Mortgage Q&A: “Are mortgage rates higher for condos?”

If you’re in the market for a new condo or a townhouse (as opposed to a house), you’re probably looking to save some money on your mortgage payment each month.

After all, condos tend to be a lot cheaper than single-family homes in similar areas because you get limited space and forgo things like a nice green yard to play in.

But you may be in for a surprise when you start shopping mortgage rates.

Condos May Have Hidden Financing Costs

- While condos are typically priced lower than single-family homes

- There are other costs to consider like HOA dues and more expensive home loan financing

- If you’re unable to put down 25% on a condo purchase you will likely get hit with a pricing adjustment

- This will either increase your mortgage rate slightly or bump up your closing costs

Sure, a condo might come with a lower price tag, but that’s not the end of the story.

They typically come with higher mortgage rates and costly HOA dues, both of which should be factored into your side-by-side analysis.

In some areas, HOA fees can be nearly as expensive as mortgage payments, totaling $500 or more each month. So definitely factor them in when determining affordability.

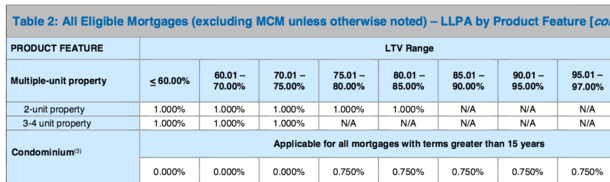

Additionally, many mortgage lenders charge a 0.75% mortgage rate pricing adjustment for a condo once the loan-to-value ratio (LTV) exceeds 75 percent.

And let’s face it, most home buyers put very little down these days.

For example, Fannie Mae (and Freddie Mac) charges a loan-level price adjustment (LLPA) for condos, as seen in the screenshot above.

This will likely be passed on to you, the consumer, in the form of a higher rate or higher closing costs.

How to Avoid the Condo Pricing Adjustment

There are two ways to avoid the mortgage pricing hit associated with condos.

Either by going with a 15-year (or shorter) loan term, or by keeping the LTV at 75% or lower, the latter sometimes accomplished via a combo loan.

Simply put, if you want a 30-year loan and can’t put down 25 percent or more on your condo, expect a slightly higher mortgage rate or a higher-cost loan.

This tends to be the case for conforming mortgages, jumbo loans and conventional mortgage loans.

Note that the pricing adjustment doesn’t mean your mortgage rate will/should be .75% higher.

It just means the bank or mortgage broker will make less on the loan, and thus will charge a higher rate or cost accordingly.

So expect a mortgage rate maybe .125% or .25% higher if it’s a condo, and perhaps even more if it’s a high-rise condo.

Why Are Mortgage Rates Higher on Condos?

- Condominiums are a form of shared ownership

- One bad apple can affect the entire building

- As such they are riskier than single-family homes

- More restrictions mean less competition, which could equate to higher rates

Well, condos are part of a larger complex, unlike a single-family home.

And each unit affects the whole project, so if several owners are unable to make payments (or if they’re vacant because of things like foreclosure or failure to sell), the other units will lose value.

Additionally, the HOA won’t get all the dues it expects, which puts the entire building at risk when it comes to things like maintenance and upkeep. This can create a serious domino effect.

Another thing to consider is the share of investment properties within the complex – more investors generally means more risk.

This explains why Fannie and Freddie charge a premium for a home loan attached to a condo.

Finally, not all mortgage lenders offers condo financing, so less competition could mean higher rates.

FHA Loans on Condos

- It can be difficult to get an FHA loan on a condo

- Only FHA-approved condos are eligible for financing

- And many condo complexes nationwide do not qualify

- There are strict rules and requirements like investor/FHA concentration, an environmental review, and more

As far as FHA loans go, there generally isn’t a pricing adjustment for condos, but you may find that fewer condominium complexes are actually approved for FHA financing.

This means it might not be an option at all, which could create an even bigger problem if you don’t qualify for a conventional loan.

You can find out if your condo complex is approved for FHA loans here.

The FHA recently enacted a tough set of standards for condos, including strict zoning rules and policies where a certain number of units must be owner-occupied, sold before endorsement, and current on HOA payments.

So you may see things like, “FHA-approved condos for sale,” because it’s a great marketing angle for the ones that do allow it.

And many prospective condo buyers probably want to put as little down as possible, which is where the FHA loan and its 3.5% down payment comes in.

Just keep in mind that when it comes time to sell your precious condo, it’ll be more difficult to find a buyer as well if financing is limited.

In short, you’re reducing the pool of eligible buyers, which you never want to do when selling anything.

This doesn’t mean you need to go out and buy a house, because that may open another can of worms, but it’s something to think about when seeking financing.

- Mortgage Rates Narrowly Avoid New 52-Week Highs as Bond Yields Surge Higher - July 31, 2026

- Trump Says Warsh Wants Lower Interest Rates, But Has a Political Board - July 30, 2026

- Do Mortgage Rates Need a Hike to Move Lower? - July 28, 2026