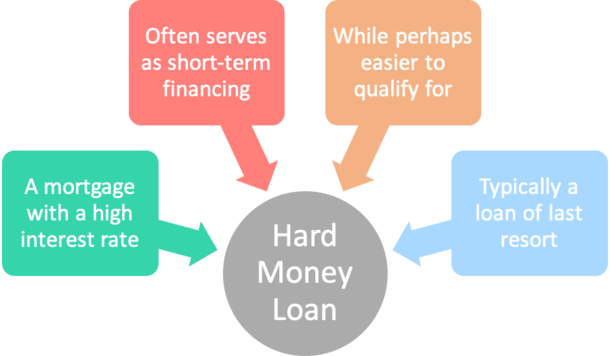

A hard money loan is a mortgage with a higher-than-market interest rate that usually serves as a source of short-term financing for borrowers who can’t qualify for a home loan with a traditional bank or mortgage lender.

The phrase could have something to do with the fact that these lenders provide hard-to-find solutions you probably won’t find elsewhere. Or possibly because the borrower has fallen on hard times.

Either way, many associate these types of loans with a bridge loan because it’s often a quick-fix loan that serves to fill a gap in financing.

For example, an investor may need short-term financing to rehab and flip a property, but might not have good credit or the necessary documentation to get approved with a retail bank.

Additionally, our investor may not have 30 days at their disposal to get the necessary financing in order. These types of loans can be closed both quickly (say 7-10 days) and more easily (less documentation).

Hard money loans might be described as a notch below subprime offerings, and often the last possible way of securing financing.

Hard Money Loans Are Often a Last Resort

- Because the interest rates are high

- And the terms generally not very attractive

- Hard money loans are a loan of last resort

- But it might be your only choice and ideally temporary

As noted, they are typically the last resort for borrowers who simply can’t find home loan financing due to poor credit profiles, unverifiable income and/or assets, unique properties, and so on.

In distressed situations, such as bankruptcy or foreclosures proceedings, hard money loans may be used as the one and only solution to avoid a complete loss.

Most hard money lenders will allow open NODs, charge-offs, notice of sale, bankruptcies, and more.

Hard money lenders usually take a more conservative value approach than the standard appraised home value larger banks and lenders rely upon.

The liquidity of the property is especially important to these types of lenders in the event of a default, which is much more common with hard money loans than bank issued loans.

In the past, these lenders would allow high loan-to-values (LTV) ratios, but after getting burned in the 1980s and 1990s, many now only offer loan-to-values between 60-80%.

This equity buffer protects them in the event things go south with the borrower.

They’ll generally use the value of the home “if sold today” as collateral for the loan, and often assume the first-lien position, which ensures they get paid first in the case of a default.

Hard Money Interest Rates Can Be Pretty High

- While hard money interest rates will vary just like standard mortgage interest rates

- Expect a much higher rate relative to what you see advertised in the traditional mortgage market

- Similarly it will depend on the amount of risk your loan scenario presents to the lender

- The good news is the loan shouldn’t be kept for too long…

You might see the term “fast money” alongside them, or be told that no documentation is required. That might be true, but expect to pay for that convenience.

Hard money lenders determine interest rates the same way a retail bank does, expect they charge a lot more.

So while there will be some level of risk-based pricing, which varies by scenario, expect a much higher interest rate.

They can range between 7-20%, and even higher if the borrower defaults on the hard money loan.

The cap is typically as high as the law allows, and can vary by state. They typically charge a large number of origination points on the loan as well. In other words, expect to pay to play.

While this may seem like predatory lending, it might be in the best interest of the homeowner as it provides a solution to avoid losing equity in their home if forced to execute a quick-sale or another unfavorable scenario.

Most loans are structured as balloon payments due 1 to 2 years after the loan is issued, so the financing is expected to be short-term like a bridge loan.

Some even come with flexible payments such as an interest-only option. And many of them offer generous approval terms such as “1 credit score OK”, no asset or income verification, and no verification of employment.

Be sure you have the money to make your monthly payments or the hard money loan will simply add to your financial woes.

These types of loans are really offered as a lifeline, and should be treated as such.

If you know you won’t have the money to make the payments, it might be in your best interest to sell the property before incurring greater amounts of debt.

When looking for a hard money lender, prepare to search locally as many of these types of lenders are smaller shops. National lenders are out there too, but may offer more conservative terms than a local company.

As with any financial transaction, practice extreme caution when dealing with these types of companies, as fraud and predatory lending are rampant in situations where a borrower is fragile.

Nowadays, many non-QM lenders fill the same needs as someone looking for hard money, so you may want to consider the non-QM route as well if you’re in need of creative financing.

- Soft Jobs Report Takes Pressure Off Mortgage Rates - July 2, 2026

- Kevin Warsh Throws Cold Water on Lower Mortgage Rates - July 1, 2026

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026

Hi,

I have a rental property w a hard money 2nd that needs to be taken out prior to a sale date 14 days away. The property is well located in west la with around 65% ltv now, including the hard money of $220,000 plus 20k-30k of cost and first of about $540,000. It appraises out around $1,200,000. Bad credit now is also issue, but property w lots of credit and could take out additional loan funds to include payments. Could you get this done?

Hi Richard,

Our site doesn’t provide loans directly, but maybe a hard money or non-QM lender could help for your situation.