It’s time for a new mortgage match-up.

Since paying down the mortgage early seems to be so en vogue these days, it makes sense to compare “20-year mortgages vs. 30-year mortgages.”

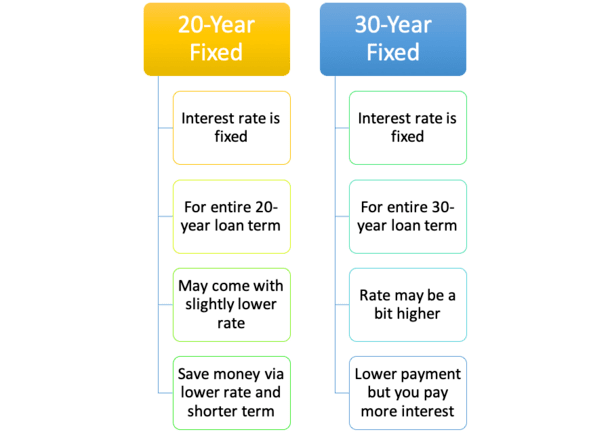

The most common type of mortgage is the 30-year fixed. It amortizes over 30-years and the mortgage rate never changes during that time.

Each mortgage payment is the same every month, so there isn’t any fear of interest rates resetting higher and pushing a homeowner toward foreclosure.

It’s also very affordable relative to other loan programs because of the ultra-long amortization period. Pretty straightforward, right?

For this reason, it holds a near-90% share of the home purchase market, and accounts for over three-quarters of all home loans, including refinances. It is the gold standard.

This simplicity and safety explains its popularity, but that doesn’t mean it’s the perfect home loan.

After all, they take a full three decades to pay off, and with first-time home buyers sometimes entering the market between the ages of 30 and 40, one could easily carry their mortgage into retirement.

Fortunately, there are other options with different loan terms to consider.

How a 20-Year Fixed Mortgage Works

- Just like the more common and popular 30-year fixed mortgage

- The interest rate never changes during the entire loan term

- But the 20-year mortgage term is a full decade shorter

- This results in less interest paid in exchange for a higher monthly payment

The 20-year fixed mortgage is a pretty simple loan program, just like it’s much more popular cousin the 30-year fixed.

They’re actually no different other than the fact that the mortgage term is 10 years less.

Both come with an interest rate that never changes during the loan term, making it a safe choice for someone fearful of a rate adjustment on an ARM.

The borrower who opts for a 20-year fixed also gets to pay off their home loan a decade earlier.

Aside from owning your home much faster, you’ll also save on interest over the shorter repayment period.

Another benefit is that the interest rate is sometimes a bit cheaper as well, which results in a one-two punch.

20-Year Mortgage Loans Can Save You a Lot of Money

- It’s not very economical to pay back your mortgage over 30 years

- Some will even argue that 20 years is too long as well

- You pay a ton of interest over such an extended period of time

- But not everyone can afford the higher monthly payment tied to shorter-term mortgages

When it comes down it, 30-year mortgages have some serious drawbacks, with the most obvious one being the long amortization period.

They also come with the highest interest rates relative to other loan programs. Yes, you pay a premium for the convenience of a fixed interest rate over three decades.

And since the mortgage takes so very long to be paid off, a lot more interest is paid and it takes forever to build home equity.

Think of it this way. If you borrowed money from a friend and asked to pay it back over 30 years, they would probably say no. Only mortgage lenders seem willing to do this.

If by chance they agreed, they’d want to charge you a higher rate of interest. And because you’d be paying it back so slowly, you’d pay a lot more interest over that time.

Assuming your loan amount is large, perhaps a jumbo mortgage, it could be the difference of many thousands of dollars versus a mortgage with a shorter term.

Consider a Shorter-Term Mortgage Like the 20-Year Fixed

- A 20-year fixed greatly reduces the amount of interest due

- And results in a home that is free and clear 10 years earlier

- The monthly payment may not even be much more expensive

- Perhaps just 1.2 to 1.3X that of a 30-year fixed depending on rate

So what are homeowners to do? Well, the most common solution to this ”problem” is to look at a shorter-term home mortgage instead, such as a 20-year loan.

While the 15-year fixed is the most common alternative, it comes with its own drawback, namely a much higher monthly mortgage payment that most home buyers can’t afford, especially first-timers.

In other words, not every homeowner can just say, “I want to pay my mortgage off faster” and switch to a 15-year fixed or 10-year fixed mortgage.

It gets very expensive. Nor can most first-time home buyers qualify at the higher payment.

Fortunately, there are mortgage product options in between, with the most common being the 20-year fixed mortgage.

A 20-year mortgage sheds 10 years off the typical loan term, and results in much less interest paid throughout its duration. The mortgage payments are also relatively manageable.

Tip: There are 20-year FHA mortgages and VA loans available if you don’t have a lot of down payment money but still want to pay your mortgage down fast.

Let’s look at an example of the 20-year fixed to illustrate the savings:

| $200,000 Loan Amount | 30-Year Fixed | 20-Year Fixed |

| Mortgage Rate | 4% | 3.75% |

| Monthly P&I Payment | $954.83 | $1,185.78 |

| Payment Difference | $230.95 | |

| Total Interest Due | $143,738.80 | $84,587.20 |

| Interest Difference | $59,151.60 |

20-Year Mortgage Rates Are Cheaper

- You should receive a lower mortgage rate if you opt for a 20-year fixed mortgage

- How much lower will vary by bank/lender and how much you shop around

- Expect a discount somewhere around .125 to .25% vs. the 30-year fixed

- But be sure to put in the time comparison shopping

As you can see from the example above, 20-year fixed mortgage rates aren’t much different than 30-year fixed mortgage rates, though the 20-year mortgage does tend to price a little bit lower than the 30-year fixed.

That lower interest rate can save you even more over the shorter term of the 20-year loan.

Overall, I’d say that 20-year mortgage rates price about a .25% below a comparable 30-year fixed. So 3.75% instead of 4%, or 3.5% instead of 3.75%. You get the idea.

It does depend on the bank or credit union in question. Some may price the loan products fairly similarly, with the only difference reduced closing costs (or fewer discount points).

They’re definitely going to be higher than rates on a 15-year fixed, but you should save some money versus the 30-year fixed.

Of course, you have to consider your property type, credit score, down payment/home equity, other various borrower attributes, and whether we’re talking about conforming mortgages or jumbo mortgages.

Anyway, in our example above the homeowner with the 30-year mortgage pays about $230 less each month, despite the higher mortgage rate. Yes, their monthly mortgage payment would be significantly lower.

But the 20-year fixed results in interest savings of nearly $60,000 over the life of the loan! This borrower would also own their home free and clear an entire decade earlier.

Doesn’t 20 years sound a lot more reasonable than 30? You can actually see the light at the end of the tunnel and pay off the mortgage before your hair turns gray.

This shorter term can be pretty beneficial, especially if you plan to retire soon and anticipate being on a fixed income.

Or if you want to build equity and buy a move-up property in the near future, using the proceeds for the down payment.

The 20-year fixed is also a good alternative because you won’t break the bank making your mortgage payment each month.

It’s a nice middle ground between 30 years and 15 years, and highlights the importance of comparing mortgages across the whole spectrum.

But again, the monthly payment will be higher than the 30-year payment, which could stretch you thin or limit what you can afford if you’re buying an expensive home.

Tip: When obtaining a mortgage pre-qualification, ask your loan officer if you make enough to support 20-year fixed payments. Or simply do the math yourself with the help of a mortgage calculator.

Go With a 20-Year Fixed Mortgage to Stay on Course

- If you have a 30-year mortgage and want to refinance to a lower rate

- Consider switching to the 20-year fixed instead of getting another 30-year term

- This way you won’t restart the (amortization) clock on your mortgage

- You can save even more interest and pay off your home loan a lot faster

If you’re currently in a 30-year fixed, and don’t want to reset the mortgage clock during a mortgage refinance, consider a move to a 20-year fixed to stay on course without even paying more each month.

For example, if you’ve already been paying down your mortgage for five years, you won’t necessarily want to take on a fresh 30-year mortgage if your goal is to pay off your loan.

Because mortgage rates are so low at the moment, you may be able to refinance from a 30-year to a 20-year fixed mortgage and still lower your monthly payment.

Also keep in mind that there are other loan types outside the 15, 20, and 30-year options.

Some banks even allow you to choose your own mortgage term, whether it’s a 17-year fixed or a 24-year fixed.

So be sure to look at all available home loan options to determine which makes the most sense financially for your unique situation.

Also ask yourself why you want to pay the mortgage off sooner rather than later. There may be a better place for your money.

Read more: 30-year fixed vs. 15-year fixed.