Getting a mortgage is never a sure thing, even if you’re the richest individual in the world. And even if you have a perfect 850 FICO score.

There are a ton of underwriting guidelines that must be met to qualify for a home loan, both for the borrower and the property. So even the most creditworthy borrower could still run into roadblocks along the way.

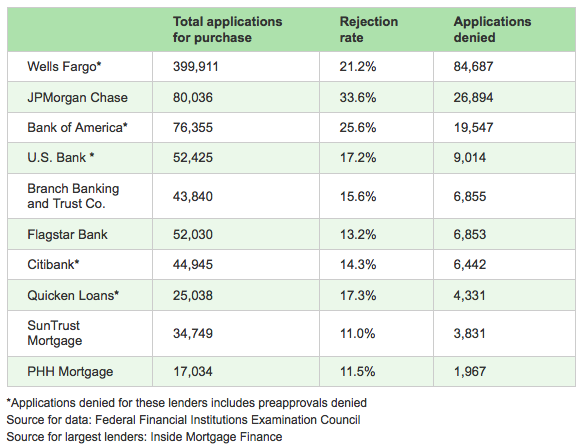

Last week, the Federal Financial Institutions Examination Council (FFIEC) released Home Mortgage Disclosure Act (HMDA) data for 2012.

Though mortgage lending was up a big 38% from 2011, there will still thousands of declined mortgage applications.

In fact, the top mortgage lender in the United States, Wells Fargo, denied 84,687 of the 399,911 home purchase applications it received (21.2% rejection rate), including those that were pre-approved, according to a Marketwatch analysis.

Rejection Rates by Top 10 Mortgage Lenders in 2012 (Purchases)

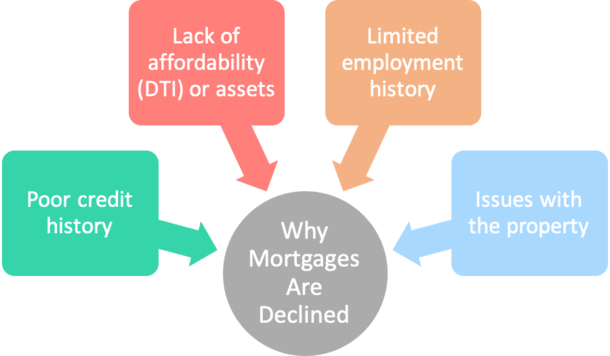

Reasons Why Lenders Decline Mortgage Applications

- Inadequate credit history

- Lack of affordability due to limited income

- Insufficient job history

- Lack of funds for down payment, closing costs, and reserves

- Issues with the property (as opposed to the borrower)

While the possibilities are endless, I can provide several reasons why a mortgage loan might be declined.

Credit History

Let’s start with credit, which is a biggie. First off, if your credit score isn’t above a certain level, your home loan application might be declined.

While the FHA permits financing with credit scores as low as 500, most individual banks have overlays that call for higher scores. So if your score isn’t say 640, you could be denied.

Even if you credit score is above a key threshold, a lack of credit history could prevent you from obtaining a mortgage. What this means is that those who didn’t open enough credit cards and other loans (student loans, auto loans/leases, etc.) prior to applying for a mortgage could be denied.

Seems unfair to be punished for not using credit, but mortgage lenders need to measure your creditworthiness somehow, and without prior datapoints it can be difficult to impossible to do so.

Staying in the credit realm, what’s on your credit report could hurt you as well. If you have recent mortgage lates, you could be denied for a subsequent mortgage.

The same goes for past short sales, foreclosures, bankruptcies, and so on, though the FHA has recently eased guidelines on that front.

Another credit issue that comes up is when borrowers make the mistake of opening new credit cards or other loans during or just before the mortgage approval process.

Doing so can hurt your credit score and/or increase your total monthly liabilities, which could kill your application in the affordability department.

Affordability and Income

Speaking of affordability, if you don’t make enough money for the mortgage you’re trying to qualify for, you could be denied. Banks have certain DTI ratio maximums that are enforced, and if you exceed them, you’ll be declined.

So attempting to borrow more than you can afford can easily lead to a denied app.

Where that income comes from is important as well. If you’ve only been at the same job for a few months, or less than two years, you’ll have some explaining to do.

Underwriters want to know that your income is steady and expected to be maintained in the future. If you just started a new job, who knows if you’ll last.

The same is true about sharp fluctuations in income – if your income all of a sudden shoots up, the underwriter might not be convinced that you’ll continue to make that amount of money until it’s proven for at least a couple years.

There’s also the odd chance that mortgage rates jump and if you don’t lock in your rate, you could fall out of affordability.

Assets and Down Payment

Another common problem is coming up with the necessary funds to close your loan. Generally, you need both down payment money and reserves for a certain number of months to show lenders you can actually pay your mortgage.

If you aren’t able to come up with the money, you could be denied, especially if there are certain LTV limits that must be met.

And if you try to game the system by depositing money from family or friends in your own account at the last minute, you’ll likely be asked to document that money or risk denial.

Property Issues

As I noted earlier, it’s not just about you. If the property doesn’t appraise, the loan will be put into jeopardy. If it comes in short, you’ll need to bring more money in at closing, and if you don’t have the money, you might need to walk away.

There are also those who try to convince lenders that a property will be a primary residence, when in fact it’s a second home or an investment property. This is a common red flag that often leads to a denial.

For condo or townhouse buyers, there are additional hurdles that involve the HOA and the composition of other owners in the complex. If too many units are non-owner occupied, or the HOA’s finances are in bad shape, your mortgage could be declined.

Even if it’s a single-family home, if there’s something funky going on, like bars on the windows or some kind of weird home-based business, financing might not happen.

There’s also good old-fashioned lying and fraud – if you attempt to pump up your income or job title, and it turns out to be bogus, your application will get declined in a hurry.

If you are denied, it’s not the end of the world. Simply determine what went wrong and look into applying with a different bank, perhaps one with more liberal guidelines. Or ask for an exception.

Of course, you might just need to wait a while if it’s a more serious issue that can only be cured with time, which is certainly sometimes the case.

Condensed List of Reasons Why Mortgages Get Denied

1. Loan amount too big

2. Income too low

3. Inability to document income

4. Using rental income to qualify

5. DTI ratio exceeded

6. Mortgage rates rise and push payments too high

7. Payment shock

8. LTV too high

9. Inability to obtain secondary financing

10. Underwater on mortgage

11. Not enough assets

12. Unable to verify assets

13. No job

14. Job history too limited

15. Changed jobs recently

16. Self-employment issues

17. Using business funds to qualify

18. Limited credit history

19. Credit score too low

20. Spouse’s credit score too low

21. Past delinquencies

22. Past foreclosure, short sale, BK

23. Too much debt

24. Undisclosed liabilities

25. New or closed credit accounts

26. New/changed bank account

27. Credit errors

28. Unpaid tax liens

29. Unpaid alimony or child support

30. Divorce issues

31. No rental history

32. Fraud/lying

33. Undisclosed relationships with seller (non arms-length transaction)

34. Attempting to buy multiple properties

35. Property doesn’t appraise at value

36. Defects with property

37. Home business on property

38. Non-permitted work

39. HOA issues

40. Investor concentration in complex too high

41. One entity owns too many units in complex

42. Title issues

43. Lender overlays

44. You own too many properties

45. Co-signer for other loans

46. Property not really owner-occupied

47. Layered risk (lots of questionable things added up)

48. Incomplete application

49. Inability to verify key information

50. Plain old mistakes

(photo: recoverling)

- Mortgage Rates Hit New 2026 Highs - May 15, 2026

- No, Kevin Warsh Isn’t Coming to Save Mortgage Rates - May 14, 2026

- Most Home Sellers Are Also Home Buyers: Why That’s a Problem Today - May 13, 2026

This is exactly why you should use a qualified mortgage broker to help you organize and present your loan file to the lender after all the potential mistakes and red flags are addressed and taken care of. Otherwise it’s in the lender’s hands and likely to too late to fix any issues.

That’s true! Don’t deal with big bureaucratic banks… Use a qualified independent mortgage broker, they want you in business and they will work their best …

We recently tried to get mortgage from Wells Fargo, we where told we’re approved, paid $450 for an appraisal wich came good – twice the amount we wanted to borrow from the bank… two weeks before closing we received a letter which stated that our application was denied due to history with prior lenders… Gues what – on the house we sold the mortgage was with Wells Fargo…

Any way my point is do not pay a penny for appraisal or any thing else until you are 100% sure ” You’re Application Has Been Approved”

Thank You! Blessings!!!

Hi Every One!

Same Guy who wrote the comment above…

First of all I want to apologize to Wells Fargo.

Twenty minutes ago I checked my bank account and I found that there’s a deposit of $455 to our account – This is actually a return we paid for the appraisal.

This makes me change my mind about Wells Fargo and I start to understand how serious the bank is !

I want to say Thank You for being kind and honest!

And I wish You helped us with this refinancing we need, we worked with you before and everything went fine…

Any way we just started a new application with a mortgage broker, hopefully it will go nice and smooth this time…

Thank You! Blessings!!!

I have an mortgage lender that I’m working for an she keep changing my mortgage payment. It’s getting higher and higher I’m suppose to go meet with her to find out these issues. Why u suppose what going on

Quicken Loans just denied me a refinance loan, on the grounds of, that my tax write offs are too high? I am an over the road truck driver earning 60 to 70 thousand a year. I get to write off travel expenses food and lodging excetra. Last year I wrote off $20,000 in expenses, and because of that I have been penalized and denied a loan. I was told I was approved twice by them. And they also made me pay $400 for an appraisal which of course I’m out now WTF!

I am also applying to well Fargo to finance a condominium,the appraisal is coming up next week.I already paid for it before I get approve,been pre approved.If they deny my application.Is that true you get the money back if denied?

Mendez,

I don’t know their policy but generally appraisal fees are non-refundable. You may want to verify with Wells Fargo directly.

Wells Fargo just turned us down. Everything was perfect EXCEPT we let our time share payments run behind. We did this intentionally in an effort to get rid of them, there is no way to get rid of them.

They don’t even show up in our Credit Karma report. But they show up when Wells Fargo checked.

The guy at Wells Fargo was very nice but he couldn’t help us. He recommended going to a local bank.

Any suggestions?

In the meantime NEVER buy a time share no matter how great it sounds. They don’t even go away when you die.

Liz,

That’s a new one I didn’t have in my great big list…but it makes sense…being late on other obligations can sink your mortgage application too. Not sure there’s any way around it, best to ask Wells directly then if they say no look at other lenders/brokers who might be able to help.

Just what do those “explanation letters” mean? My wife still has 2 charge offs on her credit file. Both are outside the Statute of Limitations for suit and will age off her credit file some time this month. One of the mortgage banks wants an letter of explanation why they were not paid. Do they really care or is this “banker-ese” for “no loan”? What constitutes a legitimate explanation? The reason is simple – in the 2008 crash we got hit hard. We held it together as long as we could but with her losing her job and my business tanking we paid what was most important – the mortgage and everything else had to slide. We even took employment outside the country because she couldn’t find anything in the good old USA. That was 7 years ago and the FCRA Statute is quickly ticking.

Transunion 676 (score crashed after ATT reported a box that was never returned) but when my lender ran my score TU is showing 602. Tomorrow I find out if I’m eligible or not. Is a 74 point difference normal or a scam? I have a good career and am progressing … I simply neglected to return an outdated piece of junk to a multi billion dollar company – and the punishment is unfair and great. Confused.

Dannie,

That’s pretty harsh, but not out of the realm of possibilities depending on how the incident was reported. You may want to work on making amends with AT&T and getting that derogatory mark removed from your credit report. Some experienced loan officers are good at cleaning up credit before applying for a mortgage. A 602 credit score can definitely disqualify you from certain types of mortgages, not to mention raise your rate if you are approved.

I got a new one. Apparently our property is underutilized. Borrowing 160k for property valued over 440k. Credit approved sufficient income . has anyone had this issue? We were in escrow and it all fell apart. Help

Martha,

Did that result in a low appraisal? And if so, what was the rationale behind the decision by the appraiser?