Here’s some Q&A with regard to the home loan approval process: “What do underwriters do?”

Once you actually apply for a home loan, your mortgage application will be organized by a loan processor and then sent along to a loan underwriter, who will determine if you qualify for a mortgage.

The underwriter can be your best friend or your worst enemy, so it’s important to put your best foot forward.

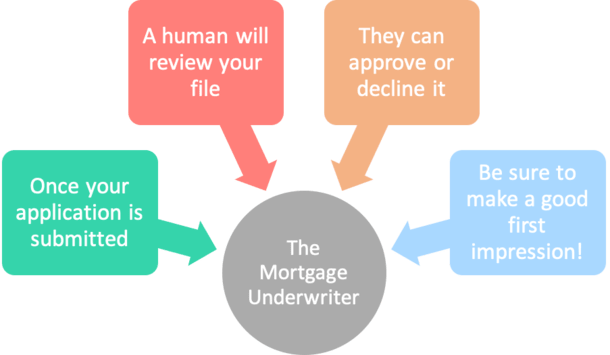

The expression, “you’ve only got one chance to make a first impression” comes to mind here.

Trust me, you’ll want to get it right the first time to avoid going down the bureaucratic rabbit hole.

The Underwriter Will Approve, Suspend, or Decline Your Mortgage Application

- After you formally apply for a home loan your file will be submitted to the underwriting department

- A human underwriter will then review your loan application and decision it

- Their job is to approve, suspend, or decline your application based on its contents

- It’s paramount to submit a clean file to boost your chances of loan approval

Simply put, the loan underwriter’s job is to approve, suspend, or decline your mortgage application.

If the loan is approved, you’ll receive a list of “conditions” which must be met before you receive your loan documents. So in essence, it’s really a conditional loan approval.

If the loan is suspended, you’ll need to supply additional information or loan documentation to move it to approved conditional status.

If the loan is declined, you’ll more than likely need to apply elsewhere with another bank or mortgage lender, or take steps to fix whatever went wrong.

The Three C’s of Mortgage Underwriting

- Credit – payment behavior over time (your credit report)

- Capacity – ability to repay the home loan (your income and assets)

- Collateral – value of the underlying asset (the property)

Now you may be wondering how underwriters determine the outcome of your mortgage application?

Well, there are the “three C’s of underwriting,” otherwise known as credit reputation, capacity, and collateral.

Credit reputation has to do with your credit history, including past foreclosures, bankruptcies, judgments, and basically measures your willingness to pay your debts.

[What credit score do I need to get a mortgage?]

If you’ve had previous mortgage delinquencies or even non-housing related delinquencies, these will need to be taken into account.

Typically these items will be reflected in your three-digit credit score, which can actually eliminate you from contention without any further underwriting necessary if you fall below a certain threshold.

For example, you need a 620 FICO for a conforming loan and at least a 500 score for an FHA loan.

Your history supporting significant amounts of debt is also important; if the most you’ve ever financed has been a plasma TV, the underwriter may think twice about approving your six-figure loan application.

Capacity deals with a borrower’s ability to repay a loan, using things like debt-to-income ratio, employment history, salary, cash reserves, loan program and more.

In short, the underwriter wants to know that you can pay back the mortgage you’re applying for before granting approval.

[How much house can I afford?]

Finally, collateral involves the borrower’s down payment, loan-to-value ratio, property type, and property use, as the lender will be stuck with the home if the borrower fails to make timely mortgage payments.

A home appraisal will be ordered to determine the value of the property using an independent appraiser.

Mortgage Underwriters Consider Layered Risk

- They don’t just look at one aspect of your borrower profile in a vacuum

- They consider all factors together to make a sound underwriting decision

- Those with risk in one area who are able to compensate for it may be approved

- While those with issues in all areas might be denied due to layered risk

Now it’s important to understand that the three C’s are not independent of one another.

All three must be considered simultaneously to understand the level of “layered risk” that could be present in said loan application.

For example, if the borrower has a less-than-stellar credit score, limited asset reserves, and a minimal down payment, the risk layering could be deemed excessive, leading to denial.

Consider a home buyer with zero down payment, a 600 FICO score, and only $1,000 in the bank, who just started a new job.

Conversely, consider a home buyer putting down 20%, with a 760 FICO score and $50,000 in cash reserves, who has worked the same job for a decade.

Obviously the second borrower sounds like a much better candidate for a mortgage.

This is the underwriter’s discretion, and can certainly be subjective based on other factors such as their occupation, how long the borrower has been in the line of work, why the credit score is less than perfect, and so on.

The underwriter must decide, based on all the criteria, if the borrower is an acceptable risk for the mortgage lender, and if the end product can be resold without difficulty to investors.

Layered risk is a major reason why the mortgage crisis got so out of hand.

Countless borrowers applied for mortgages with stated income and zero down financing, which is certainly very high risk, and were easily approved.

Rising home prices covered up the mess for a while, but it didn’t take long for everything to unravel. This is why sound mortgage underwriting is so critical to a healthy housing market.

What Shouldn’t You Do During Underwriting?

One last thing. When the underwriter is working to decision your loan file, you as the borrower should do your part as well.

This means NOT applying for new lines of credit, such as a credit card or a new auto loan. And not making large purchases.

If you do, they could show up on the credit report or be reflected in your credit scores. The last thing you want is a lower credit score to jeopardize your loan application.

The same goes for moving assets around from one bank account to another, or switching jobs. It might sound crazy, but just about anything you can think of has happened.

Long story short, you want to remain in a holding pattern while your home loan goes through underwriting and ideally gets funded.

Once the loan is funded and recorded, you can go on about your business, whether it’s buying new furniture or applying for a new credit card.

But until that time, you can make life easier for everyone (including yourself) by doing nothing!

What You Should Do Before Underwriting

I talked about what you shouldn’t do, but what about what you should do? Well, I’ve actually dedicated an entire post to this, but let me quickly get you up to speed.

Rent first to build a solid rental history and get used to living on your own. Check your credit report and scores each week or month and over time. Any necessary improvements or fixes will take time.

While you’re at it, pay down any outstanding debts to improve your scores and also boost your purchasing power. Fewer liabilities mean you can borrow more for a home purchase.

Put any unnecessary spending on hold and get your assets for down payment and reserves into a dedicated account, like a savings account, several months in advance.

Continue to remain employed at your current job (yes, I have to say it!), squirrel away money, and better educate yourself on the mortgage process. Learn the lingo while you’re at it!

Lastly, think of any red flags that might come up if an underwriter digs through your financials. Instead of hoping they don’t notice, address it NOW so it’s not a problem later.

If you’re worried about something, don’t put your head in the sand. Fix it. Underwriters are smart.

This can help you avoid having to write a letter of explanation if something comes up during the loan process.

And always, always, always cooperate with the underwriter!

Mortgage Underwriter FAQ

Do underwriters work for the bank/lender?

Yes, underwriters are employees of banks, lenders, and mortgage bankers. They work on the operational side of things, making loan decisions after the sales team brings the loan in the door. This means they work in the same building as the sales team.

How long does underwriting take?

It might only take an underwriter a few hours to comb through a loan file and approve, suspend, or deny it. However, mortgage lenders only have so many underwriters available, and surely the number of loans in the pipeline will exceed the number of staff. As such, much of the time might be waiting in the queue until a pair of eyeballs actually look over your loan.

So if you’re wondering how quickly can underwriting be done, it may depend on how busy the company is and if there’s any backlog. Once your file does get in front of an underwriter, the average time for underwriting is pretty quick, often 24 hours or less.

Why do underwriters take so long?

Hmm…I don’t know, because they’re approving a six-figure loan amount, or seven, to a complete stranger. As noted, the actual underwriting might not take that long, but the amount of available underwriters (humans) might be low. So you could just be in the queue. A clean loan file will get approved faster and with fewer conditions so get it right before the underwriter even sees it.

Do underwriters verify employment?

While employment is generally verified nowadays when you take out a mortgage, it might not be the underwriter verifying it. Instead, the loan processor may obtain the verification of employment (VOE). Many use the “The Work Number,” an independent third-party employment verification company now owned by credit bureau Equifax.

So the underwriter probably won’t call your employer, but your employment will be verified one way or another.

Should I be worried about underwriting?

The decisioning of your loan can definitely be nerve-racking, but this is why your loan officer or broker (and processor) works diligently to get all your ducks in a row before loan submission.

If you address any and all possible red flags before you submit your loan to underwriting, you should feel a lot more at peace with it. There’s always the chance of loan denial, but submitting a clean file is a great way to improve your chances of approval!

How much do loan underwriters make?

They can make pretty good money. Salaries may be in the high five figures to low six figures if they’re seasoned and skilled in underwriting all types of loans, including FHA, VA, and so on. If you start as a junior underwriter the salary could be less than $50,000. But once you become a senior loan underwriter, the pay can jump up tremendously. It may also be possible to earn overtime.

Do underwriters make commission?

They shouldn’t because that would be a conflict of interest. They should approve/deny loans based on the characteristics of the loan file, not because they need to hit a certain number. Compensating them for loan quality might be a different story, but again could lead to discrimination if they cherrypick only the best loans.

Do underwriters work weekends?

I’ve heard of some that have. I don’t know if they do on a regular basis, but if loan volume picks up in a short period of time it’s possible to come in on a Saturday or Sunday. The mortgage world is all about highs and lows, so sometimes it might be slow and other times it’s impossible to keep up.

Underwriters probably worked weekends in 2020 and 2021 when refinance volume was through the roof, but nowadays it’s likely not very common.

Are underwriters warm and friendly?

They can be if you don’t rub them the wrong way. I look at mortgages kind of like the DMV. Show up with the right paperwork and a good attitude and you’ll get in and out before you know it. Do the opposite at your peril!

(photo: Joelk75)

My husband recently switched from employee to contractor that receives 1099. We are being told that regardless of credit score and down payment we will have to show 2 years of Self Employment tax returns in order to be considered. Is there any way around this and if we apply will we considered at all?

Hi Renee,

Changes in employment can present challenges, especially going from W-2 to self-employed, and certainly if it’s less than two years. But if he’s been doing it over a year and it’s in the same line of work and an equal or better position than his former one, it may be possible to get financing. It might be best to speak with a broker or two so they can scan their range of offerings to see what lenders might be willing to help. And maybe also reach out to some portfolio lenders who keep their loans and thereby underwrite a bit differently.

if i have less than stella credit and a student loan in default, which is now being rehabilitated, how can i get my pre approval from a lender, ??

Rad,

You may still be able to get approved but it’s probably better to apply when your credit score is higher…lower rate, more options.

I included my home in a bankruptcy 5 years ago but the mortgage company has failed to foreclose on the loan, I have reestablished my credit and have a good credit score can I still buy a home?

So I have no credit. It’s not been established and I’ve also never made a large purchase, so i feel as if we would get laughed at. Nearing 30 would love to pay toward owning a home, our home. What are options for someone who doesn’t have a credit report,or a larger purchase, But a good income and years of management for the same company.

Jessica,

A lender might be able to use alternate credit such as utility bills, cell phone bill, etc. But it’s better to have a car loan/lease and/or some credit cards with some years of history on each line to make qualifying a lot less hassle-free. Good luck!

My fiancé is currently in the process of purchasing a new home. He was approved for the loan, and then they started asking for other things. He did what they asked, and now we can’t close. If he was already approved, why are we still dealing with underwriter?

Caitlyn,

Could be a million different reasons. Every time new information is shared with the lender there’s a possibility for denial or the need for additional documentation. Sadly it’s a very intensive, bureaucratic process. Best to ask the lender directly what is needed and why.

I had past payment problems on my last house due to a child being born 4.5 months premature and having to pay for a lot of dr. Bills and testing. Now my son is fine and we have another child and need to move into a bigger house. The end result I filed chapter 13 100% repayment plan in 2012 paid it all in full in just one year. since then I haven’t been on any payments credit cards or mortgage and my signature loan with my bank has been paid on time and almost paid off my credit score is a 681 717 677 idk why transunion is higher than the others. But will a underwriter deny me because of my past payment problems although I’ve had no late payments in over 3 years?

Jay,

There are waiting periods to get a mortgage after filing BK, but if extenuating circumstances can be documented the period is much shorter. Depends on the type of loan and what you can prove.

Colin,

I am going the USDA route, I am very close to the income cap limit to qualify. I am just curious if underwriters are able to get some real time report from the gov that says you have had withholdings from your employer therefore your income or do they take your income verification straight from your paystubs.

Thanks!

Nick,

The USDA is pretty strict when it comes to income to ensure the loans go to those who need them. They’ll likely ask for paystubs and W-2s and consider household and projected income.

Colin,

I have had rental issues that are on my credit report from the past 6 years. My report is at 676. My husband and I have been pre approved for a loan his score is a 767. What are the chances we may be denied?

Kay,

Credit score is just one piece of the pie. Your score could certainly be better but it being low may just affect the rate you receive, not whether you are approved or not. Good luck!

Colin,

Can a underwriter deny your loan if they feel you you came off wrong and have a bad attitude? Can you fight it, meaning go over their head and talk to their manager? This happened to my fiancé. The underwriter denied his loan cause he came off wrong. He was just confused because she asked the same questions as the sales guy.

Candace,

That’s strange and hopefully not the case. Underwriters shouldn’t factor in one’s attitude as the process should be objective and based on the facts not emotion.

I’m 3 weeks in closing and because my boyfriend the Co signer cannot guarantee 40 hours but we can 2 weeks just not the other 40 we are being denied is that possible??

Jazmin,

It sounds like his income is being scrutinized, probably best to work with the underwriter/loan officer to determine how to get around the issue if at all possible.

We’re so close! Our house is being built. Apparently, my husband’s scores are fine, and he gets a VA loan, but my median score using my mortgage guys system is a 588, and I need to be at least 600 to be a co borrower. I’m working with a credit repair company, but I’ll be devastated if this doesn’t go through. Thoughts on rental karma to bring up my score and becoming an authorized user on my brothers card to lengthen my history? Do we have a chance? Closing May 20th!

Debra,

Hmm…not sure if the authorized user data will bring up your score that quickly, but it’s possible. Any large revolving balances you can pay down in the meantime while also making sure you don’t mess with your cash reserves for the mortgage? Good luck!

I’m trying to buy a house my fico score is only 606 but my boyfriend is 654 now the lender is telling me that my income is not good cause my taxes from last year I added self employ but this year I still work for the same company should I go to a different place?

Yaniris,

You can always get a second or third opinion but your FICO scores certainly could use some major improvement, and the self employment income formula is pretty complex depending on what it is you do.

I have money save will the underwriters want to know how I got the money

Deborah,

Depends how long the money has been in verifiable accounts…if it’s been in the account for 60+ days no explanation may be needed, if less you will likely need to explain and paper trail deposits.

Hi Colin,

I actually have a question about becoming an underwriter. I just started with my research but this is a career I am highly interested in and would like to speak with someone to get more information in terms of education, training, certification, etc. I have a degree in Accounting, could you tell me what steps I can take for this career.

Mahalo,

Donneshia McCants

Hi Colin,

I have some conflict. I want you to give your opinion. I’m a fresh graduate that have degree in finance. Recently, I’ve got an offer to work as account assistant. I’ve accept it. But, now I have got an offer from a company that offered me as an underwriter. Do you think I should accept it or not? Thankyou.

Sheera,

I don’t know what an account assistant is…so it’s hard for me to offer an opinion, but hopefully my description of an underwriter will give you some idea of what the job entails.

Underwriter wants college transcripts to verify former part-time work status. If I provide this item, are they really going to call my school and verify if I provide official transcripts?

Joe,

Not sure Joe, but if you’re worried about something if they do call you might want to be prepared to explain it.

I’m have been conditionally approved for a refi. I have credit over 700 and more than enough equity. My concern is that I am part W2, part I-9 and part cash income, as I nanny. One of my w-2 incomes ended in July. It was a nanny position. I have more than enough cash income from other nanny families, to make up for that. Will they take VOI from them? I have been in childcare for over 20 years so its not a new employment field.

Donna,

You’ll likely need to prove that the income you’re currently earning is stable, ongoing, and can be documented. May want to discuss with your loan officer to ensure there aren’t any hiccups.

Hi Colin,

I’m a recent college grad with no prior work experience working on getting my MLO license I just need to take the national exam and I get licensed. But I hear it would be a better option for me to work for a bank to get experience. I live in South Florida, what do you suggest I do ? I find the underwriting more interesting but how do I get my foot in the door with no experience what so ever and a BA degree in Accounting.

Thanks, Felipe

Felipe,

Not sure why a bank would give you more experience versus working for an independent lender or a broker. In fact, you might learn more with the latter because they often work with more loan programs, fewer automated systems, etc. The MLO vs. underwriter positions are quite different, with the former being a sales job and the latter an operations job. Generally, you can get the MLO with no prior experience but underwriters tend to need degrees and some experience, or start as junior UWs. Good luck!

Hi Colin

My wife was pre-approved in late August for a loan for a new construction loan (I will not be on the loan). After she was pre-approved I received a gift from a friend and I gave it to my wife to use as the initial down payment (9k) – basically a gift to her. At the time I did not realize that these funds would need to become ‘seasoned’ in my account first, before I made the deposit/gift to her account. Since the home is new construction her pre-approval will go in to a hibernation until 60 days before close. At the 60 day mark, the lender will reopen the pre-approval, rerun the credit, and verify assets. When the re-open the pre-approval in February, she will have more than enough money for all of the down (including the 9k I gave her), as well as closing costs and reserves. Also, her debt to income is extremely low, and her credit is around 740. She also has stable employment at the same location for 17 years. Could the gift money be an issues when the underwriter looks at it again? He has already requested my bank statement from that time period.

Thank you, Eric

Eric,

Depends if they use more recent bank statements or the old ones and if so, will they allow gifts as long as they are sourced and paper trailed?

Collin,

Thanks for the quick reply we’re a little stressed out right now. They allow gifts that are sourced. When the pre-approval gets reopened in February, they want the December and January statements — these bank statements will only contain funds received via our direct deposit from our respective employers. It sounds like they want to see my statements from back in August where I received the gift and essentially gifted it to my wife within a few days.

Eric,

If they allow gifts and you can document it what’s the problem?

Colin,

My concern is that I received the gift money (I won’t be on the loan), and I then gifted it to my wife in the same week. After doing some research my understanding is that this money needed to be ‘seasoned’ in my account for at least 60 days.

Colin,

Will the underwriters deny your loan at closing

Albertina,

It’s possible if loan conditions aren’t satisfied, or if something comes up that can’t be resolved.

Hi Colin….my closing date is set for July 7th today i gave my loan officer and processor some documents they needed w2s check stubs bank statements divorce decree etc… When the processor got to my w2s it was a problem because i filed my 2015 w2 on my 2016 return the numbers didn’t add up so i had to show her my 2016 w2…long story short i had to call the IRS to get my tax transcripts and give them to her…so my question is will my w2/ returns get me denied at closing?

Zary,

Why do you think it’ll be a problem? Is the income not sufficient? Is there some other issue? Just because the underwriter is asking for more documentation doesn’t mean it’s a bad thing, it just means they need more information to make a sound lending decision.

Our situation:

Mine/my wife’s combined income: $200K+ (plus small income from owned condo with a renter paying us monthly)

Credit Scores: both 800+

Debt: None

Down Payment: 20% on a $1.1M home (saved)

Loan Pre-approved: Yes

Employment: Both full-time, though I’m a contractor (w/ complete tax records/returns from last 5 yrs)

– – – – – – –

My concern is when we’re scrutinized more closely (whatever that entails) by the Underwriter at closing.

Everything looks good, but I do have a little bit of history: Between 2008-2010 I had to do a “debt consolidation” on my credit cards. At the time this was the only way I could get out of credit card debt. All accounts were “settled” or “settled with derogatory marks,” So initially my credit score was probably as low as it could be. Since then, I have rebuilt my credit, financed and paid off a $40K car, never missed any payments on anything, never took on debt, etc. My credit score returned to 800+. So my question is, how likely will my past ‘misadventures’ (ended 2010) impact the underwriter’s decision for our loan?

Thank you for your time and advice,

Scott

forgot to add – we can show $100K in additional savings/assets.

Scott,

That stuff may not even show up on your credit report if it’s seven or more years old. Have you checked your own reports (all three bureaus) to see what’s on there still? Even if it is, your higher credit score now reflects the efforts you’ve taken to clean up past mistakes, and ideally an underwriter will understand that even if they do stumble upon anything. If there is lingering info, they may want an LOE (letter of explanation).

Hi, I’m about two weeks from closing on a FHA loan. I am using my tax return as the funds for a down payment on the home. I had placed 3k on one card and the remainder on my hr block card to save for funds for the down payment. At first they wanted just the hr block info on deposit from the taxes etc. Now they want the info on my other card for the other 3k. My question is, if there is enough on the hr block card for the cash to close, why would they want the info from my other card that has nothing to do with there money they are to receive? This makes no sense

Karman,

Once you disclose an account, underwriters typically want to see statements, even if there’s no specific reason.

Can underwriters email you if something goes wrong after the loan was given?

Joe,

You probably won’t have direct correspondence with the underwriter. But they may convey something to you via their loan officer or processor.

Hello,

I was pre-approved for a mortgage loan based on the typical factors. I had great credit but, Once it was sent to the underwriter the company pulled a different report other then my credit report which showed that I was late on my previous mortgage payment for 8 months straight so they asked for an explanation of why they were late. Which I provided, (I filed a Chapter 13 over 7 years ago and during the course of the Chapter 13, which was 5 years total, my mortgage payments were paid by the court appointed trustee, so I would send my mortgage payment on time to the Chapter 13 courts and then the Chapter 13 trustee would forward my payments to my mortgage lender, so I had no control over the payments making it to my mortgage company on time during the Chapter 13). So will this have a strong impact on my loan approval?

My home was sold about 3 weeks ago the loan was approved it was supposed to close on the 3rd of August which it didn’t and was sent to the underwriters and was supposed to close in a week then it was told to me that it was between the underwriters and the government why it hasn’t closed yet can you tell me what the government has to do with this Underwriters? Thank you

Catherine,

Either the home buyer/borrower took out an FHA or VA loan (they are government-backed) or it’s something to do with tax transcripts and the IRS. That’d be my guess.

Income to prove debt to ratio, is it true you only need to see amount(s) of deposit(s) for proof of income and not how much money I have in my account which shows on my statement. If so, is it not true I can black out account number, amount I have in account?

James,

Maybe for a so-called bank statement program that only focuses on deposits, but probably not a conventional home loan program. Generally, underwriters don’t like anything blacked out on financial paperwork.

My boyfriend and I were pre-approved for a mortgage. Seller had an open permit that needed to be fixed before closing. We waited, living with parents for 6+ months. During that time, we used some credit ($50/m increase) towards DTI. Everything was going smoothly and promptly sent requested documents. Comes underwriting and they have a problem with my bonus money. I’ve been with my employer for over 3 years and have increasing pay every year until now. LO wants a letter from my boss saying bonuses are likely to continue. BUT, I work for a Fortune 500 company. The HR and legal department STRICTLY prohibits any kind of endorsements of such. Now the LO sent an email to my company’s HR manager to hopefully get filled out. According to the LO, the investors of our mortgage want reassurance that my bonuses will continue, DESPITE it already showing an increase for 3 years in a row. If my HR manager doesn’t oblige or provide satisfactory documents, can we still get denied?

Tiffany,

You’ll just have to wait and see – generally, if things makes sense, loans get approved. And sometimes underwriters just want to establish the narrative that it all adds up.

You talk about being nice to Underwriters and I understand we have to be nice to everybody. But aren’t underwriters or the loan company obligated to give you a response on your loan in a specific period or time? Also, can they deny you a loan without good justification?

KB,

Underwriters are probably very busy at the moment with loan volumes unexpectedly higher (staffing levels are low), and in terms of a response time, it will vary by company. Any communication will probably come from an intermediary such as your loan officer, not the UW directly. They shouldn’t have any incentive to deny your loan, so it’s unlikely they would do so without justification. Aside from being nice, being cooperative is key to ensure you can get them whatever documents they need to feel comfortable approving a loan.

Good credit doing a 1031 exchange putting down $112,000 down on $370,000 pieces of rental property (duplex)which rent at $1350 per unit under have ask me for the same documents 3 time now and a a second appraisal said the units where deeded separately. I starting to feel like I’m being discriminate against. What can I do ? My final 1031 date is 10 December no time to look for another loan

Henry,

Ultimately, you want to satisfy any documentation requests the underwriter makes so they can approve your loan. If you believe you have and disagree with their assessment, you may need to provide an LOE and/or additional documentation to make it more clear. They should also want to approve your loan, they just need to feel comfortable doing so. Your loan officer should also be going to bat for you. Simply put, best to work together instead of arguing.

Husband and I got pre-approval for a VA loan. We have signed all the documents, they’ve pulled our credit, inspections have been ordered, down payment made, paycheck stubs have been furnished. They’ve set out closing date for 12/27. At what point do we know everything has gone through and closing is set in stone?

Sandra,

Once the underwriter actually approves the loan and any additional prior-to-doc conditions (if applicable) are met.

My husband was preapproved for a loan about 6 weeks ago. We have sold and purchased a new home. All these are supposed to close in a week. Our lender just told us the underwriter hasn’t even looked at our application yet. Is closing in a week even realistic timeframe?

Nicole,

It depends on their process – some lenders don’t have the underwriter look at the file until near the end. And if that’s the case, you’ll need to hope that everything is clean and there aren’t additional conditions. Also I assume the appraisal is already done. May want to call your loan officer and let them know the time issue so they can push it along.

I am purchasing a new built and my lender said closing date will probably be on July 17. I have already been pre-approved but I am still waiting on a answer from the underwriter. I am currently renting and so I want to give my 30-day notice on the 1st of July. I don’t want to pay August rent if I will be moving in July. Should I let my lender know so they can do the process faster.

TJ,

It never hurts to let them know your situation in the hope of expediting, but lenders are probably super busy at the moment, so it may take longer than expected to get a decision. Perhaps your loan officer can give you a sense of approval odds now so you have a better idea of where you stand, but nothing is guaranteed until it funds. Good luck!

I recently was signed over the deed to my house I am doing a refinance to pay off the mortgage that’s on the house. I pre-qualified and submitted bank statements, pay stubs, tax returns, w2’s. My loan officer submitted to underwriting how do they verify my information with the paperwork I submitted to the loan officer is that why I needed to submit those documents?

Hi Michele,

If all those documents came from certified sources they can use them to determine your debt-to-income ratio (vs. any liabilities on your credit report) to ensure you can afford a monthly mortgage payment on the property. Check out my DTI page to learn more about that process and good luck with your approval!

I was pre-approved for a 32,000 loan from my credit union in November. Closing was set for Dec. 28th. Dec 23rd my agent texted me that she had received nothing from the bank. I found out that both the loan officer and the underwriting officer went on vacation the 18th and won’t be back until the 28th. The agent said they need to close by the end of the year. Do I have any recourse? I supplied all the requested documents.

We’ve been approved for a VA loan. Appraisal has been done. Closing date is supposed to be today, but underwriter has not approved it. Underwriter keeps finding reasons not to sign. Is this normal? We’ve given everything they’ve asked for. Lender keeps saying we’ll close today, but how can that be if underwriter has not approved it. Extremely frustrated. I feel like I’m being strung along. This process began February 1, 2021.

We’ve been searching for a home for quite a while with no luck. I ended up getting surgery back in July and a week or two after the surgery we found a house and made an offer. Our offer was accepted and we’re scheduled to close on 9/14. On the initial application, my credit score was 760 but I didn’t realize that my credit was pulled before the $1600 was charged to my card for the surgery ($5000 credit limit).

What ended up happening after we were conditionally approved was the charge went through and I got ding’d for the hard inquiry and my credit dropped to 721 (because I exceeded 30% of the card’s limit). Since July I’ve paid it down to $600 which makes my DTI less than 1% and my credit score is back up to 745 but, all over the web I see, “don’t make any big purchases.” Does this sound like a scenario that may jeopardize our closing? I don’t consider this a “big purchase” because I have no other debt and I have 100% on time payments for over 7 years and it’s well within what I can afford but it sounds like these UW are pretty…. Strict.

I’m concerned it will be an issue because my credit score will be lower than what was reflected in my initial disclosure. Technically I didn’t make the “big purchase” after the loan process started but the credit card company only updates on the 2nd of every month so on the initial application it didn’t show up…

Patrick,

It sounds like you’ve been diligent and are tackling the issue. Hopefully a 740+ FICO is priced the same as a 760+ FICO. That’d probably be the only issue, assuming you have since paid down the purchase so DTI isn’t affected. The only other potential issue would be less assets if you tapped them to pay off that bill. But again, it may not be a concern if you have plenty in the bank. You can always ask your loan officer to be sure.

Others get into trouble because they make big purchases then don’t pay them off, which depresses their credit scores and raises their DTI. And if they’re already borderline, loan approvals can go south.

Good luck!

I had gone through 4 companies trying to get a mortgage. 3 ended up saying no after 3 weeks because it was a manufactured home. The 4th went all the way. Paid for appraisal and foundation inspection. Credit 800. Just when it was time to close underwriter said our condo association wasn’t approved. I asked why and they said because we don’t write an annual budget. It is small association 26 condos. No amenities to deal with. We have over a 10% reserve and just keep rest of money in checking account and when a bill comes in we pay it. How do we get the condo association approved? Tried emailing the underwriter to find out what they want us to do but they won’t reply. LO said to contact her and ask what we needed.

Mildred,

The LO should tell you what you need because they are the liaison with the underwriter. UWs don’t typically speak directly to borrowers.