If you’re new to real estate and preparing to make an offer on a property, you might be wondering what mortgage is best for a first-time home buyer.

This is especially important now that mortgage rates have essentially doubled, putting budgets front and center.

It also means the popular 30-year fixed is no longer the default option for home buyers, with cheaper adjustable-rate mortgages now a consideration.

While both seasoned homeowners and first-time buyers may wind up with the same exact home loan, there are additional options to consider if you’ve never bought a home before.

Let’s explore the many loan choices available today to determine what might be best in the current environment.

Home Loan Types to Consider If You’re a First-Time Buyer

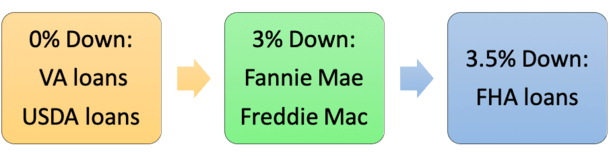

- Fannie Mae HomeReady (3% down payment)

- Freddie Mac Home Possible (3% down payment)

- FHA loans (3.5% down payment)

- VA loans (0% down payment for vets/active duty)

- USDA loans (0% down payment for rural home buyers)

- State Housing Finance Agency loans (down payment assistance and help with closing costs)

- Also look for local and national grants for first-time home buyers and Mortgage Credit Certificates (MCCs)

I’ve listed the most common loan types available to first-time home buyers, many of which are also an option for existing homeowners.

These generally don’t require much in terms of down payment, which seems to be a chief need/want for first-time buyers that don’t have the equity of move-up buyers.

Personally, I prefer to put down 20% on a home purchase to avoid costly mortgage insurance and to obtain a lower mortgage rate, but I understand that isn’t always realistic.

If a veteran/active duty, there are VA loans that require 0% down payment and come with lower mortgage rates relative to other loan types.

If buying in a rural area, USDA loans also allow 0% down payment and competitive mortgage rates.

There are fewer restrictions on FHA loans, which require a 3% down payment but allow credit scores as low as 580.

In addition, conforming loans backed by Fannie Mae and Freddie Mac only require a 3% down payment.

Note that for Fannie/Freddie loans, you can get your loan-level price adjustments (LLPAs) waived if you’re a first-time home buyer with qualifying income ≤100% area median income (AMI) or 120% AMI in high-cost areas.

Or if the loan is HomeReady/Home Possible, meets Duty to Serve requirements, is in a high needs rural region, a loan to a Native American on tribal land, or a loan originated by a “small financial institution.”

So for those lacking assets, the programs listed above are probably a good starting point, especially if you qualify for LLPA waivers.

Is Your First Home a Starter Home or a Forever Home?

- Always think about how long you’ll stay in the property you’re buying

- It might be possible to save money by choosing an ARM if you plan on moving soon

- Many first-time buyers move-up to larger properties within a few short years

- Your expected tenure is also a key consideration with regard to paying points

Once you choose a loan type, you can decide on a specific loan program, such as a 30-year fixed, 15-year fixed, or an ARM.

While most first-time buyers will ultimately go with a 30-year fixed, let’s discuss how the property itself could dictate your financing decision.

The first thing I’d consider when buying a first home would be how long you plan to keep it. A lot of folks buy what are known as “starter homes” initially, then move up to larger homes within a few years.

For example, if you just got married and want to buy a home next, you might also be thinking about starting a family shortly after that.

This often results in outgrowing that first home, and requiring a new, larger property. Depending on your timeline, this could all happen within just a few years.

In that case, it could make sense to go with a hybrid adjustable-rate mortgage (ARM) such as the 5/1 ARM or 7/1 ARM.

While fixed mortgage rates aren’t much more expensive than ARMs at the moment, this isn’t always the case. Sometimes it’s significantly cheaper to go with an ARM.

And these hybrid ARMs offer a fixed-rate period for the first five or seven years before you even have to worry about an interest rate adjustment.

In other words, it operates exactly like a 30-year fixed-rate mortgage up until its first adjustment – by then you could have already sold and moved on to a new property.

Tip: It might be easier to skip the starter home because entry-level homes tend to be the most in demand. You could even avoid having to move a second time!

Be Mindful About Paying Points Upfront

Another consideration is whether or not to pay mortgage points – again, how long you plan on staying has a lot to do with it.

These points are a form of prepaid interest that lower the interest rate you receive on your loan. In short, you pay today (at loan closing) for a discount while you hold the loan.

For example, you might pay one point for a 0.375% discount in rate for the next 30 years.

However, there’s no point (no pun intended) in paying points on a mortgage you’ll only keep for a few years. Often it takes many years to break-even on discount points paid.

Even if you stay in the home, you may refinance your mortgage sooner rather than later, making points a losing proposition.

Consider the current mortgage rate environment, and where interest rates could be headed after you buy.

The exception to this might be a temporary buydown, especially if it’s paid for by the lender or seller, since you get the full value in the first couple years. Or potentially a refund if you refinance/sell early.

You Don’t Want to Be House Poor

- You may experience payment shock or become house poor when buying your first home

- This means going from paying a relatively small amount to a large amount monthly

- Also consider the other bills you’ll need to pay like homeowners insurance and property taxes

- Don’t look at the mortgage like a bad debt, it’s often the cheapest debt you’ll have the joy of repaying

It may be tempting to go with a shorter-term mortgage such as the 15-year fixed, seeing that it can cut your interest expense significantly. But it will also nearly double your monthly payment.

One thing mortgage lenders consider when extending home loans to first-time buyers is payment shock.

Simply put, if you go from paying $1,000 per month in rent to $3,000 on a mortgage, they may worry that you’ll have a tough time adjusting to the higher payments.

And they have good reason to worry because it’s all supported by data.

Even if you are approved for a shorter-term mortgage, it might be better to take things slow instead of going all-in on the mortgage.

Sure, it’s great to pay off a large debt quickly, but a mortgage can be a good debt, and is often the cheapest debt you’ll have.

Despite the 30-year fixed coming in closer to 6.5% or higher today, it’s still relatively cheap compared to other debt like credit cards and so on.

And, it’s always possible to make extra mortgage payments if you want to pay your mortgage off early, regardless of which loan program you choose.

So you can get the flexibility of a 30-year loan with the option to prepay it like a 15-year loan if you so choose.

Check Out Home Loan Programs Exclusively for First-Time Buyers

- Visit your state’s housing finance agency to see what special programs they offer

- It might be possible to get a mortgage with nothing down if you don’t have much money saved up

- Also search for first-time home buyer grants and Mortgage Credit Certificates that may be available to you

- Compare both traditional and first-time buyer loan programs to determine best option

While it’s possible to apply for any home loan out there, certain loan programs are reserved only for first-time home buyers.

These are meant to be more accommodating to those who may have trouble qualifying, often due to down payment.

If you check out your state’s housing finance agency (HFA) for homebuyer assistance, you should see loan programs geared specifically toward first-time buyers.

This can include down payment assistance, closing cost assistance, or both, handy if you haven’t saved much prior to purchase.

One recent example is the Dream For All Shared Appreciation Loan, which doesn’t require a down payment but works as if you put 20% down.

Note: These housing agencies are not lenders, so you’ll need to research them then use their “find a loan officer” section to see which lenders offer their products.

You can also do this in reverse if you’re already working with a lender. Ask what HFA programs they offer to first-time home buyers.

It may also be possible to get a first-time home buyer grant with a large bank, local credit union, or direct mortgage lender.

Be sure to search for local grants because they’re often forgivable, meaning it doesn’t need to be paid back!

One example is the U.S. Bank Access Home Loan, which offers up to $12,500 in down payment assistance and a lender credit up to $5,000.

The one caveat to some of these loan programs is that you might need to complete a homeownership class, though it can be beneficial and is typically pretty basic and not all that time consuming.

Another perk first-time buyers might be able to take advantage of is a Mortgage Credit Certificate (MCC), which can reduce your tax liability, thereby saving you money indirectly on your mortgage.

It may also allow you to qualify for a larger loan amount in some cases.

Lastly, look beyond loan programs for first-timers. You may not need any special loan program, and it could actually be cheaper to stick to a traditional one instead.

Who Are the Best Mortgage Lenders for First-Time Buyers?

I don’t know of one bank or lender that specializes in financing for first-time home buyers, though there are companies that only cater to home buyers, such as Tomo.

And with mortgage rates significantly higher today, most lenders are pivoting to be home buying specialists anyway.

Look out for special offers and incentives as the mortgage market becomes largely purchase-driven.

Ultimately, you’ll probably find a lot of the same loan programs no matter where you look, barring some of the unique offerings discussed in the prior section related to grants and state housing agencies.

This means you’ll be able to get an FHA loan, USDA loan, or VA loan from most banks/lenders out there. The only difference might be the mortgage rates and/or lender fees.

You should also be able to obtain a Fannie Mae HomeReady or Freddie Mac Home Possible loan from just about any lender.

As noted, both require just three percent down when purchasing a home and come with other potential pricing discounts.

Consider a Mortgage Broker If You’re a First-Time Home Buyer

Instead of focusing on a single lender, it might be better to get in touch with an experienced mortgage broker, especially if you’re a first-time buyer.

These individuals can guide you through the loan process and compare rates and programs from dozens of lenders at once.

Or structure your loan to save on mortgage insurance and/or mortgage rate with specific down payments.

They can be helpful if you have lots of mortgage questions, which is often the case for someone purchasing their very first home.

You might not get the same level of service with a large bank or call-center lender.

Alternatively, you can reach out to a HUD-approved housing counselor if you need one-on-one assistance or are uncertain of where to turn for financing.

An experienced real estate agent may also be helpful, as many of them are pretty well-versed in mortgages.

Just be sure to due your own diligence and look beyond their own recommendations. You don’t have to use their “person.”

Ultimately, educating yourself on mortgages before reaching out to others might be the best way to start your home buying journey. Being knowledgeable means being financially empowered.

Perhaps the “best mortgage” for a first-time home buyer is simply one they fully understand.

Read more: What is a good price for a first-time home buyer?

- Do Mortgage Rates Need a Hike to Move Lower? - July 28, 2026

- How Mortgage Rates Avoid a Return to 7% - July 24, 2026

- Mortgage Rates Hit New 52-Week High - July 23, 2026