Over the next few months, the FHA will make a number of substantial revisions to its annual mortgage insurance premium structure.

This is in addition to the FHA’s increase in upfront mortgage insurance premium, which came last year.

In short, the changes will cost new FHA borrowers more money going forward as a means to bolster capital for the agency’s ailing reserve fund.

Essentially, future borrowers will pay for the missteps of past homeowners, though the FHA was the one that allowed such loose lending (downpayment assistance loans) to persist.

The blame game aside, let’s take a look at the important changes coming soon to an FHA loan near you:

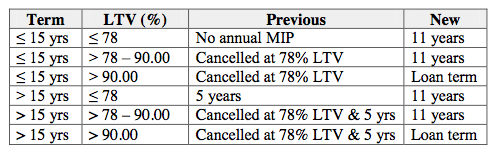

Mortgage Insurance No Longer Canceled at 78% LTV

- A rule that went into effect in 2001

- Canceled the annual MIP on FHA loans at 78% LTV

- Based on the original amortization of the home loan

- Meaning homeowners only had to pay it for a fraction of the loan term

Perhaps the biggest change is the automatic removal of annual mortgage insurance premiums once an FHA loan falls to a certain loan-to-value ratio (LTV).

This rule, which came into effect in 2001, canceled MIP payments once the loan reached 78% of the lower of the sales price or original appraised value, based on the original amortization schedule.

It was also possible to make extra principal payments to get to that magical level, though using a new appraisal to lower the LTV is not an option.

In other words, if you want to remove MIP on an older FHA loan, you can’t do so simply by getting an appraisal, even if your home price has skyrocketed. You’ll have to refinance to a conventional loan instead.

*Also note that for 30-year loan terms, the annual MIP had to be paid for a minimum of five years, regardless of LTV.

However, the FHA realized it was still insuring these loans against default long after borrowers stopped making insurance payments, therefore costing the agency billions in foregone revenue.

Below is a chart that details the new annual mortgage insurance premium structure, depending on your LTV and loan term (15 year vs. 30 year).

The typical borrower who puts down less than 10% and opts for a 30-year fixed mortgage will be stuck paying annual MIP payments for the life of the loan.

Certain less risky borrowers will only be subject to annual MIP payments for 11 years, though that compares to previous rules that didn’t require any annual MIP.

These changes apply to loans with FHA case numbers assigned on or after June 3, 2013. So if you’re shopping for a home, get on it!

Higher Annual MIP for FHA Loans

- This is actually a one-two punch for FHA borrowers

- Because the annual MIP was also increased

- So borrowers will pay more for a longer period of time

- Which will probably lead most to refinance out of the program earlier

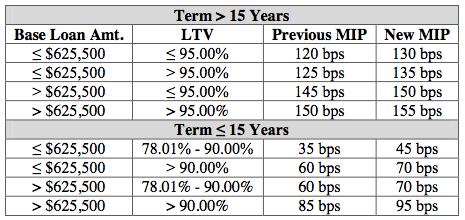

On top of these changes, the FHA will also raise the annual MIP for most new mortgages by ten basis points, or .10%.

This change isn’t as significant, though it will still hit new borrowers’ wallets.

If we look at the second line in the box above, the current 125 basis point annual MIP costs a borrower with a $100,000 loan $1,250 a year.

The change will increase that cost to $1,350 a year. It’s essentially another $100 for every $100,000 financed, which equates to several dollars a month in extra mortgage payment.

For loan amounts over $625,500, the annual MIP increase will only increase five basis points (0.05%), which is the maximum authorized annual MIP.

These changes also apply to new loans with case numbers assigned on or after April 1, 2013.

Note: This change does not apply to streamline refinances of existing FHA loans that were endorsed on or before May 31, 2009.

Low Risk FHA Loans No Longer Exempt

- FHA borrowers who went with 15-year fixed mortgages

- And had LTVs of 78% or less

- Didn’t have to pay annual mortgage insurance premiums previously

- But they will be on the hook for a 0.45% annual MIP going forward

While the FHA has traditionally served the low-down payment market, there are those who have taken advantage of the low mortgage rates and lack of an annual MIP.

For example, those who elected to take out 15-year fixed mortgages with LTV ratios equal to or less than 78% didn’t have to pay an annual MIP on an FHA loan in the past.

But come June 3, the new annual MIP for such loans will be 45 basis points, making these types of borrowers think twice about the FHA.

[FHA loans vs. conventional loans]

What Else Is in Store?

- The FHA also wanted to raise the minimum down payment

- On jumbo conforming loans insured by the agency

- From 3.5% to 5%

- But this never actually materialized

Also note that the FHA has proposed raising the down payment requirement for so-called “jumbo conforming loans” that exceed $625,500.

The minimum down payment will be bumped from 3.5% to 5%, assuming it becomes a new guideline.

Additionally, the FHA will require lenders to manually underwrite loans where borrowers exhibit layered risk.

Specifically, those with credit scores below 620 and debt-to-income ratios above 43% will have to document compensating factors to support positive underwriting decisions.

This change is effective for case numbers on or after April 1, 2013 as well.

These revisions should continue to affect the FHA’s market share of new mortgages, which surged in recent years as subprime lenders went the way of the dodo.

However, the latest loan origination report from Ellie Mae revealed that FHA loans accounted for just 18% of new loans in January, down from 24% six months earlier.

Fannie Mae and Freddie Mac are also expected to raise g-fees to make the mortgage industry less reliant on the government.

So slowly but surely, more private capital will make its way back into the mortgage market. At least, that’s the plan…

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

- Mortgage Rates Are Now Higher Than They Were a Year Ago - August 5, 2026

- Chase Is Advertising Mortgage Rates With Nearly Two Discount Points to Keep Them Looking Attractive - August 4, 2026