It’s time for another edition of mortgage match-ups: “FHA vs. conventional loan.”

Our latest bout pits FHA loans against conventional loans, both of which are extremely popular loan options for home buyers these days.

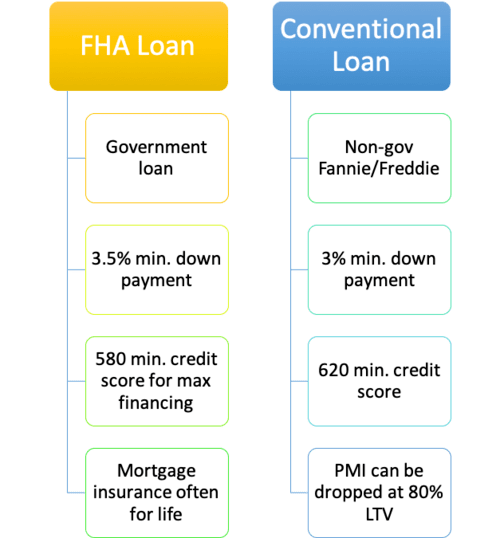

In short, conventional loans are non-government mortgages, typically backed by Fannie Mae or Freddie Mac.

Whereas FHA loans are government-backed mortgages that are insured by the Federal Housing Administration (FHA).

Both can be a good choice depending on your credit profile and homeownership goals, but there are key differences.

Let’s discuss the pros and cons of both loan programs to determine if and when one might be the better choice.

FHA and Conventional Loans Both Offer a Great Low Down Payment Option

- It’s possible to get an FHA loan with a 3.5% down payment and a 580 FICO score

- Or a conventional loan with just 3% down payment and a 620 FICO score

- FHA lending is more flexible in terms of credit score but requires a little bit more down

- Be sure to consider the cost of mortgage insurance when comparing the two loan programs

First off, whether you go FHA or conventional, know that the down payment requirement is minimal.

You need just 3.5% down for FHA loans and only 3% for conventional. So you don’t need much in your bank account to get approved for either type of loan.

The main selling point of an FHA loan is the 3.5% minimum down payment requirement coupled with a low credit score requirement. That’s a one-two punch.

However, in order to qualify for the government loan program’s flagship low down payment option, you need a minimum credit score of 580.

A FICO score below 580 requires a 10% down payment for FHA loans, which most home buyers don’t have.

And 580 is just the FHA’s guideline – individual banks and mortgage lenders still need to agree to offer such loans. So there’s a very good chance you’ll need an even higher credit score with many lenders.

Meanwhile, Fannie Mae and Freddie Mac require a minimum 620 FICO score and just 3% down (instead of the 5% down they used to require), which is even better.

This means the FHA is no longer winning in the down payment category if you ignore credit score. Both FHA and conventional loans can be had for very little down!

However, the FHA vs. conventional loan battle doesn’t end there. We need to consider other factors, such as mortgage rates and mortgage insurance.

FHA Loans Are Generally Better for Those with Poor Credit

- There’s not one clear winner across all loan scenarios

- Determining the cheaper option will depend largely on your credit score and LTV

- FHA loans tend to benefit those with low credit scores and high LTVs

- Conventional loans are often cheaper for those with better credit scores and larger down payments

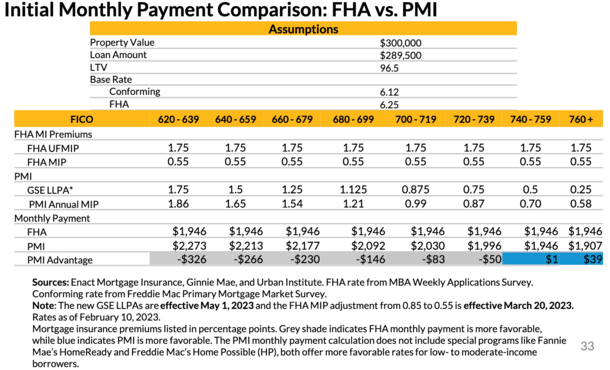

The screenshot above from the Urban Institute details when FHA wins out over conventional lending, and vice versa.

It takes into account the latest FHA premium cut (beginning March 20th, 2023), along with changes at the GSEs, including a new 780 FICO score bucket.

They show how each type of loan stacks up at 96.5% loan-to-value (LTV), while factoring in the borrower’s FICO score.

You can use this chart to quickly determine what credit score and down payment combination favors which type of loan.

Of course, you’ll need to plug in your actual numbers into a mortgage calculator to see what works for you because they make a lot of assumptions.

Note: Conventional loan pricing adjustments (LLPAs) are waived for HomeReady, Home Possible, first-home buyers with qualifying incomes (generally ≤100% area median income), and Duty to Serve loans.

If any of these situations apply to you (be sure to ask your broker/loan officer), it could make conventional loans much cheaper!

A Low Credit Score Combined with a Small Down Payment Strongly Favors the FHA

The PMI advantage row at the bottom of each chart shows when conventional or FHA financing is the better deal.

If PMI advantage is shaded grey, it means the FHA loan is the cheaper option.

We can see that FHA financing is remarkably cheaper for borrowers with credit scores between 620-679, assuming the down payment is 3.5%. And even about $150 less for scores between 680-699.

The FHA is a big winner if you’ve got just 3.5% down and a 620 FICO score.

Conversely, conventional loans begin to make a lot more sense financially when you have a 740+ FICO score, and even more sense with larger down payments. Those are shaded blue.

Conventional loans are cheaper if you have a 740+ FICO score, and potentially much cheaper with larger down payments.

But FHA loans can be a good option for those with bad credit and little set aside for down payment who are determined to get a mortgage.

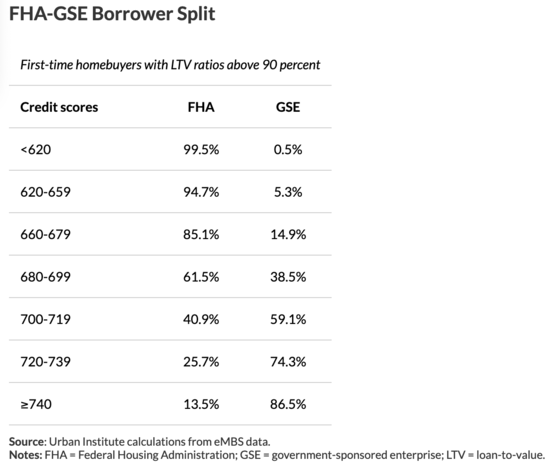

FHA vs. GSE Market Share by Credit Score

To give you an idea of the type of borrowers who go with one loan type versus the other, see the chart above.

Virtually all first-time home buyers with sub-620 FICO scores go with FHA loans (because Fannie/Freddie don’t accept sub-620 credit scores in most cases).

Meanwhile, a whopping 86.5% of borrowers with 740+ FICOs go with conventional loans.

It tends to be more of a mixed bag in the 680-719 FICO score buckets, where you might need to pay closer attention to rates, fees, and insurance premiums.

Long story short, low FICOs generally go FHA, while higher credit scores go conventional.

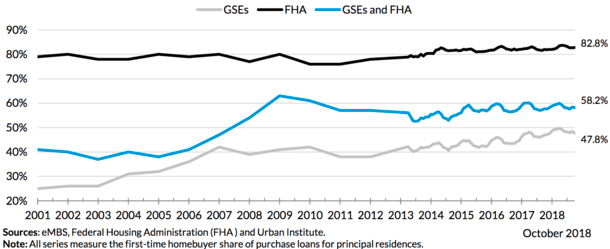

FHA Loans Are Hugely Popular with First-Time Buyers

Chances are if you’re a first-time home buyer, you’ll use an FHA loan over a conventional loan.

Just look at the chart above from the Urban Institute, which details the FTHB share of purchase mortgages by loan type.

As you can see, the FHA was dominated by FTHB with an 82.8% share in October 2018. Yes, nearly 83% of those who used an FHA loan for a home purchase were first-timers.

Meanwhile, only 47.8% share of purchase loans backed by the GSEs (Fannie Mae and Freddie Mac) went to first-timers.

The reason this might be the case is due to the low credit score requirement coupled with the low down payment requirement.

Since first-timers are often short on down payment funds (because they aren’t selling a prior residence and using the proceeds toward the new home), FHA tends to be a good fit.

FHA borrowers also generally have higher DTI ratios, higher LTVs, smaller loan amounts, and lower credit scores relative to GSE borrowers.

However, if you have student loans, which a lot of first-timers probably do, the FHA can treat them a bit more favorably when qualifying you for a mortgage.

Recently, they made a change where just 0.5% of the outstanding loan balance is used as the monthly payment for DTI purposes, down from the former 1%.

Meanwhile, Fannie Mae may calculate your DTI using 1% of the outstanding student loan balance, which could make qualifying for an FHA loan easier.

So if you have student loan debt, pay close attention to this rule, and/or check out the more flexible guidelines offered by Freddie Mac.

Are FHA Mortgage Rates Lower than Conventional?

- FHA mortgage rates are typically lower than conventional loan rates

- The spread can vary and not be much different depending on market conditions and the lender in question

- But you need to consider the entire housing payment beyond just principal and interest

- Once you factor in costly mortgage insurance premiums the math could change dramatically

When it comes to mortgage rates, FHA loans tend to come with slightly lower interest rates.

However, you must consider the entire payment (with mortgage insurance included) to determine what’s the better deal.

The boxes above actually assume an interest rate of 3.02% for an FHA loan and 2.81% for a similar conventional one.

To get actual/current rates, you’ll need to shop around to see what’s out there today.

It’s somewhat unusual since it’s usually the other way around, with interest rates on FHA loans lower.

However, this spread can vary over time (shrink or widen) and does depend on the mortgage lender in question.

Ultimately, there’s a good chance FHA mortgage rates will be lower than conventional ones, but pay attention to current rates on both products as you shop lenders.

I wouldn’t bank on FHA rates being higher, so if reality turns out to be different, it can certainly change the outcomes in the tables above.

FHA Loans Are Subject to Costly Mortgage Insurance

- Mortgage insurance is unavoidable on an FHA loan, which is the big downside

- And it will often remain in force for the entire loan term (as long as you keep your loan)

- Conventional loans allow you to drop MI at 80% LTV, which can be a huge advantage

- Fannie Mae and Freddie Mac also offer discounted mortgage insurance premiums for certain borrowers

We’ve talked about some benefits of FHA loans, but there are drawbacks as well.

The major one is the mortgage insurance requirement. Those who opt for FHA loans are subject to both upfront and annual mortgage insurance premiums, often for the life of the loan.

The upfront mortgage insurance requirement is unavoidable, and nearly doubled from 1% to 1.75% back in 2012. In addition, the annual premium can no longer be avoided.

Since 2013, many FHA loans now require mortgage insurance for life, making them a lot less attractive and expensive long-term! The never-ending FHA MIP could be the tipping point for some.

However, it’s possible to execute an FHA to conventional refinance to dump the MIP once you have the necessary home equity.

So it doesn’t really need to stay in-force for life. And many FHA borrowers do in fact refinance out or sell their homes before paying MIP long-term.

There’s No Mortgage Insurance Requirement on Conventional Loans

- If you come in with a 20%+ down payment or have 20% equity

- You won’t have to pay mortgage insurance with a conventional loan

- Some lenders may even waive the MI requirement regardless of the LTV

- They can do so by offering a slightly higher interest rate

Now let’s discuss some of the advantages of conventional loans, an alternative to FHA loans that tend to offer a lot more variety.

You won’t be subject to mortgage insurance premiums if you go with a conventional loan, assuming you put 20% down on a home purchase, or have at least 20% home equity when refinancing.

Even if you’re unable to put down 20%, there are low down payment loan programs that don’t require private mortgage insurance to be paid out of pocket.

In fact, the Fannie Mae HomeReady program only requires a three percent down payment with no minimum borrower contribution (and you can get up to a 3% credit for closing costs).

Additionally, there are select lender programs that offer 3% down with no MI, so in some cases you can put down even less than an FHA loan without being subject to that pesky mortgage insurance.

Of course, you can argue that the PMI is built into the interest rate when putting down less than 20%, even if it isn’t paid directly.

So you might get stuck with a higher interest rate if you make a small down payment and don’t have to pay PMI.

As noted, conventional mortgages require a down payment as low as three percent, so low down payment borrowers with good credit may want to consider conventional loans first.

Conventional Loans Offer Many More Options and Higher Loan Amounts

- You get access to many more loans programs when going the conventional route (fixed, ARMs, etc.)

- The loan limits can be significantly higher for both conforming and jumbo loans

- The minimum down payment requirement is also now lower!

- And you can get financing on more property types with fewer restrictions

With a conventional loan, which includes both conforming and non-conforming loans, you can get your hands on pretty much any home loan program out there.

We’re talking a 1-month ARM to a 30-year fixed, interest-only loans, and everything in between.

So if you want a 10-year fixed mortgage, or a 7-year ARM, a conventional loan will surely be the way to go.

Meanwhile, FHA loan offerings are pretty basic. They offer both purchase mortgages and refinance loans, including a streamlined refinance, but the loan choices are slim.

You’ll most likely be stuck with a 30-year or 15-year fixed, or maybe a 5/1 adjustable-rate mortgage.

If you’re looking for something a little different, the FHA probably isn’t for you.

Another benefit of going with a conforming loan vs. an FHA loan is the higher loan limit, which can be as high as $1,089,300 in certain parts of the nation.

This can be a real lifesaver for those living in high-cost regions of the country (or even expensive areas in a given metro).

With an FHA loan, you might be stuck with a maximum loan amount just above $472,000.

For example, it caps out at $530,150 in Phoenix, Arizona. That pretty much ends the discussion if you’re planning to buy even semi-expensive real estate there.

If you need to go above the FHA loan limit, it will either be considered a conforming loan or a jumbo loan, both of which are conventional loans.

For those who need a true jumbo loan, a conventional mortgage will be the only way to obtain financing.

You Can Get Conventional Loans Anywhere

- All banks and mortgage lenders offer conventional loans

- Whereas only certain lenders/banks originate FHA loans

- Additionally, not all condo complexes are approved for FHA financing

- And you can’t get an FHA loan on second homes or non-owner occupied properties

Another plus to conventional mortgages is that they’re available at pretty much every bank and lender in the nation.

That means you can use any bank you wish and/or shop your rate quite a bit more. Not all lenders offer FHA mortgage loans, so you might be limited in that respect.

Additionally, conventional loans can be used to finance just about any property, whereas some condo complexes (and even some houses) aren’t approved for FHA financing.

If you’re actively shopping for a property, real estate agents will probably point this out to you.

The FHA also has minimum property standards that must be met, so even if you’re a great borrower, the property itself could hold you back from obtaining financing.

In other words, you might have no choice but to go the conventional route if the condo you want to buy doesn’t allow FHA financing.

The same goes for second homes and non-owner investment properties. If you don’t intend to occupy the property, you will have no choice but to go with a conventional loan.

Let me make it very clear; the FHA home loan program is only good for owner-occupied properties!

Lastly, a home seller may favor a buyer with a conventional loan, knowing it’s a safer bet to close.

This is related to the mandatory home inspection on FHA-backed loans, along with a stricter appraisal process, especially if the property happens to come in below value.

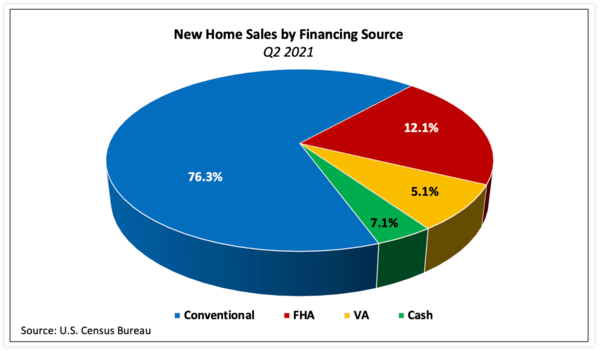

Conventional Loan vs. FHA Loan Share

A new analysis from the National Association of Home Builders (NAHB) found that conventional home loans were used to finance 76.3% of new home sales in the second quarter of 2021.

That was the largest share since the beginning of the Great Recession back in 2008.

They were very popular in the lead up to the mortgage crisis because most were non-government, private-label.

We’re talking a 90% market share thanks to all those option ARMs, interest-only loans, jumbo loans, and so on.

The conventional loan share has once again become very dominant, in part due to a competitive housing market that requires larger down payments.

The NAHB notes that today’s home buyers are wealthier thanks to big stock market returns and low mortgage rates.

This has effectively allowed them to avoid the FHA and its pricey mortgage insurance and property requirements.

Over time, this can obviously change, but at the moment FHA loans are mostly out of favor with a mere 12.1% share of new home sales.

In a competitive housing market, FHA loans might not be a good choice if you want to win a bidding war!

Are Fannie Mae and FHA the Same Thing?

People seem to confuse these two, maybe because they both start with the letter “F.”

So let’s put it to rest. The answer is NO.

Fannie Mae is one of the two government-sponsored enterprises (a quasi-public company) along with Freddie Mac that issues conforming mortgages.

The FHA stands for Federal Housing Administration, a government housing agency that insures residential mortgages.

They have a similar mission to promote homeownership and compete with one another, but they are two completely different entities.

Ultimately, Fannie Mae is a private sector company, while the FHA is a government agency that represents the public sector.

Final Word: Is an FHA Loan Better than a Conventional One?

- There is no definitive yes or no answer, but a seller will likely favor a buyer with a conventional loan approval

- Every loan scenario is unique so be sure to look into both options when shopping your mortgage

- Also consider how long you’ll keep the loan and what your financial goals are

- Compare and contrast and do the math, there are no shortcuts here if you want to save money!

These days, both FHA and conventional loans could make sense depending on your unique loan scenario. You can’t really say one is better than the other without knowing all the particulars.

And as noted, you or the property may not even qualify for an FHA loan to begin with, so the choice might be made out of necessity.

The same could be true if your FICO score is below 620, at which point conventional financing could be out.

Both loan programs offer competitive mortgage rates and closing costs, and flexible underwriting guidelines, so you’ll really have to do the math to determine which is best for your particular situation.

Even with mortgage insurance factored in, it may be cheaper to go with an FHA loan if you receive a lender credit and/or a lower mortgage rate as a result.

Conversely, a slightly higher mortgage rate on a conventional loan may make sense to avoid the costly mortgage insurance tied to FHA loans.

Generally speaking, those with low credit scores and little set aside for down payment may do better with an FHA loan.

Whereas those with higher credit scores and more sizable down payments could save money by going with a conventional loan.

Start with an FHA Loan, Then Move On to Conventional

Also consider the long term picture. While an FHA loan might be cheaper early on, you could be stuck paying the mortgage insurance for life.

With a conventional loan, you’ll eventually be able to drop the PMI and save some dough.

What a lot of folks tend to do is start with an FHA loan, build some equity (typically through regular mortgage payments and home price appreciation), and then refinance to a conventional loan.

In that sense, both loan types could serve one borrower over time.

Your loan officer or mortgage broker will be able to tell if you qualify for both types of loans, and determine which will cost less both short and long-term.

Ask for a side-by-side cost analysis, but also make sure you understand why one is better than the other. Don’t just take their word for it! They might be inclined to sell you one over the other…

Lastly, be sure to consider the property as well, as both types of financing may not even be an option.

Tip: If you want a zero down loan, aka have nothing in your savings account, consider VA loans or USDA home loans instead, both of which don’t require a down payment.

There is also the FHA 203k loan program, which allows you to make home improvements and get long-term financing in one loan.

Now let’s sum it all up by taking a look at a condensed list of pros and cons for FHA and conventional loan programs.

FHA Loan Pros

- Low down payment requirement (3.5% down)

- Lower credit score needed (580 for max financing)

- Lower mortgage rates in most cases

- May be easier to qualify for than a conventional loan (higher DTIs allowed)

- Shorter waiting period to get approved after foreclosure, short sale, etc.

- No prepayment penalty

- No asset reserve requirement (for 1-2 unit properties)

- Gift funds can cover 100% of closing costs and down payment

- Streamlined FHA refinances are fast, cheap, and easy

FHA Loan Cons

- Slightly higher minimum down payment requirement (3.5% vs. 3%)

- Subject to mortgage insurance (for full term of mortgage in many cases)

- Must pay upfront and monthly mortgage insurance premiums

- Fewer loan type options than conventional loans

- Only available on owner-occupied properties

- Mandatory home inspection and strict appraisal guidelines

- Many condominium complexes aren’t approved for FHA financing

- Loan limits are lower in more affordable regions of the country

- Generally only allowed to have one FHA loan at a time

- May take longer to close your loan

- Sellers tend to favor buyers with conventional loans because they’re generally easier to fund

Conventional Loan Pros

- Lower minimum down payment requirement (3%)

- No mortgage insurance requirement if 80% LTV or lower

- Can cancel mortgage insurance at 80% LTV

- Can be used on all property and occupancy types

- Many more loan program options available

- Can hold numerous conventional loans at given time

- No maximum loan limit and conforming loan limit much higher than the FHA floor

- More lenders to choose from (nearly every bank offers conventional loans)

- Might be able to close your loan faster

- No mandatory home inspection and more flexible appraisal guidelines

- LLPAs are waived for certain types of loans and for first-time home buyers with qualifying incomes

Conventional Loan Cons

- Higher credit score requirements (minimum 620 credit score)

- Slightly higher mortgage rates

- May be more difficult to qualify for than an FHA loan

- Mortgage insurance still required for loans above 80% LTV

- Reserves may be required to qualify

- Possible prepayment penalty (not common these days)

- Student loan payments could push you over DTI limit