverse mortgage calculator to compare all the available programs to see which will work best for you.

Beware of companies that masquerade as pubic sector or non-profit organizations offering reverse mortgage advice. While they may appear to be government backed agencies, many are simply just banks or mortgage lenders pushing consumers to execute a reverse mortgage, whether it’s in their benefit or not.

can we get a reverse mortgage if we live in an over 55 community? the house is fully paid for, but we don’t own the land?

Dawn,

That sounds like a tricky one…you may want to reach out to some reverse mortgage lenders (or brokers) to explain the scenario in detail.