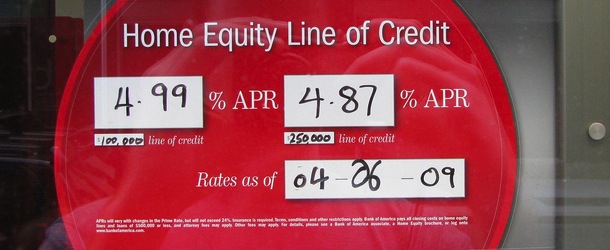

Several years ago, when the mortgage crisis first materialized, an interest rate reset chart from Credit Suisse began circulating on the Internet.

The picture said more than a thousand words – it essentially foretold disaster for the housing market, and it largely delivered.

Fast forward to 2013, and you’d think we’d be out of the woods, seeing that the chart was from all the way back in 2007.

But there is yet another wave of resets on the horizon, and this time it’s home equity lines of credit (HELOCs).

More 10-Year Draw Periods End in 2014

Most HELOCs are designed so a homeowner can draw from the line of credit for the first 10 years, and then pay back the balance during the following 15 years.

To further accommodate homeowners, the initial 10-year draw period allows for interest-only payments. And people tend to like to make smaller payments.

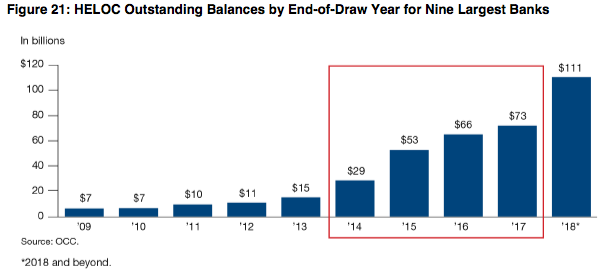

Per a new report from Fitch Ratings titled, “U.S. Banks – Home Equity ReSet Risk Hitting the ReSet Button in 2014,” home equity lending surged in 2004 as credit conditions eased and home prices shot higher.

The screenshot above from the OCC’s Fall 2012 Semiannual Risk Perspective illustrates that (it actually gets worse in later years).

According to Fitch, HELOCs outstanding increased 42% in 2004, and home prices still aren’t back to 2004 levels in many areas of the country.

In other words, most borrowers who still have their HELOCs will have a difficult time refinancing out of them.

And borrowers are essentially hit with two payment increases. For one, they must make principal and interest payments, as opposed to paying interest-only.

Additionally, the amortization period drops to just 15 years. So if you only paid interest for the entire draw period, you’d have a full balance to pay off in just 15 years.

Clearly this could increase monthly mortgage payments significantly, especially for those who took out large HELOCs.

During the boom, there were plenty of homeowners who used HELOCs as second mortgages to finance their hefty purchases. We’re talking $200,000+ loan amounts and higher in California and other pricey states.

For these folks, the payment increase will be nothing to sneeze at.

And Fitch believes individual bank disclosure on the risk of home equity payment resets is “generally inadequate.” So are banks not being upfront about their increased default risk on HELOCs?

It May Not Be That Bad

Fitch noted that only a “handful of rated banks” made disclosures about their home equity loan situation, meaning they could be holding out on the truth.

But there are a number of good things happening that should offset this anticipated payment shock.

For one, a decent amount of these loans were probably already paid off, refinanced, or extinguished when associated properties sold or were lost to foreclosure or short sale.

Secondly, many distressed homeowners have taken advantage of HAMP or HARP and other programs for those with negative equity.

As a result, their total monthly mortgage payments have been greatly reduced, even if a reset is coming on their second mortgage.

In fact, if homeowners are saving several hundred dollars a month on their first mortgages thanks to a massive interest rate reduction, it should be more than enough to offset a payment increase on the HELOC.

If anything, they can take their savings on the first mortgage and apply it to the HELOC, and probably still wind up with money left over.

Additionally, home prices are on the rise, meaning many of these homeowners are getting back above water, or even lowering loan-to-value ratios to levels where a traditional refinance is possible.

Lastly, the prime rate, which dictates what a borrower will pay on a HELOC, is as low as it can go, at just 3.25%.

Before the crisis, the prime rate was as high as 8.25%, so rates on HELOCs are rock bottom as well.

In other words, we probably don’t have too much to worry about collectively, though certain homeowners will definitely be affected.

And that could mean more payment defaults and foreclosures, and more losses for the big banks that hold all these loans.

- Can You Get a 4% Mortgage Rate Still? - August 10, 2026

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026