What Is a Jumbo Mortgage Loan?

A “jumbo loan” is a mortgage with a loan amount that exceeds the conforming loan limit. It is set by the Federal Housing Finance Agency (FHFA), which oversees Fannie Mae and Freddie Mac.

This limit can change annually and is currently $832,750 for a one-unit property in the contiguous United States for 2026, up from $806,500 last year

If your loan amount is $832,751 or higher, your home loan is considered jumbo unless it’s a multi-unit property and/or located in a high-cost area.

Among other things, this means it’s not eligible for purchase by Fannie Mae or Freddie Mac.

As such, it could be more difficult to obtain/qualify, and the interest rate might be higher too.

Jump to jumbo loan topics:

– Jumbo Loan Limits

– Jumbo Loans vs. Conforming Loans

– Getting a Jumbo Loan Can Be More Difficult

– Jumbo Loans Tend to Be More Expensive

– Jumbo Mortgage Rates

– Minimum Down Payments on Jumbo Loans

– High Balance Loans

– Super Jumbo Loans

– Jumbo Mortgage FAQ

Determining the Size of a Jumbo Mortgage

Each November, the FHFA announces the conforming loan limit for the following year, based on annual home price changes from October to October.

If the housing market does well and home prices rise, the conforming limit will go up and so will the minimum loan amount for a jumbo.

If home prices happen to fall, which is rare, the loan limits will simply remain flat.

Higher loan limits are generally viewed as a good thing because borrowers tend to try to avoid the jumbo realm. They do so to receive better loan pricing, or to qualify for a loan more easily.

Jumbo mortgage rates are typically higher than interest rates on conforming mortgages because they can’t be purchased by Fannie Mae and Freddie Mac. Fewer investors (buyers) means less liquidity and higher interest rates.

Additionally, it can be more difficult to obtain a jumbo loan, either because of a higher credit score requirement or larger minimum down payment.

So if you’re a prospective home buyer or planning to refinance an existing mortgage, be sure to keep this key threshold in mind while shopping rates.

Jumbo Loan Limits Vary By Property Type and Region

The baseline conforming loan limit is the main determining factor for whether a loan is jumbo or not.

But in certain “high-cost regions” of the country there are expanded conforming loan limits. These loan limits are also higher for multi-unit properties like duplexes and triplexes.

In other words, there are different jumbo loan limits depending on both the number of units, along with where the property is located.

For properties located in the contiguous United States, including D.C and Puerto Rico, jumbo loan limits are as follows:

1-unit property: Greater than $832,750

2-unit property: Greater than $1,066,250

3-unit property: Greater than $1,288,800

4-unit property: Greater than $1,601,750

*In Alaska, Guam, Hawaii, and the U.S. Virgin Islands, and high-cost regions, jumbo loan limits are even higher.

1-unit property: Greater than $1,249,125

2-unit property: Greater than $1,599,375

3-unit property: Greater than $1,933,200

4-unit property: Greater than $2,402,625

And Hawaii has high-cost area loan limits on top of these. For example, you can get a home mortgage as large as $2,499,100 for a four-unit property in Honolulu or $2,402,625 in Los Angeles before it is considered jumbo.

As you can see, you can get a very large loan without entering jumbo loan territory in high-priced areas of the country. The same goes for multi-unit properties in all 50 states.

Loan amounts between the baseline conforming loan limit and the jumbo cutoff are known as “high-balance mortgage loans.” They are subject to additional pricing adjustments, which I’ll discuss below.

Jumbo Loans vs. Conforming Loans

- Jumbo mortgage rates tend to be higher than conforming rates in most cases

- And fewer banks and lenders offer jumbo loan financing

- Underwriting guidelines are also more conservative for jumbos

- You typically need a higher minimum credit score and larger down payment

So what’s the difference between jumbo loans and conforming loans, you ask? And does it matter?

Well, for starters, the loan amount must be at or below the conforming loan limit to be considered conforming, as discussed above.

In addition, the mortgage must meet the strict underwriting guidelines (credit, income, assets requirements) of Fannie Mae or Freddie Mac.

Known as government sponsored enterprises (GSEs), the pair buy and securitize mortgages on the secondary market. They do so to provide liquidity to lenders so they can fund more loans.

The main takeaway is conforming loans are smaller in size than jumbo loans, as the name implies. That’s pretty much the main point to remember.

While there are several ways a mortgage can earn the distinction of non-conforming, only a large loan amount will make it a jumbo.

Getting a Jumbo Loan Can Be More Difficult

- Not all banks offer jumbo loans so they maybe harder to find

- Jumbo underwriting guidelines can vary considerably by lender

- Higher down payment/credit score requirements may make it harder to qualify

- May need 10%+ down payment vs. just 3% for a conforming loan

- May need a 660/680 minimum credit score vs. 620 for conforming

Qualifying for a jumbo loan can be much more difficult than qualifying for a conforming loan, as fewer banks and mortgage lenders offer them.

This all has to do with risk – because conforming loans are guaranteed by Fannie and Freddie (who are government-backed), there’s more demand for them on the secondary mortgage market.

After all, the loans are essentially guaranteed by the government. As a result, interest rates will be lower because more buyers means banks can fetch a higher price for their mortgages.

Conversely, with fewer banks vying for your jumbo loan, you will likely be greeted with both a higher interest rate and more financing restrictions.

Are Jumbo Mortgages More Expensive?

- Jumbo loans aren’t backed by Fannie Mae or Freddie Mac

- This means they aren’t as easy to package and sell to investors

- As such jumbo mortgage rates are generally higher

- But this spread can change over time and may not always be significant

Typically, jumbo loans are more expensive than conforming loans.

Historically, this spread has ranged from a quarter to a half percentage point, but it widened to as much as two percentage points during the height of the financial crisis.

At that time, nobody wanted to touch anything without an implied or explicit government guarantee.

Currently, the spread between conforming and jumbo loans is very small, perhaps less than half a percentage point. But it’s not just higher mortgage rates you have to worry about with a jumbo loan.

Because jumbo loans don’t adhere to Fannie and Freddie’s underwriting standards, they don’t come with that sought-after government guarantee.

Instead, individual banks and lenders set their own jumbo loan guidelines, which are typically more stringent.

For example, you’ll likely need to come up with a larger down payment (we’re talking 20% and higher in many cases) while maintaining an excellent credit score.

Fannie and Freddie accept credit scores as low as 620. Expect a higher minimum credit score for a jumbo, perhaps 660 or 680. Plenty of assets in the bank are usually a requirement as well.

These drawbacks explain why most home buyers attempt to avoid jumbo loan territory, either by putting down more cash at closing or going with a combo loan, thereby keeping the first mortgage at or below the conforming limit.

In any case, be sure to shop around with a variety of lenders to ensure you explore all your options, whether your loan is conforming, jumbo, or somewhere in between.

Jumbo Mortgage Rates Are Often Higher

Because of additional risk and less liquidity, jumbo loans tend to carry slightly higher mortgage rates, although not necessarily by that much.

As mentioned, the difference may only be .25% – .50% higher, or borrowers may just lose out on any lender credit offered for a conforming loan amount (this translates to higher closing costs).

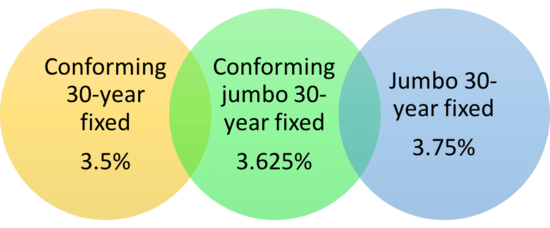

As seen in the illustration, if a conforming 30-year fixed loan (non-jumbo) is going for 3.5%, you might expect to pay 3.75% for a comparable jumbo mortgage.

Mortgage rates are a lot higher in 2025 so adjust accordingly, but the same rule applies. You’ll generally pay a premium for a jumbo loan.

While that might not seem like a lot, it can boost the monthly payment quite a bit due to the large loan amount.

At the same time, you might find a particular lender whose jumbo rates are much more competitive than their conforming rates, and vice versa.

For example, Ally Mortgage is really aggressive when it comes to jumbo mortgage rates, whereas their conforming offerings are nothing out of the ordinary.

So take the time to compare mortgage offerings from bank to bank. It can pay off big time.

Minimum Down Payments on Jumbo Loans

Most mortgage lenders offer the same loan programs for jumbo loans as they do for conforming loans, such as fixed-rate mortgages, adjustable-rate mortgages, and interest-only home loans.

However, it is much more difficult for borrowers to find low-down payment or zero-down jumbo mortgages.

For reference, many lenders back in the early 2000s could provide 100% financing on deals up to around $1.5 million! Then the housing market crashed…

Today, you might be expected to come to the table with a 20% down payment if you want a jumbo.

Keep in mind that most jumbo lenders have maximum loan amounts as well. These usually drop as the loan-to-value (LTV) increases.

For example, you may be limited to $2 million at 80% LTV, but able to borrow $3 million at 70% LTV.

If your LTV is below 65%, a loan as large as $5 million may be possible. Of course, these are just some examples, guidelines will vary by lender.

These max loan amounts and LTVs will be even lower if the property isn’t your primary residence.

You may also be required to document a larger amount of cash reserves (in your savings account) to prove you can pay the loan back.

The takeaway is jumbo loan underwriting can be a lot more restrictive relative to other types of mortgages.

High Balance Loans – Between Jumbo and Conforming

- Loan amounts above the baseline conforming limit

- But within the high-cost loan limits are known as conforming-jumbo loans

- Known as high-balance loans (Fannie Mae) or super conforming mortgages (Freddie Mac)

- Mortgage rates can be lower than jumbos and underwriting a bit more flexible

After the mortgage crisis in the early 2000s, the Housing and Economic Recovery Act of 2008 (HERA) brought about so-called “conforming-jumbo loans.”

These are neither jumbo loans or conforming loans, and range between $832,750 and $1,249,125 for a one-unit property.

Fannie Mae refers to them as “high-balance mortgage loans” (HBLs), while Freddie Mac calls them “super conforming mortgages.”

In the Los Angeles County, you can get a loan up to $1,249,125 on a one-unit property without it being considered jumbo.

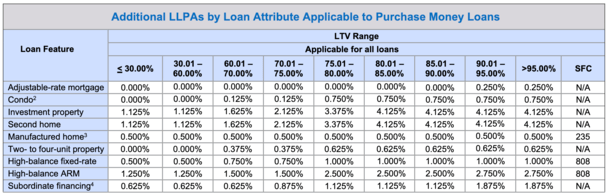

However, additional pricing adjustments apply, as seen in the chart below.

This would make the mortgage rate higher than a standard conforming loan. But likely cheaper than a jumbo.

Counties with lower home values, such as Maricopa (Phoenix) don’t have a high-cost loan limit because home prices there don’t warrant it. The same is true in Chicago and Miami.

This matters because conforming jumbos may be easier to qualify for and just slightly more expensive to finance than a conforming loan.

Super Jumbo Loans – The Really Big Ones

- This is a subjective term that may vary depending on who you ask

- A super jumbo in the early 2000s was a loan amount above $650,000

- Now it might be a loan amount that exceeds the high-cost loan limit

- Though it probably varies by region and company

Some jumbo loans are known as “super jumbo loans,” much to the excitement of mortgage brokers and loan officers who think they’ve got a huge deal on their hands (and dollar signs in their eyes).

While there might be some argument, a true “super jumbo loan” is probably any loan amount above the high-cost limit for the county, ranging up to $20 million or higher.

This term is certainly relative, depending on the state in which the overzealous loan officer resides. I suppose it can vary based on where you live and what you’re used to seeing.

When I worked in the business, a super jumbo was any loan amount over $650,000…today it might be a loan amount of $2 million and up thanks to our friend inflation.

CoreLogic recently defined super jumbo as a loan amount between $10 and $20 million, and identified over 230 active loans that fit that description.

They noted that a whopping 75% of them were originated since 2013, a testament to recent sky-high property values.

Tip: You can break up your loan into a first and second mortgage to avoid paying more for a jumbo loan, keeping the first below the conforming loan limit. Just make sure the combined rate is cheaper than what it would be otherwise.

Jumbo Mortgage FAQ

How much is a jumbo mortgage in 2026?

Any loan amount above $832,750 for a one-unit property in the contiguous United States, including D.C. and Puerto Rico. There are higher limits for multi-unit properties and for properties in Alaska, Guam, Hawaii, and the U.S. Virgin Islands. See top of page for all the numbers.

How much is a jumbo loan in California? Or any other state.

In my home state, and more specifically, city of Los Angeles, it starts above $1,249,125. However, it varies by county, so some areas of California start at just above $832,750. Check this list to see where your county stands. It’s not a state-based calculation, so make sure you check the county!

What types of jumbo mortgages are available?

Like other types of home loans, you can get anything from adjustable-rate mortgages to 20-year fixed mortgages and everything in between. You might even be able to get your hands on something conforming mortgage lenders don’t offer. So you shouldn’t be limited in this department.

How hard is it to get a jumbo loan?

As noted, it was very difficult post-mortgage crisis to even find a lender willing to offer them. But it has gotten much easier. Today there are plenty of options from all types of different lenders. In fact, some lenders will now offer a jumbo with just five percent down!

However, I would still say qualifying is a bit more difficult than it is for conforming loans, especially if we’re talking about an investment property. Often you’ll need a larger down payment and a strong balance sheet (healthy amount of assets and solid income) to get approved. Don’t be deterred though!

Can I get a jumbo loan with bad credit?

Maybe, but typically minimum credit scoring requirements are a lot higher, and your options will be more plentiful if your FICO scores are 700+. If you are able to obtain financing with a lower score, you’ll likely pay the price in the way of a higher mortgage rate. And you probably won’t want your mortgage payment to be any higher than it already is.

Do jumbo loans require mortgage insurance?

It depends. If the LTV is above 80% and the lender requires it then yes. Often it isn’t required because the minimum down payment will be at least 20%. If the LTV is above 80% and it’s not explicitly charged, you could argue that it’s built into the (higher) mortgage rate anyway.

What is the minimum down payment on a jumbo loan? Can I get one without 20% down?

Some aggressive lenders are now only asking for 5% down, though you’re more likely to see a down payment requirement of at least 10%, if not 20%. But if you shop around you can find a lot of flexible jumbo loan options these days.

- Did Everyone Forget Mortgage Rates Were 2-3% Back in 2012 Too? - June 8, 2026

- Mortgage Rates Now Face a Triple Threat - June 5, 2026

- Can You Have Two Mortgages at the Same Time? - June 4, 2026

I’ve noticed lately that mortgage rates are lower on jumbo loans vs. non-jumbos? Is this because the Fed is going to stop buying mortgages backed by Fannie Mae and Freddie Mac?

Pretty much – as investor demand for conforming mortgages decreases (thanks in part to Fed exit), interest rates will need to rise to lure in more buyers. Conversely, as more investors seek jumbo loans, rates should drop.

I recently applied for a jumbo loan and was told it would be cheaper if it were conforming. So I guess it depends on the lender. I might be able to bring in some cash to keep it under the jumbo limit though. Gotta do the math to see if that makes sense.

Yeah, last I checked, Wells Fargo was offering lower rates on jumbo loans than conforming loans, but it might be short-lived, assuming things normalize again soon.

I’ve seen the opposite. It depends which bank you’re dealing with and what they specialize in. Most of the time jumbo loans will be priced higher than conforming loans. That’s the norm, so anything opposite of that is the exception, not the rule.

Yep. More often than not your jumbo loan is going to price higher than a conforming loan. There’s less liquidity for jumbos on the secondary market, so they often carry a premium.