A company called Point wants to give you “early access to your home equity” without ever having to make monthly payments, similar to how a reverse mortgage works.

While at first glance it sounds pretty good, you’ve got to dig into the details to see what you’re actually getting.

Ultimately, you’re sharing your future home price appreciation with the company in exchange for a piece of the action today.

Let’s learn more about how it all works to determine if it might be a better alternative to a traditional home equity loan or HELOC.

How Point Works to Tap Home Equity

- Point makes an investment in your home in exchange for cash today

- No monthly payments are made during the 30-year loan term

- You pay back their investment at any time via sale, refinance, etc.

- Buyback cost includes amount originally received plus portion of your home’s appreciation

Instead of taking out a loan to access your home equity, Point “invests” in your property via a Home Equity Investment (HEI) and gives you cash today for some of that sweet, sweet home appreciation tomorrow.

Like a traditional first or second mortgage, you need to answer the usual questions like how much you make, what your home is worth, and what your credit scores are.

They say you can pre-qualify for Point in less than two minutes, then you’ll be presented with a pre-offer to see how much you can borrow. Funds can be received in as little as 15 days.

Their investments range from $35,000 to $350,000, though they can exceed that max in some cases.

The amount of money you receive will depend on your available home equity, with 20% of your home’s value generally the limit.

Additionally, you’re required to have at least 20% equity after the Point investment. In other words, the max CLTV is 80%.

Once you proceed with the application, they’ll pull your credit and order a third-party home appraisal to determine your property’s starting value.

The appraisal is key in determining how much you can borrow, and also how much Point will receive when you eventually repay them.

How Much Does Point Cost?

- While there are no monthly payments to worry about

- You do pay anywhere from 3-5% at the outset as a transaction fee

- And they share in the upside value of your home over time

- Total cost will vary based on how much your property appreciates and when you pay them back

As noted, there are no monthly payments associated with the Point investment, nor is there an associated interest rate because it’s not a loan.

However, they do charge a transaction fee of anywhere from 3-5%, which is deducted from your proceeds along with an appraisal fee and escrow fee. Think of it as an origination fee, similar to what Figure charges.

They say your specific offer is determined by “special pricing equations,” which I assume takes into account things like your credit score, DTI ratio, LTV ratio, housing market expectations, how you plan to pay them back, etc.

My guess is it’s similar to a typical mortgage rate in that the less risk you present, the better the terms will be.

How Do You Repay Point?

This is an important question seeing that you don’t have to make monthly payments via their investment in your property.

As noted, Point’s investment comes with a 30-year term, just like most mortgages. At any time, you can pay them back via several different methods, including:

- Home sale

- Cash-out refinance

- HELOC or home equity loan

- Another source of funds

When you’re ready to pay Point back, they rely upon the sales price if you sell the property, or in the case a refinance, the appraisal, AVM, or a broker price opinion (BPO).

If the term is up and you don’t want to sell, you can buy Point out using the appraised fair-market-value.

Or you can pay off their investment with another source of financing, such as a home equity loan, HELOC, or a reverse mortgage.

That’s the easy part. Determining how much you owe is a different story. For one, the appraised value isn’t the starting point.

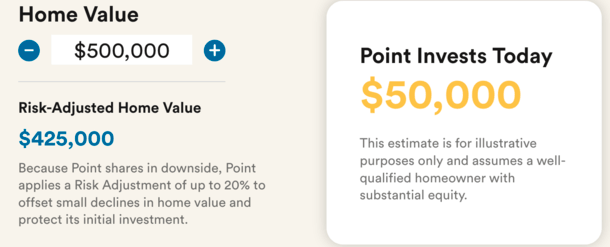

Instead, they use a “Risk-Adjusted Home Value,” which can be as much as 20% of the appraised value to account for the decline in home values to protect Point.

In the example on their website, they use a home valued at $500,000 with a Risk-Adjusted Home Value of $425,000, as seen above.

They give the homeowner $50,000 payment-free in exchange for 20% of their future appreciation, using that Risk-Adjusted Home Value.

This value can range based on borrower and property profile, as determined by their underwriters.

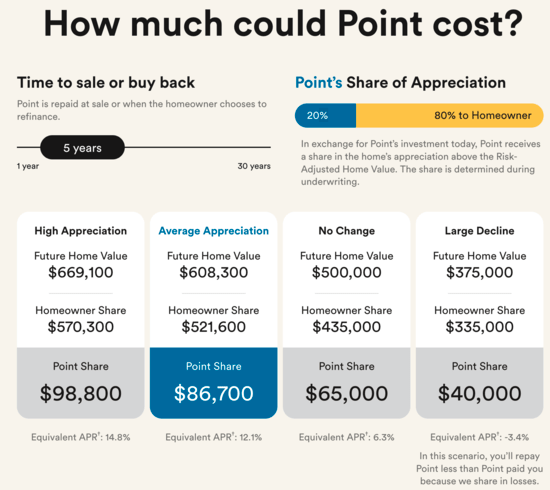

Anyway, as you can see, how much Point takes will vary based on when you sell or buy back your equity, and how your property value fares during that time.

One negative is you’re basically already in the hole thanks to the Risk-Adjusted Home Value. Even if home prices were flat after five years, you’d owe $15,000 on that $50,000 investment.

And you have to factor in the fees taken from your initial investment as well.

If your property saw “average appreciation” and rose to $608,300, you’d wind up with a share of just $521,600, while Point would get $86,700.

They’d get 20% of the $183,300 rise in value from the Risk-Adjusted Home Value, or roughly $36,700, plus their $50,000 original investment back.

Simply put, the more your home value increases, the more Point makes, and the less you get in a sale.

However, Point is also taking a risk if the property decreases in value because they will share in losses. If the home somehow manages to drop in price to $375,000, Point would only receive $40,000.

That 20% loss based on the $425,000 Risk-Adjusted Home Value means they give up $10,000 of their original $50,000 investment.

Who Qualifies for a Point Home Equity Investment?

- Home must be located in an eligible area and valued above $200,000

- Must have 20% of your home equity after Point’s investment

- Requires a credit score above 500

- Owners of single-family residences, condos/townhomes, and multi-unit properties may qualify

Point says it invests in most types of residential real estate, including single-family residences, condos, townhomes, and multi-unit properties (1-4 units).

Additionally, they allow title to held by individuals, in trusts, and by LLCs, the latter two being subject to their approval.

Unfortunately, Point is unable to invest in the following types of properties:

- manufactured homes

- mobile homes

- properties with 5 or more units

- tenants-in-common (TiC) properties (unless owners are immediate family members)

Speaking of title, Point isn’t added to the title of your property, and you retain sole ownership. However, their investment is secured by a Deed of Trust and a Memorandum of Option.

Homeowners must have credit scores above 500, which is very low, and must retain 20% home equity after Point’s investment. In other words, you need to be fairly equity rich.

Additionally, your property must be worth at least $200,000 and located in an eligible area.

Where Is Point Available?

At the moment, Point isn’t available nationwide, but they are working to expand to new regions of the country.

Currently, the service is live for homeowners in select areas of:

Alabama

Arizona

Arkansas

California

Colorado

Connecticut

Florida

Georgia

Idaho

Illinois

Indiana

Iowa

Kansas

Kentucky

Maryland

Michigan

Minnesota

Montana

New Jersey

New Mexico

North Carolina

Ohio

Oklahoma

Oregon

Pennsylvania

South Carolina

Tennessee

Texas

Utah

Virginia

Washington

Wisconsin

They expect to bring Point to more homeowners in coming months, and ask that you contact them if you’re interested and outside their present service area.

Point vs. a Reverse Mortgage

- No minimum age requirement

- Not a loan and does not accrue interest

- Can be in first lien position or junior lien

- Can’t be underwater because Point shares in losses

- Point agreement is assumable by heirs

As I noted earlier, Point works kind of like a reverse mortgage in that you’re able to tap your home equity without having to make payments.

However, there is a no minimum age to use Point, which differs from the 62+ age requirement to take out a reverse mortgage.

Additionally, Point’s HEI isn’t a loan, nor does it charge interest. To that end, they also say you’ll never wind up in an upside-down position on your investment from Point because they share in losses.

A reverse mortgage also requires a first lien position, whereas Point’s investment can be subordinate to existing loans.

Lastly, Point’s investment is assumable, unlike a reverse mortgage, so your heirs could potentially assume your Point agreement.

Who Is Point Actually Good For?

If you’ve read how Point works above, you’re aware it’s a pretty unique way of tapping equity. The company even says it themselves.

On their website, they note that “homeowners who aren’t a good fit for a traditional home equity product” may turn to Point to get their finances in order.

Then once their situation improves, they might obtain more traditional financing that can be used to pay back Point.

The biggest downside to Point is that you’re giving them a sizable chunk of your future home price appreciation, even if you don’t have to make monthly payments on the quasi-loan they give you.

For me, wealth creation is one of the best parts of homeownership. It’s a big reason why people invest in real estate.

Point can take between 25-40% of future appreciation, so it could be a very big price to pay. However, there are situations where Point may make sense.

For someone deep in debt, the lack of monthly payments will be helpful. Point might also be a viable option if unable to qualify for other home equity products and in need of cash.

Additionally, the Point investment doesn’t show up on your credit report, nor does it increase your debt load.

So for someone between a rock and a hard place, it could provide some relief, but be sure to do the math and explore more traditional alternatives like home equity loans, HELOCs, a cash out refinance, and more.

Update: Point now operates as a full-service mortgage lender, offering purchases and refinances, including conventional, FHA, USDA, and VA loans.

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

- Mortgage Rates Are Now Higher Than They Were a Year Ago - August 5, 2026

- Chase Is Advertising Mortgage Rates With Nearly Two Discount Points to Keep Them Looking Attractive - August 4, 2026

Could a home equity investment could be an alternative to a transition bridge loan? In the relatively short term of a housing transition, the equity is the original home would not likely rise dramatically.

The investment does not charge interest, there are no payments, and the money is not due for 10 years; but it has some steep up-front costs. The bridge loan does charge interest or collect payments. It has some up-front costs. It also has a short payback time.

To add another consideration when working with Point is that they frequently run out of funds and push closing back months to budget out their expenses.

Can you take out a home equity loan if needed in the future if you are part of this program .we will be closing next month on in nj. $324,000 cash deal . Could we start the process?