Mortgage Q&A: “What is a streamline refinance?”

While qualifying for a mortgage refinance is generally a lot harder than it has been in the past (now that lenders actually care how your home loan performs), there are less cumbersome options available.

In fact, many lenders offer “streamlined” alternatives to existing homeowners to lower costs and make refinancing more accessible, knowing that borrowers simply want payment relief.

When you think about it, a mortgage with a lower interest rate should also be lower-risk, as the monthly payment will be reduced, putting less burden on the homeowner.

It is for this reason that “streamline refinance” programs are available with just about every bank and lender out there.

They come with looser credit scoring requirements, easier income and asset verification, and limited paperwork.

And in some cases, you don’t even need to order a home appraisal since collateral isn’t really an issue if you’re just swapping your mortgage for one with a lower rate.

Simply put, a streamline refinance takes a lot of the legwork (and time) out of the process, and may increase your chances of approval.

However, streamline refinances also come with their own list of requirements, namely that the refinance has a “net tangible benefit.”

In other words, it should help the homeowner, not just put money in the pocket of the loan originator (yes, they benefit too when you refinance by earning a commission).

This generally means that the mortgage rate should drop by an amount that will eclipse any related fees, and/or that the loan is converted from an adjustable-rate mortgage to a fixed-rate mortgage.

Ultimately, the borrower should have a cheaper home loan when all is said and done.

How a Streamline Refinance Works

Here’s a condensed list of possible streamline refinance guidelines, rules, and features:

- Must be current (not delinquent) on your existing mortgage

- Refinance must clearly benefit the borrower (e.g. lower payment or ARM to FRM)

- No cash out allowed (must keep loan balance the same)

- Limited income/asset verification

- Minimal credit requirements

- Less paperwork

- Faster processing

- Lower closing costs

- No appraisal necessary in some cases

*Keep in mind that these guidelines can vary widely from bank to bank, and by loan type, and not every lender will offer a streamline refinance, or approve you if they do.

Also note that a streamline refinance can take just as long as a regular refinance. They aren’t necessarily faster, they’re just meant to be easier to qualify for.

Now let’s talk about the different types of streamline refinance options available today.

FHA Streamline Refinance

- Loan must already be FHA-insured (aka an existing FHA loan)

- The borrower must be current on payments (not delinquent)

- The refinance must result in a tangible benefit (lower mortgage payment or safer loan program)

- No money can go to the borrower (in excess of $500 in incidental cash)

Perhaps one of the most popular and well-known streamline refinance options out there comes courtesy of the FHA.

In fact, the FHA has permitted “streamline refinances” since the early 1980s, making them a pioneer of sorts in the business of expedited mortgages.

They became much more popular after the most recent mortgage crisis, which brought down home values tremendously and made it difficult if not impossible to refinance in traditional fashion.

An FHA streamline refinance makes it easy to refinance your mortgage to a lower mortgage rate without the need for an appraisal, many of which happened to come in low a decade ago.

In fact, if an appraisal is conducted and it’s not favorable, the FHA will even allow lenders to ignore it and set it aside.

Now this isn’t as much of an issue these days, but if and when property values crater again, it could be beneficial for some homeowners.

Additionally, because there is no credit scoring requirement and limited documentation requirements, most borrowers can qualify for an FHA streamline refinance quite effortlessly, even if they don’t have adequate income, assets, or employment.

These are known as “non-credit qualifying” streamline refis because the typical in-depth underwriting process is avoided.

It should be noted that while the FHA doesn’t require a credit report, the individual lender might as part of their own guidelines (lender overlay). Or they may just ask for a mortgage-only credit report.

The idea here is that a borrower with smaller monthly mortgage payments is a less risky borrower, which is good for the FHA.

So even if it sounds risky to give a homeowner a new mortgage with very little paperwork, they’re actually just being given a more affordable home loan when all is said and done.

For example, if their existing payment is $2,000 per month and a streamline refi can get their payment down to $1,500 per month, chances are they’ll have an easier time making payments.

And there’s a better chance they’ll stay current on their mortgage, which is good for everyone, including lenders, mortgage investors, and the FHA. Of course, it’s never a guarantee.

Use a refinance calculator to determine how much you can save in the way of monthly mortgage payments.

There are just a handful of simple requirements necessary for approval.

As long as your existing mortgage is an FHA loan and in good standing (not delinquent), and the refinance will result in a lower monthly mortgage payment (or you’re converting your ARM to a FRM), you should be good to go.

You can even streamline a 203k loan to the standard 203b FHA loan program with some lenders.

Note that there are cases when income will be verified and DTI ratios computed, but only if the refinance increases the mortgage payment by 20% or more, if a borrower is removed triggering the due-on-sale clause, or following a loan assumption.

In these scenarios, a streamline is still possible but it has to be “credit qualifying,” which is a bit more involved underwriting wise.

FHA Streamline Seasoning Requirements

Aside from the details discussed above, there are seasoning requirements that must also be met for FHA loans, including the following:

– you must have made at least six (6) payments on the FHA-insured mortgage before refinancing

– six (6) full months must have passed since the first payment due date of the original mortgage

– 210 days must have passed from the closing date of the original mortgage

If the loan is less than 12 months old, you aren’t allowed any mortgage lates.

If it’s greater than 12 months, you are permitted no more than one 30-day late payment in the preceding 12 months.

And the three most recent payments must have been timely.

Also note that no cash out can be taken out via a FHA streamline refinance. Only rate and term refinances work here.

However, you can get your hands on a no cost refinance, meaning you won’t necessarily need to pay out-of-pocket expenses, but you’ll be stuck with a higher interest rate in return.

This is common because the FHA doesn’t allow lenders to roll closing costs into the new mortgage amount on a streamline refinance without an appraisal. And most people gravitate to this program for that appraisal waiver.

To sum it up, because no appraisal is required, the FHA streamline refinance is an excellent option for those who are underwater on their mortgages, of which there are many.

Tip: President Obama lowered mortgage insurance premium costs on FHA Streamline Refinances to help more borrowers take advantage of the record low mortgage rates currently on offer.

Those refinancing an FHA mortgage endorsed on or before May 31st, 2009 pay an upfront mortgage insurance premium of just 0.01% and an annual MIP of 0.55%.

VA Streamline Refinance Requirements

- A streamline is also possible for those with VA loans

- It’s known as an Interest Rate Reduction Refinancing Loan (IRRRL)

- The loan process can be very quick and easy

- And doesn’t require a home appraisal or a COE

The FHA isn’t the only one offering streamline refinances. The VA also offers a streamlined “VA loan to VA loan” refinance, known as an “Interest Rate Reduction Refinancing Loan,” or IRRRL for short.

Yes, that’s a lot of “R’s,” but a VA streamline refinance is easy to execute and can save you a lot of money now that mortgage rates are so low.

The same basic rules apply. Your refinance must result in a lower interest rate, or you must switch from an ARM to a fixed-rate mortgage, and no cash out is permitted.

The VA does not require an appraisal or a credit underwriting package, and you have the option of rolling the refinance costs into the new loan or opting for a no cost refinance.

Additionally, a Certificate of Eligibility from the VA is not required, making it a snap compared to the usual tedious refinance process.

HIRO Streamline Refinance (Fannie Mae and Freddie Mac)

- There is also a streamline solution for conventional loans

- Specifically for borrowers with Fannie Mae- and Freddie Mac-backed loans

- It’s known as a HIRO refinance (short for high-LTV refinance)

- Like the other programs there are many rules that must be met to qualify, but the process is simplified

You may have also heard of HARP and HARP 2.0, a streamlined loan program that allowed underwater homeowners to refinance their mortgages, no matter how high their loan-to-value ratio (LTV) was.

This was a popular option several years ago, but has since been replaced with permanent solutions known as a High LTV Refinance, or “HIRO” for short (also known as a Freddie Mac Enhanced Relief Refinance).

The same basic qualification requirements (or lack thereof) apply here, though your loan must be owned by Fannie Mae or Freddie Mac, and the note date must be on or after October 1st, 2017.

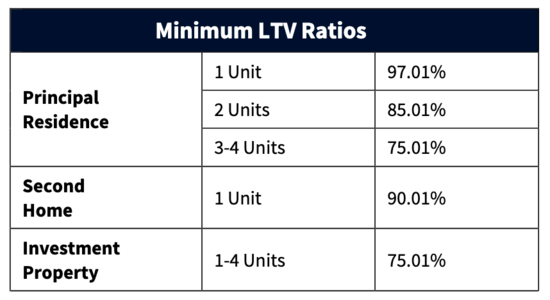

Additionally, your current LTV must be quite high in order to qualify, though it varies by occupancy and property type (see chart below).

Additionally, the borrower must benefit in at least one way, whether it’s a reduced monthly payment, lower mortgage rate, shorter amortization period, or a more stable loan product (e.g. ARM to FRM).

At least 15 months must have passed between the note date of the loan being refinanced and the HIRO mortgage.

Finally, you must be current on your mortgage at the time of refinance, with no 30-day late payments in the past six months and no more than one late payment in the preceding 12 months (and none greater than 30 days).

Assuming you qualify, you should be able to get your hands on a much lower mortgage rate, even with an excessively high LTV, all with limited fees and closing costs.

Borrowers are able to use the HIRO refinance option multiple times assuming all other requirements are met, including the loan seasoning mentioned above.

Is Streamlining Your Refinance the Best Deal?

- Sometimes the easiest option isn’t the cheapest one

- So make sure the streamline refinance is actually the best deal

- It should have the lowest interest rate and closing costs

- Relative to other mortgage programs you may qualify for

While a streamline refinance may be your easiest option, and a money-saving one at that, it may not be the best choice for you.

Whenever you’re in the market for a refinance, it’s wise to take the time to shop around, even if you’ve been approached about one of these programs.

That means looking beyond your current lender and/or loan type to see if there’s something better out there.

Be proactive and reach out to lenders, as opposed to simply taking whatever falls into your lap. Don’t be a desperate homeowner.

For example, it might be better to have a conventional loan instead of an FHA loan, even if that means going through the whole underwriting process as opposed to a streamline.

You may find a lower mortgage rate with a new lender that will justify a more involved qualification process. And it may not even require much more work or time to go about it the traditional way.

Sure, it can be a pain to refinance your mortgage, but the savings afforded each month and over your lifetime should definitely be worth your time.

It’s hard to find a better return on investment for the small amount of time put in considering you could be saving money for the next 360 months.

Read more: When to refinance your mortgage.

- UWM Launches Borrower-Paid Temporary Buydown for Refinances - July 17, 2025

- Firing Jerome Powell Won’t Benefit Mortgage Rates - July 16, 2025

- Here’s How Your Mortgage Payment Can Go Up Even If It’s Not an ARM - July 15, 2025