Today we’ll check out another one of the newcomers in the mortgage industry that is all about technology and low rates, aptly named “Lower Mortgage.”

Similar to Better Mortgage, which is also a one-word-named mortgage company, they like to keep things simple and make it easy to apply for a home loan.

That means you can get started right on their website, or even begin your home loan process with a text message.

They’re also all about things being lower, whether it’s mortgage rates, lender fees, monthly payments, or the amount of hassle it takes to get a mortgage.

They even take a subtle jab at Quicken Loans on their website, saying “No rocketry. Just the important stuff—like lower rates.”

Let’s find out more about this low-loving, techy mortgage lender.

Lower Mortgage Quick Facts

- Direct-to-consumer mortgage lender that offers home purchase loans and refinances

- Launched in 2018, headquartered in New Albany, Ohio (just outside Columbus)

- Originated roughly $5 billion in home loans last year

- Licensed in 45 states and the District of Columbia

- A top-rated lender on LendingTree that has won several customer satisfaction awards

- They have a sister company called Homeside Financial (founded in 2013)

- Exclusive mortgage provider for Opendoor

- Acquired real estate portal Movoto in May 2025

- Partnered with real estate brokerage HomeSmart in October 2025

Lower, which actually refers to itself as a technology company, was launched in December 2018.

The main goal of the company is to improve the online mortgage and refinance experience, knowing that the majority of applicants start the process on the Internet.

In a sense, they’re kind of like Rocket Mortgage, which is the tech platform backed by parent company Quicken Loans.

Anyway, Lower is located in New Albany, Ohio, which is just outside Columbus and has been around since the end of 2018.

They’re currently licensed to do business in 45 states and the District of Columbia.

They don’t do business in Alaska, Hawaii, New York, Rhode Island, or Vermont.

In 2024, their parent company funded nearly $5.3 billion in home loans, with about 83% for home purchases and the remainder refis.

While they’re available in most states, the most volume came from Colorado, Florida, Illinois, North Carolina, Texas, and their home state of Ohio.

It should be noted that Lower Mortgage also has a sister company called Homeside Financial, which was founded back in 2013 by current Lower CEO Dan Snyder.

In November 2023, Lower acquired Denver-based Universal Lending. It includes both the retail division and wholesale channel, which will operate under the company’s PowerTPO brand.

And in December 2023, the company announced a merger with Thrive Mortgage, which will apparently double their national footprint.

In May 2025, Lower announced plans to acquire real estate portal Movoto, a move aimed at gaining high-intent web traffic from prospective home buyers.

And in October 2025, they partnered with real estate brokerage HomeSmart and their 25,000 agents via a national marketing agreement.

Applying for a Mortgage at Lower

- You can apply for a home loan directly from their website without assistance

- They utilize a loan recommendation engine that relies upon artificial intelligence (AI)

- It’s also possible to text or call them to get started on your application if you need help

- Lower offers a digital mortgage process with document uploading, eSign technology, and more

Lower is definitely a new-age mortgage lender that relies heavily on tech. And a certain cool factor that differentiates them from the older, stale banks and lenders.

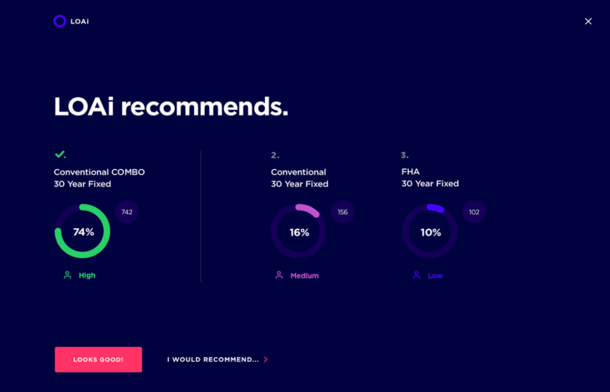

Aside from having a snazzy looking website, they also have a virtual loan assistant known as LOAi. It uses artificial intelligence to help you pick the best home loan for your unique situation.

Data is analyzed from thousands of closed loans and other peer data points to deliver a personal home loan recommendation in real-time.

In terms of applying for a home loan, you can do so right on their website by clicking “Apply Now.”

You actually get three options, including a “Jump Start,” “Quick Apply,” and a simple text to get the ball rolling. Clearly, they are a mortgage lender geared toward Millennials and Gen Z.

Use a Human or Navigate Lower.com on your Own

It’s also possible to just call them up if you’d like to speak to a human (they’re open Monday through Saturday).

If you choose the Jump Start option, it’s probably just a short contact form. This means a loan officer will get in touch after completion.

The Quick Apply Option appears to be sort of like a quick mortgage pre-qualification sans hard credit pull to start the actual loan process.

My assumption is you can complete mostly everything online or via smartphone since they’re a so-called “techy” mortgage lender.

This may include linking financial accounts, scanning and uploading paperwork, and eSigning documents along the way.

But humans are also available if and when you need them to discuss loan options, loan rates, or to answer any other mortgage questions you may have.

All in all, they pride themselves on making it quick and easy to get a mortgage, and all operations are conducted under one roof at Lower HQ.

Loan Types Offered by Lower

- Home purchase loans

- Refinance loans (rate and term and cash out)

- Conventional loans backed by Fannie Mae and Freddie Mac

- Government-backed loans including FHA loans, USDA loans, VA loans

- Jumbo home loans

- Home equity lines of credit (HELOCs)

- Fixed-rate and adjustable-rate mortgage options available

Lower appears to keep things pretty simple, though they should have loan programs to suit most borrowers.

It is my understanding that you can get financing on all property types, including primary residences, vacation homes, and investment properties, including condos/townhomes.

You can get both a home purchase loan or a refinance, including a cash out refinance. They say you can access up to 95% of your home’s equity, which may separate them from other lenders.

This might be accomplished via a combo loan, utilizing a home equity line of credit (HELOC) and a first mortgage.

In any case, if you want to tap into your home equity, Lower might be a good option. But they also make it easy for those purchasing a home as well.

If they’re anything like their parent company Homeside Financial, you should be able to get a conforming loan, jumbo loan, or a government-backed loan such as a FHA loan or VA loan.

Both fixed-rate and adjustable-rate options are available, including 30/15 fixed mortgages and hybrid ARMs like the popular 5/1 ARM.

Lower’s Free Refi for Life Deal

For a limited time (unclear how long exactly), if you use Lower.com to buy a home or refinance, you won’t have to pay lending fees on future refinances, for life.

If you do refinance with Lower again, they’ll waive any Lower retained fees. This includes an applicable loan origination fee, underwriting fee, processing fee, or administrative fees.

However, it does not apply to any discount points or any third-party settlement service fees such as title insurance, home appraisal fee, or credit report fee.

You must have closed the previous refinance transaction with Lower at least six months prior to any subsequent application

Lower.com Mortgage Rates

With a name like Lower, you better publicize your mortgage rates, right?

Well, they do, right on their homepage, albeit just one rate, a 30-year fixed, which they refer to as “Today’s Lower Rate.”

While the rate appeared to be really low, they did disclose that it required 2.25 discount points, which can be pretty expensive.

For example, on a $300,000 loan amount, that’s $6,750 in closing costs, not to mention any other fees that must be paid.

They also list three competitors, which at the time of this writing, included Quicken Loans, Wells Fargo, and the Bankrate average.

As you might suspect, they beat all three handily, both on interest rate and mortgage APR, the latter of which factors in lender fees.

Speaking of, they actually have a page dedicated to lender fees on their website, but it only lists possible fees you might be charged, sans any actual dollar amounts.

This makes it a bit unclear as to what they charge and how much it might set you back.

Remember to look beyond mortgage rate alone, and really dig into the closing costs when comparing Lower to other mortgage lenders to ensure you get the best deal.

Lower Is the Exclusive Mortgage Provider for Opendoor

In early 2023, Lower became the exclusive mortgage fulfillment provider for Opendoor.

Opendoor is an iBuyer that helps home buyers an sellers. In order to focus on that business, they are outsourcing their mortgage services to Lower.

So if you work with Opendoor, there’s a good chance they’ll refer you to Lower for mortgage financing.

However, Opendoor customers are allowed to use any licensed mortgage lender.

Lower refers to it as a “Mortgage as a Service” (MaaS) platform. Simply put, companies can offer mortgage products to their customers via Lower.

Lower Mortgage Reviews

On LendingTree, they’ve got a 4.9-star rating out of 5 based on more than 2,100 customer reviews, along with a 99% recommendation rate.

They also have seven accolades from LT, including a top-10 for home lending customer satisfaction for Q1, Q2, and Q3 of 2020, along with Q4 of 2019, and similar awards for home equity lending.

On Zillow, they have a 4.92-star rating out of 5 on nearly 3,000 reviews, many of which say the interest rate was lower than expected. I sure hope so with a name like that…

Their parent company Homeside Financial is not Better Business Bureau accredited, but does enjoy an ‘A+’ rating at the moment based on customer complaint history.

In summary, Lower Mortgage is probably a good pick for someone who wants a low mortgage rate with limited fees that is comfortable applying for a home loan without much help (though it is available).

Lower Mortgage Pros and Cons

The Good

- Offer a tech-enabled digital mortgage process

- Can apply for a home loan directly from their website or via smartphone

- They apparently have low mortgage rates and low lender fees

- May be able to access more money because they offer HELOCs

- Don’t charge lender fees on subsequent refinance transactions for life

- Excellent customer reviews

- A+ BBB rating

- Free mortgage calculators and other tools on site

The Maybe Not

- Not licensed in all states (Alaska, Hawaii, New York, Rhode Island, or Vermont)

- Do not list their lender fees

- Would be nice to see more information regarding their mortgage rates

- No brick-and-mortar locations

(photo: Marcin Wichary)

- Mortgage Rates Catch a Break as Job Growth Goes Negative - August 7, 2026

- Mortgage Rates Move Higher on Jobs Report Defense - August 6, 2026

- Mortgage Rates Are Now Higher Than They Were a Year Ago - August 5, 2026

My experience with Lower.com has been less than stellar. As someone with really good credit, I thought doing a refinance with them would be quick and painless, boy was I wrong. They have a decent sales person, contact you and promise you the sun and the moon, but then unfortunately they fail to deliver. My guess is their customer base grew too quick for their limited resources to handle. Here are some of the issues so far:

• The Loan estimate I got had no points listed, yet when I got the first CD they had tacked on ~$2K of points on top of their origination fee.

• We had discussed and the Loan Estimate showed no Escrow Account, yet the CD has added an escrow account, and to waive it they are asking for an additional $400.

• Before even closing the loan, they got themselves listed as a “Second Mortgage” on my Home Insurance. WTF?

• They are seriously dragging their feet on the backend, they were already at fault for expiring the first 45 day lock, we are going through extensions of that now, when my previous refi with Provident took 10 days from application to closing. I am still waiting for them, going on 2 months! (Jan 7 – March 2)

• Not to mention their incompetent Leads team, I have been getting 3-4 calls per week from their Leads team trying to get me to do a refi with them, I have had multiple conversations with them explaining that I am already in the process with them, and each and every time they promise they’ll fix their database, only to call me again a few days later as a new lead.

• Lastly, I just got notified that someone attempted to file taxes with the IRS who was not me, and the only company I have given enough info to do that has been Lower.com Coincidence? I hope so….

I still don’t know if this loan refi will even happen, I really wish I would have used my current lender (Provident) to do my refinance.

I began my refi with Lower on January 11, 2021 with a 60 day rate lock. As of this date, March 24, nothing has happened. I have been told that extension cost will be covered by lower but at this point I find it hard to believe. The only reason I have been so patient is the rate of 2.625 was lower than I could find anywhere for a loan of only $160k. After reading the comment from Alex, I’m wondering if I too will suddenly see points added later in the closing or some other cost not disclosed in my loan estimate. :(

I am a current customer that has been trying to close since October of last year. Excuse after excuse after excuse, little to know updates, no progress, delay after delay, lie after lie. Days turn into weeks, weeks turn into months… I get a call last week saying “We’re ready to finally close”. Nope, that just means we will show up at your house with a notary and try and get you to sign all the documents quick without giving you time to review. I said “I need at least 48 hours to review the documents before the notary arrives”…. Oh yes no problem at all…. well excuse after excuse lie after lie still no mortgage documents for me to review, they’re full of it, and I’ve had enough… I’m out. Now I’m out my appraisal fee, lost a great interest rate, and lost 7 months of wasted time. I told them two days ago I’m out of the deal and I need a formal letter of withdrawal stating I’m not working with them anymore, I’ve left 3 voicemails, color me surprised, but they now won’t return my calls. I don’t understand what it is they are trying to accomplish but seriously save yourself the aggravation and go to someone else. I’ve also brought referrals to them, all of them also have had similar experiences and are done.

My experience with Lower mortgage was extremely disappointing. At first I was reassured by the good reports on lending tree and Zillow but now I wonder if those are actually based on customer reviews or their company’s opinion (which may have been influenced by a financial relationship with Lower). I worked with Damien Conglose who was nice over the phone and reassured me that we could explore all options including conventional, FHA, and USDA to find what’s best for me. I sent him the requested info and he really pushed me to go for conventional. I said I’d consider it but asked to please send over what the offers would be for FHA and USDA as well so I could compare. He stopped responding. I called and emailed still with no answer. Weeks went by during which several good house options for me were sold that I would’ve loved to put offers on. His unresponsiveness caused my family to miss out on housing opportunities and he didn’t even bother to let me know we wouldn’t be getting any offers from Lower. Thankfully I moved onto other lenders but even now it’s been over a month with no answer from Damian or anyone at Lower. If you want a conventional loan they may be able to help you but don’t ask for anything else or they may just cut you off completely. As a buyer you should be able to explore multiple loan options to find what’s best for you, so for this reason AVOID Lower!

My experience with Lower.com has been disappointing. I ended up with Lower after finding out Navy Federal would not be able to close in the timeframe necessary so I reached out to Lower.com and was sold on mortgage brokers claim they could close in 21 days which was even earlier than original close date which was ideal. Turns out that was a lie. I have all the necessary documents on hand and it still supposedly sat in underwriting for over a month. Then finally got the loan contingencies which I fulfilled but still waiting on final documents to sign. I wish I had gone with Rocket.

Lower.com is proving to be bad news for me also as a home loan co-signer for my granddaughter. The number used to call me is labeled spam risk. Looking that up confirms it is a home number to someone else? Does not add up. I was also offered a call back, never got one until the next day. My research also showed the agent does not have a land line? My granddaughter was finally told she did not qualify on her own after working with the agent for over 2 weeks? He did not record her income correctly? Very fishy. Still working on this but the deadline is 6/24 so unlikely it will process on time. Hope to provide an update here by then. Right now, I say STAY AWAY FROM LOWER.COM.

Lower Mortgage has a terrible response time and zero communication. Buyers are using them to finance and they can’t even get an appraisal ordered. Both brokers, the buyers and myself as the seller have emailed Lower Mortgage and have not had a response to an appraisal date in three weeks. The buyers expiration date on the contract is ready to end and I will list my home again and keep the earnest money for damages. Terrible company.

From the comments above, I’m seeing a pattern emerge. I just asked them for a HELOC quote and was told that “Underwriting wouldn’t approve it without holding your first mortgage.” They then proceeded to give me a first mortgage quote that I didn’t ask for with a rate HIGHER than my current mortgage! Needless to say, I cut them loose and asked not to be called again. This does not seem like a trustworthy business to me!

Funny, this article was written the day I committed to getting a loan from Lower. I was relying on their great reviews on Zillow but now am suspect because the review I submitted to Zillow hasn’t posted (no vulgarity, or specific names that might have gotten it blocked) and in looking for it, saw this article. The experiences you all have listed were pretty similar. They cancelled the fourth attempt to close and we walked, nearly 6 months after we started. Aside from the loan officer, who was very kind and also dismayed at the process, the communication was poor and often confusing.

I think they are overwhelmed by business and customers get lost in the cracks. The short of it is, we signed our initial paperwork on March 2, 2021 and by March 10th had our appraisal and all our paperwork completed. After at least four “Closing Disclosures” signed throughout June, July and August, I told our LO on August 9th that the final date that we could close before we were to end our business with Lower would be on Sunday August 22. After they cancelled the closing on August 18th we moved on.

I worked with Patrick Szymczak and he was excellent. He guided me through the process and made it as easy as possible. Patrick kept me posted along the way and told me step by step what document to upload and what document had to be signed. I received a very good rate and was surprised how simple the process was. I accomplished the entire refinancing via email except for the final loan closing even that was a piece of cake. I recommend Patrick to everyone I know that is considering a refinance. Thank you, Patrick and Lower.com!