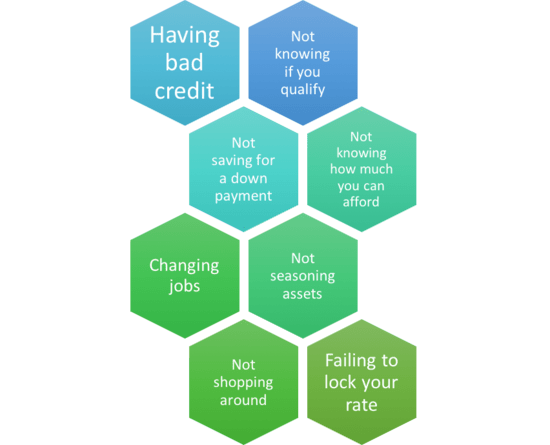

Common Mortgage Mistakes Borrowers Make

- Not getting pre-approved for a mortgage

- Not shopping around for a lower interest rate

- Failing to check credit scores in advance

- Opening new credit cards or other loans before/during the mortgage process

- Making late mortgage payments or worse, filing foreclosure/BK

- Not saving enough for a down payment and closing costs

- Not seasoning assets beforehand in a verifiable bank account

- Applying with limited or inconsistent employment history

- Changing jobs prior to or during loan process

- Forgetting to lock your mortgage rate

- Lying to the bank or lender!

I’ve put together a list of what I feel are the top 10 “mortgage mistakes” individuals should avoid if they’re planning to apply for a home loan.

These apply whether you’re financing a new home purchase or refinancing an existing mortgage.

Avoiding these missteps will ensure your home loan process is a smooth one. Or at least not a complete train wreck.

Some are obvious. Some less so. But it never hurts to brush up on the basics before an important life event.

Otherwise you could end up with a higher-than-necessary mortgage rate, or worse, see your loan application get declined!

1. Filing Bankruptcy or Being Foreclosed Upon

While this may be a no-brainer, it still reigns supreme. Avoid bankruptcy and foreclosure, plain and simple. Either could keep you out of the mortgage game for several years (up to seven years in fact!) for obvious reasons.

Also steer clear of late mortgage payments. I’m talking about 30+ day delinquencies, not just being a day or two late.

Even if your credit scores are high enough to meet minimum underwriting guidelines, late mortgage payments that show up on your credit report can disqualify you with many banks and lenders. Especially recent ones. Makes sense doesn’t it?

2. Not Locking Your Mortgage Rate

If you fail to (or forget to) lock the interest rate on your mortgage, your rate could go up. A lot.

Remember, mortgage rates change daily, just like stock tickers because they’re based on the same market dynamics.

The price today might be totally different tomorrow. And until you lock it in, it’s subject to change.

Yes, you have the choice to lock or float when you apply for a mortgage, but make sure you understand both options and keep an eye on interest rates before and during the home loan process.

Fortunately, it’s fairly easy to track mortgage rates, though predictions are a little harder.

3. Lying to the Lender

This is a given, but it doesn’t stop people from trying. Don’t lie to your lender. Don’t lie to the loan officer, the loan processor, or the loan underwriter.

They are good at what they do and will likely catch you if you attempt any funny business. This means being upfront and honest from the start to ensure you don’t create major problems later on.

For example, don’t say the property is your primary residence if you intend to rent it out. Sure, it may be easier to qualify this way. And the mortgage rate might be lower. But if you get caught, it’ll be game over.

And don’t falsify your income, assets, or employment history. Fake pay stubs and other nonsense are a surefire way to get your application denied. Or worse, in serious hot water.

It’s also just better for all parties involved. Otherwise you could waste their time and yours.

[See common refinance mistakes if you already own a home.]

4. Not Factoring In All the Costs

Before you apply for a mortgage, consider all the costs involved. Even outside the loan itself you’ll be faced with moving/relocation costs, renovations, new furnishings, and more.

Meanwhile, the mortgage is just one piece of the pie. There’s a handy acronym for housing payments known as PITI.

It stands for principal, interest, taxes, and insurance. Yes, there is more to a mortgage than just principal and interest.

And those other costs can be quite expensive. In fact, homeowners insurance costs have skyrocketed in some markets. The same goes for property taxes.

Once you own the home, things could get even worse. Have you earmarked cash for maintenance or the unexpected repair?

Being a homeowner is a lot harder (and more expensive) than it looks. It’s no wonder homeowners often dream of being renters again.

Jokes aside, make sure you’re financially prepared long before you apply.

5. Not Getting Pre-Approved for a Mortgage Early On

Not figuring out how much you can afford well before beginning your property search. You should get pre-qualified or pre-approved before you even start looking at homes.

Once you know how much home you can afford based on your salary and assets (and liabilities), you can properly assess the situation.

Otherwise you could just be wasting your time and setting yourself up for disappointment.

In fact, I’ve argued that it might be best to look for a mortgage before looking for a home.

After all, if you don’t even qualify, what’s the point? You’ll waste your time and your real estate agent’s too.

Knowing your purchasing power upfront can also help you fine-tune your property search and set appropriate filters on apps like Redfin and Zillow.

You won’t want to get your hopes up on your dream home, only to realize it’s out of your budget.

6. Opening New Credit Cards or Spending Big

Opening new credit cards or making excessive charges on existing credit lines before and during the loan application process (it happened to me!).

This can hurt your credit scores tremendously and increase your debt load, which could lead to disqualification. See my debt-to-income ratio post for more on that.

It’s a one-two punch because your scores go down, which can lead to a much higher mortgage rate. And you have less borrowing capacity due to increased monthly liabilities.

This can eat away at your purchasing power and make qualifying more difficult if not impossible.

When it comes down to it, you can buy your new fancy couch and big-screen TV once the loan is funded and recorded.

7. Applying for a Mortgage with Limited Employment History

Attempting to get a mortgage with less than two years consecutive employment in the same occupation or field (unless you’re a recent grad with proof of future income like a doctor) isn’t the best idea.

You must prove to mortgage lenders that you will actually continue to make the money you’re currently making to obtain a home loan.

To this same end, avoid switching jobs prior to application unless it’s in the same field. If you were a chef and all of a sudden you’re an accountant, the lender may not be so sure your income will continue.

Show them you’ve got a solid track record of making money in a similar position and you should be golden.

If nothing else, avoid job hopping just to make the loan process smoother for all parties involved.

8. Not Having Seasoned Assets and Rental History

Don’t attempt to get a mortgage without a documented 12-month housing history.

This means cancelled checks or a Verification of Rent (VOR) from your landlord that proves you made timely rental payments in the past.

Yes, lenders want to know that you paid your rent on time previously (unless you live with your parents).

The same goes for verifying your assets. Be sure you set aside assets that cover at least two months of your proposed mortgage payment, including taxes and insurance.

Oh, and the money needs to be in your bank account, not under your mattress. Or in your cousin’s account. And it should be there for several months before you apply to ensure it’s seasoned.

Don’t forget the down payment and closing cost funds while you’re at it.

9. Applying Without Solid Credit History

You may not get approved for a mortgage if you fail to establish your credit history beforehand.

You generally need at least three credit tradelines (that actually show up on your credit report) with a minimum two-year history on each to qualify for a mortgage.

Yes, credit is apparently the root of all evil, but also a necessary one in the mortgage world, that is, unless you plan to pay for your house with cash…

Ultimately, you want to aim for a FICO score of 780+ to obtain the best terms on your loan.

It might be possible to get by with less, but your financing options could be limited. And the interest rate/fees may not be as competitive.

Regularly review your credit report to ensure there are no surprises long before (several months) you begin the mortgage process.

10. Failing to Shop Around for Your Mortgage

If you don’t take the time to comparison shop, as you would any other product you buy, like a plane ticket, TV, or a car, you’re doing yourself a major disservice.

It’s even more of a fail when it comes to getting a home loan since the payment could stay with you for 360 months!

You don’t pay once. You pay monthly. So do your research and get it right the first time.

Studies prove that those who obtain multiple quotes save money versus those who don’t. And guess what? Most consumers only get a single quote. And they typically use the first lender they speak to.

Don’t be lazy. Speak to a few different companies. Educate yourself along the way. Put in the hours necessary to ensure you find the right bank/lender/broker to work with.

In the process you should be able to snag a good deal, aka a low interest rate with limited closing costs.

Bonus tip: Compare different loan products, such as fixed-rate mortgages vs. ARMs and conventional loans vs. FHA loans.

One may be better suited for you and even save you some money. There is no one-size-fits-all solution.

I wish I had known these before I applied for a mortgage. Problem is once you apply, it’s too late if you don’t adhere to the rules mentioned above. It’s a shame the banks don’t make these rules more clear to the general public.

#4 is not specifically correct. Medical collections are not usually considered in the underwriting process. In addition adding a dispute to a credit report will prevent any loan from closing, the dispute will have be removed. When the dispute is removed it will be counted as an active debt and credit scores will go down.

Mike,

I should specify that disputing these items long before you apply for a mortgage will help. Perhaps a few months. That way you can get them removed and restore any related credit score damage before beginning the mortgage process.

Thanks for your input.

In the article it says medical debts crush your fico. I spoke to a lender about my situation and he said medical doesn’t really have any bearing on how they figure score. Told me not to worry about my medical judgment. Can anyone elaborate on that?

The new FICO score (FICO® Score 9) greatly reduces the impact of medical collections because the brains at FICO realized they aren’t representative of increased credit risk, and therefore their impact on credit scores should be low. But that assumes the lender is using FICO 9 and not an earlier model. Either way, it makes sense to remove/dispute medical collections before applying for a mortgage to ensure your score is as high as possible.

What type of rent documentation is required for mortgage loan approval? While looking through 12 months of electronic documentation, I saw that there were a few months that were paid a few days late, but less than 30. Will we not qualify for a mortgage as a result? I do not have cancelled check to provide, just electronic records that show the late fees. My credit score is good otherwise. Thanks.

Generally, a verification of rent form will ask for 30-day late payments, not payments made a few days late.

I have 4000 in medical collections is there any way that I can get home loan. I make good money but having hard time

Hey Kyle,

It depends on your credit score, assets, income, etc., but the collection itself may not be an issue depending on loan type and your other borrower attributes. Might be a low credit score that’s the problem?

Wonderful how the 2-year credit requirement discriminates against new US residents…

Dan,

There are lenders that specialize in foreign nationals and non-resident aliens.

Thanks for all the great advice.

I have purchased many homes and hung out with my parents during their real estate business wheeling and dealing days and still browse the net for updated advice / reinforcement on what I already know. I learn something new or see a new perspective all the time.

These are such good points, but for most first time buyers they mere abstractions. They just want that first house so very badly. It takes a couple of times through the buy-pay-sell cycle to appreciate.

Thanks again!

can i get approved if i have no rental history?

Lex,

If you don’t have rental history you’ll likely just need to explain what you’ve been doing (for housing) and prove that you can handle mortgage payments going forward.

Can you please give me advice? I have to give you some background so I apologize for the length. I have always relied on my husband but a couple yrs ago he suffered a severe blood clot and developed a pain disorder. He has not been able to work since. Our landlord, who is very compassionate, allowed me to work for rent often reducing or eliminating rent. Some months we would pay in full but it would be middle end of the month. At the time I was making between $150-$200 a week supporting a family of 4 and making excessive trips for doctors tests therapists etc. Often 1 hr travel 1 way. My credit took a bit of a hit too. Anyway, I’ve been working hard to get things stable. I now work a job where I bring home $360 a week plus a 2nd job that’s an on call gig but made 5k in 2015. My credit is improving, no lates in 12 months on credit cards. Middle Fico is a 620. We want to buy a house for $50k 5% down. If we can get it, it will save us $100 a month over renting…I just don’t know how this rent thing will affect us…Will the low price of the house make a difference? Lender calculations are telling me U can afford $120k but I’m only trying to get $50 any advice… I’m so sad because I though I was doing so well.

Kat,

Instead of speculating you’ll probably want to get pre-approved to see exactly what you qualify for based on all the numbers. And if you’re concerned the rent thing could hurt you, it may make sense to explain it upfront with a broker or loan officer that knows how to navigate the situation. Good luck!

Question: if you have old unpaid debts (from 9yr ago) and it not on credit report (and not sure who to pay the debt to) when applying for a home loan will lenders see that past unpaid debt?

Keep,

I suppose it depends who can see those unpaid debts and where they actually show up. Chances are a lender may not see them if they’ve already fallen off your credit report.

A few questions…1) what documents are required for rent history…a letter from the rental company? 2) i have been self employed for two years with a small income but recently started employment with a good salary…it’s only been a couple months…is there any chance I could still qualify with just a handful of paychecks…if I could show and employment contract would that help? Any tips? And 3) how do you even start…is there a certain bank/lender that specializes in FHA loans or first time home buyers? I’m a little lost on where to even begin. Thanks!

Cortney,

Either VOR (verification of rent form) or cancelled checks for some period, typically 12 months. It might be tough to use income that is brand new unless it’s something you can prove will definitely continue for the foreseeable future. A broker might be helpful for you because they can advise you and send your loan application to a specific lender whereas a single bank will just kind of tell you if you’re approved or not with them.

I might be short for closing. Can I make a large deposit (30k) from my SCorp (100% owned) to my personal during underwriter processed? Thank you !

Richard,

Best to ask your loan officer or broker to be sure.

Richard,

Best to ask your lender directly to know 100%.

Me and my wife Prequalified for a 150k mortgage for a house house and later decided to purchase a cheaper house (the one we have been renting for three years) we just acquired a purchase agreement contract and have an appointment with the bank in a few days. The thing that has me nervous is my wife (co-borrower) has a few medical bills in collection but her credit score is in the high 600’s..I myself (borrower) don’t have any delinquent debts and have good credit..I am nervous about being denied because of those.. but i keep reading mixed responses about medical debt. most say eliminate them for a higher credit score (no brainer) but if your credit isn’t that bad anyways are they grounds for a denial?

Glen,

As you said, removing them would likely make her credit score jump considerably, but if you can get approved regardless it might not matter. However, a lower credit score could result in a higher mortgage rate, so you could see about removing them (might be to late now) or possibly see if you can qualify without her if her credit hurts your overall application.

Hi Colin.

I bought a house 10 years ago. rigth now my mortgage is 20 years. I know the first 10 years you pay interes only. I want to refi. my house but I can’t proof my income because, I’m self employee. my self is in the mortgage and my husband is in the title. inconme for 2015, he report : 40,000 and I report 72,000 inconme from the house. We report the 40,000 from him, because we want to refi. next years and we plan to take me from the mortgage and put my husband in the mortgage and title. Can we do that and how is work.

Thank you for your help.

monica.

Great post.

I am about to close a house, and the bank is requiring proof of rent payment. I have money overseas outside the united states (That I have proof of), and brought in some cash with a relative from my overseas bank account. I used that money to pay few months of rent in cash to my current landlord.

I have cash receipts from the LL as well as a copy of the lease.

Is this an automatic denial on my loan? I am very nervous as my closing date is supposed to be in 2 weeks.

Kindly advise

Ray,

The lender may want a letter of explanation to determine why you used a relative’s money to pay your rent and ensure you have the necessary funds to make your own rental payments and subsequent mortgage payments. If it can be reasonably explained it may not be grounds for denial.

Is there anyway around the two year employment thing? High down payment? Co-signer? Etc?

Britney,

It’s possible depending on the loan and situation…the two-year thing is a general rule to avoid further scrutinization. Certainly no reason to give up until explicitly denied on this basis.

Very helpful. I have VOR question. When my wife and I got married I moved in with her to her apartment. I wire her money and she pays the rent. I just applied for a mortgage without her and the bank wants to verify my rent payments. Turns out my wife has paid the rent late quite a few times even though i sent her the money on the first of each month. Can this somehow be attributed to me and be a grounds for denial? I can prove that I wired her the rent amount on time each month.

James,

It might not be an issue if the payments are only a few days late and not reported as delinquent (generally 30+ days late), but if they are your explanation may hold water if you can document it all. Good luck.

Thank you for the quick reply!

This is a GREAT ARTICLE about a horribly f****d up industry. Buyers looking for jumbo loans need to be especially aware of #9. “You generally need at least 3 credit tradelines…” This is one of the very rare articles that even mentions this.

I prepared for a house purchase for well over a year as we patiently waited to find our dream home, relying on a mortgage broker who pulled my credit and examined my returns and issued pre-approval and assured me all requirements were met. Today I discovered that even with high Fico, high income, and perfect payment history I may not qualify because I dared to buy my cars in cash and only have two credit cards.

Not once did the idiot mortgage broker mention this in all the time he worked with me. I’m so angry right now I’d like to beat the crap out of him, and I can’t believe this messed up industry can function this way. There should be a standard set of guidelines readily available for consumers. And I did do my best to educated myself, but never once did I see this mentioned in all the articles I read. Just the opposite, all every freaking article tells you is to not get new credit.

Argh!

Robert,

Sorry you didn’t come across this tip earlier…yes, if you eschew credit it’s difficult to get other credit, such as a mortgage.

Hi Colin,

I am kind of in a sticky situation here. We arranged for a loan from PNC bank, with an agent who is very lazy as hell. We had no idea he would be this lazy and careless. He promised us we will have the mortgage ready before closing within 30 days. He never entered correct information in our documents, which is why we still haven’t signed the mortgage agreement documents yet.He promised it will be corrected soon, but it’s been a week and he has still not corrected anything and it’s only 2 weeks to closing now, is it too late to switch mortgages or is i a better idea to switch to a different branch of PNC, without losing appraisal money and other details. Please advice.

Max,

Might be tough to switch and close with so little time left…unfortunately you don’t know if the next bank/lender will be just as bad. Sadly, this is kind of how the mortgage industry works – lots of delays amid critical timelines with inconsistent service.

My husband son and I live in my Grandmothers home. I have always lived here and in the last 3 yrs have not worked due to her failing health. My husband has been on workers comp for 3 yrs as well due to having 3 surgeries from the injury and is in the process of being approved for re training. My Grandmother got a reverse mortgage about 6 yrs ago and we would like to buy the house for that balance. I would start working again either for myself or someone once I am no longer her caregiver and we could afford the mortgage payment, taxes and all but how difficult will it be to get approved with decent credit and no debts.

This is a great post. Thanks

Is it even possible for a retired person with low S.S. payments ($589 per month) to get a loan on a $27,000 (trailer) home? I’ve had a small account at the local bank for 5 years. I have no co-signer or collateral except my 2005 Dodge Neon, which is in good shape.

Might an excellent rent-payment record to the same landlord for 7 years (I’ve lived at the current location for 5) be considered? (Of course I don’t want my landlord to know I’d like to move unless something is definite.)

My credit is between Fair and Acceptable. The only thing I bought on credit was my first car, in 1969. And, can the loan be slightly higher than purchase amount?

I have roughly $10,000 on hand in cash, PayPal, and recent uncashed checks. Thank you!