If you’re a doctor, resident, or even a veterinarian, getting a mortgage can be a little bit easier thanks to so-called “physician mortgages” offered by most major lenders.

Just about every bank offers a special mortgage program for doctors, including large commercial banks like Bank of America and small local credit unions as well.

The names of these programs, along with the guidelines and perks, will vary from bank to bank. They’re typically not heavily advertised, so you may have to do some digging to find all the details.

But they all seem to have two things in common; large maximum loan amounts and high loan-to-value ratios (LTVs).

My assumption is lenders are keen to offer these loans to future doctors because they’ll be good clients with lots of assets, ideally kept with the bank. In fact, you may need a prior banking relationship to get approved.

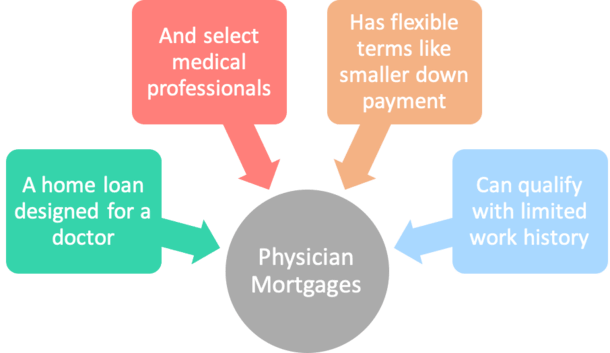

What Is a Physician Mortgage?

- A mortgage designed specifically for doctors, residents, fellows, and interns

- As well as dentists, orthodontists, pharmacists, and veterinarians

- Offers more flexible underwriting like higher loan amounts and LTVs and no mortgage insurance

- Applicants can get approved regardless of medical school debt and/or limited employment history

In a nutshell, a “doctor mortgage” is a home loan designed specifically for physicians that offers flexible underwriting guidelines and unique features a traditional mortgage loan may not offer.

But we’re not just talking medical doctors (MDs). These loan programs are often available to a wide range of disciplines, including dentists, orthodontists, veterinarians, ophthalmologists, and even pharmacists and lawyers.

If you have any of the following licenses, you might be able to take advantage of one of these specialty programs:

– MD

– DO

– DDS

– DVM

– DMD

– OD

– DPM

– PharmD

Additionally, you can often be a resident, fellow, intern, or practicing physician to qualify. So they’re pretty flexible in terms of where you’re at in your career.

This is especially true if you’ve yet to start a new job, but have an employment contract in hand.

Banks and lenders know you’ve got a lot of earnings potential if you’re going to be a doctor, even if you don’t have the down payment funds necessary to buy your first home. Or even the pay stubs to document your income.

It’s a common problem, thanks to the high cost of medical school, and the fact that doctors, like anyone else in school, don’t get paid the big bucks until they’ve completed their training.

Instead of saving for a down payment, these individuals might be busy paying off costly student loans.

Compounding this is the fact that someone who will be highly compensated in the near future might be looking at a very expensive home purchase.

This explains why physician mortgage programs tend to allow for higher loan amounts than typical loan programs, along with higher LTVs. Those are certainly the two main distinctions.

Doctors Can Get a Mortgage with No Money Down

- Physician mortgages come with flexible terms including low and no-down payment options

- And often allow for very large loan amounts to suit home buyers at all levels

- This is necessary because doctors tend to purchase very expensive properties despite being green in their career

- These tailored programs can make it easier to get approved for a home loan without additional scrutiny

Many of these programs allow doctors to get a mortgage with no money down, something most individuals can’t readily take advantage of unless they’re a veteran or buying in a rural area.

You might see something like 100% financing up to $750,000 or $850,000 loan amounts, and just 5% down for $1 million-dollar loan amounts, assuming you have a decent credit score.

That’s a non-conforming loan amount (jumbo) with zero down payment requirement. Good luck finding that elsewhere.

Additionally, doctors might be able to get that level of financing without private mortgage insurance (PMI), which is typically required for a loan amount above 80% LTV.

The hitch is that even if PMI isn’t explicitly required on high-LTV mortgages, it’s generally just built into the rate.

So instead of say a mortgage rate of 3.75%, you might pay 4% instead. You’re just charged a different way.

These Lenders Understand Your Employment Situation Better

- Banks and lenders that specialize in physician mortgages will be better equipped to get you approved

- They should have an easier time navigating your unique financial and employment situation

- This could mean a faster loan process and one that is more likely to make it to the finish line

- Conversely you might run into trouble with conventional lenders that aren’t familiar with how doctors get paid

Another perk is that the bank or lender (or credit union) offering this type of loan should have a better understanding of your situation.

After all, they’ve done it before, likely hundreds or thousands of times, so they should know how to navigate the process.

Instead of wondering what documentation they’ll need to get your loan approved, they’ll likely be familiar with paperwork requirements and the handling of student loan debt when it comes to your DTI.

Ideally, this means you’ll stand a better chance of getting approved for a mortgage with fewer snags or gotchas.

This can be really important if you’re relocating to a new city and trying to nail down living arrangements, especially in a competitive housing market.

Doctor Mortgage Loan Programs

- Home purchase and refinance loans

- Available on primary residences and second homes

- Single-family residences, multi-unit properties, condos/townhomes

- Fixed-rate options: 30-year, 20-year, 15-year, etc.

- Adjustable-rate options: 5/1, 7/1, 10/1, etc.

- Interest-only options to maximize cash flow

As far as loan options go, just like normal mortgages you can get a fixed-rate loan or an ARM on a home purchase or a refinance.

So if you want to play it safe with a 30-year or 15-year fixed, no problem. But if you want to save some money, an adjustable-rate mortgage could also be an option.

Some doctors may favor ARMs because of the lower monthly payment, and the fact that they may sell or refinance before the initial fixed period ends.

For example, you might buy a starter home before upgrading a few years later, all while the interest rate is fixed if it’s a 5/1 or 7/1 ARM.

And if the terms of a physician mortgage aren’t as attractive as a typical mortgage, it might make sense to go with an ARM early on.

After all, you might move up to an even larger home once you’re more established. Or you could relocate to a different city for a new position.

Perhaps you’ll be able to pay down a large chunk of your mortgage balance early, making the type of loan you go with less significant.

Consider that when deciding if mortgage points are worth it because you might not keep your loan long enough to justify the upfront front.

Minimum Down Payment for a Physician Mortgage

- 100% financing on loan amounts up to $750,000

- 95% financing on loan amounts up to $1 million

- 90% financing on loan amounts up to $1.5 million

While these programs can certainly vary from lender to lender, there seems to be a somewhat standardized down payment structure.

From what I’ve seen, the tiers above are the most common requirements for these types of loans.

Generally, you can get a no down payment loan up to $750,000, and 5% down for loan amounts to $1 million.

At $1.5 million, you might be required to put down 10%, depending on the lender in question.

The main difference between banks might be maximum financing, with certain banks allowing much higher loan amounts than others. Or some offering up to $1.25 million with just 5% down payment.

Be sure to put in the time to shop around if you’re buying a super expensive home, as these minimums and maximums range quite a bit.

Which Banks Offer Doctor Mortgages?

As noted, just about every major bank out there has a program suited specifically to doctors and other medical professionals.

The same goes for independent mortgage brokers, who may be partnered with wholesale lenders that offer these programs.

Chances are your financial planner will have a referral or send you in the right direction. Just be sure to look beyond their preferred vendor…

In terms of specific banks, I’ve listed several below to give you an idea of qualifying criteria and options.

For example, Bank of America can close 90 days before you start a new job if you’re a resident or a fellow.

BMO Harris offers flexible debt-to-income underwriting guidelines for physicians and no income history requirement (proof of future income is required).

Fifth Third Bank allows established physicians and dentists to finance up to $750,000 with no down payment when purchasing or refinancing a home loan.

And Guild Mortgage will exclude student loan debt while allowing a max DTI ratio of 43%.

Huntington Bank allows 90% financing up to $2,000,000 if you have an active employment contract with proof of sufficient income and reserves.

KeyBank will go all the way up to $3.5 million loan amounts, and eligible property types include owner-occupied primary residences and second homes.

There’s also Northpointe Bank, which offers purchase and rate/term refinance loan amounts up to $1,000,000 with zero down options available.

Both Regions Bank and Ruoff Mortgage pitch the no down payment and no PMI requirement, both of which are more flexible than standard loan programs.

Meanwhile, a TD Bank Medical Professional Mortgage can consider your overall earning potential while ignoring certain student loan debt to sidestep DTI constraints.

Finally, the Union Bank Doctor Loan Program allows loan amounts as high as $5 million if you want your dream house today instead of later.

And they offer interest-only adjustable-rate options if you’re looking to maximize cash flow and put your money to work elsewhere.

Be Sure to Consider Traditional Mortgage Options Too

- You don’t necessarily need a physician mortgage if you’re a doctor

- Traditional loan programs could be perfectly suitable and cheaper

- Explore all home loan options to ensure you don’t miss out on a better deal

- A direct lender or mortgage broker might offer a lower mortgage rate than the big banks

It should also be noted that the more flexible guidelines associated with a doctor mortgage don’t come free of charge.

While the lender is probably happy to offer financing to a well-qualified borrower with excellent earnings potential, they will often charge a higher interest rate in exchange.

Once you are able to pay down your mortgage, it could make sense to look into refinancing to a traditional mortgage, especially if your LTV is low enough to avoid mortgage insurance and most pricing adjustments.

These loans typically do not have a prepayment penalty, so you should be free to refinance almost immediately.

If you’re paying down a mortgage at 95% or 100% LTV, chances are you’re paying a lot more in interest than you otherwise would with a lower LTV mortgage, such as one at 80% or less.

Also be sure to shop both traditional and physician mortgages to determine which is the better option.

You might not need to get a mortgage via one of these special programs if you have down payment funds available, or even a gift for down payment from a relative.

Doctor Mortgage Loans in Review

- Can be a resident, fellow, practicing physician (or even a veterinarian, dentist, pharmacist, or lawyer)

- Ability to obtain financing before your job starts and use projected income

- Can be a purchase or a refinance, sometimes second homes permitted

- Multi-unit properties and condos/townhomes should be OK

- Allow for large loan amounts (up to $1.5 million+)

- Often do not need a down payment for loan amounts up to $750,000

- Typically do not charge private mortgage insurance (PMI)

- Flexible qualifying guidelines with regard to student loans and DTI

- Generally need good credit (720+) to qualify

- Both fixed and adjustable-rate options available (sometimes interest-only)

- Mortgage rates may be higher than traditional loans

- Banks may require you to open a checking/savings account

- Also consider a mortgage broker who may be able to link you with a wholesale lender

- Mortgage Rates Narrowly Avoid New 52-Week Highs as Bond Yields Surge Higher - July 31, 2026

- Trump Says Warsh Wants Lower Interest Rates, But Has a Political Board - July 30, 2026

- Do Mortgage Rates Need a Hike to Move Lower? - July 28, 2026