Interested in a 40-Year Fixed Mortgage?

- If you need even more time to pay off your mortgage

- Or need to get the monthly payment down to boost affordability

- A 40-year fixed mortgage could be one alternative to consider

- But they’re harder to come by these days and aren’t well-suited for everyone

Every now and then, I take a look at a specific mortgage product to determine if it could be a good fit for a prospective (or existing) homeowner.

Today, we’ll discuss a formerly popular home loan option, the “40-year mortgage.” It was all the rage during the prior housing boom in the early 2000s.

But also partially to blame for the housing crisis that took place shortly after.

Still, with mortgage rates now double what they were to start the year, they could make a resurgence.

What Is a 40-Year Mortgage?

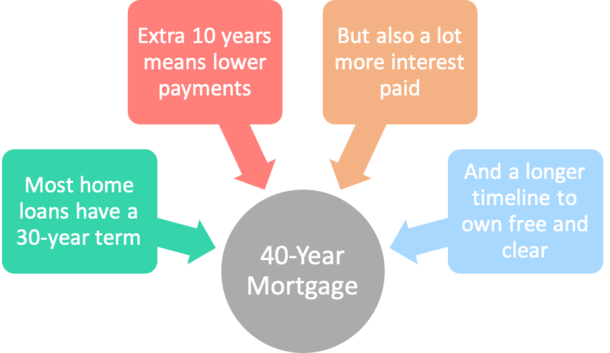

A 40-year mortgage is a home loan with a loan term that lasts for 40 years. This is 10 years longer than the typical 30-year loan term attached to most mortgages.

You may already be thinking, “40 years? I thought mortgages had terms of 30 years?” Is this a mistake?

Well, you’d be mostly right. The majority of mortgages issued today do have terms of 30 years. It’s certainly the most common loan term out there.

In fact, aside from 30-year fixed mortgages, which clearly last for 30 years, as the name implies, most adjustable-rate mortgages also have terms of 30 years, despite lacking any reference to 30 years in their title.

So that 5/1 ARM or 7/1 ARM you’ve got your eye on still has a 30-year term, meaning it’s fixed for the first five or seven years.

It then becomes adjustable for the remaining 25 or 23 years, respectively. This is one reason why consumers have a great amount of difficulty understanding mortgages.

Only the 15-year mortgage and 10-year fixed come with different loan terms, 15 and 10 years respectively.

Why Go With a 40-Year Mortgage Term?

- It’s an extra 10 years over the typical 30-year loan term

- Offered as a means to lower monthly mortgage payments

- This can make the home loan more affordable or allow money to allocated elsewhere

- But it will also lead to a lot more interest paid over the longer term (and a slower payoff)

Okay, so we know the 40-year mortgage bucks the trend, and adds 10 years on to the standard mortgage term. But why?

What’s the point of paying a mortgage for an extra decade? That sounds like a literal lifetime commitment. Especially since 30 years is already way too long.

Well, the longer a mortgage amortizes (is paid off), the lower the monthly mortgage payment.

Essentially, payments are stretched out over a longer period of time. Instead of 360 months, you’re looking at 480 months.

Let’s look at an example of a 40-year fixed mortgage:

Loan amount: $300,000

30-year fixed: $1,703.37 @5.5%

40-year fixed: $1,598.66 @5.75%

As you can see, the monthly mortgage payment on the 40-year mortgage is roughly $105 less each month thanks to that longer period of time to pay it off.

That extra cash could be used to pay off student loans, credit cards, personal loans, and other higher-APR debt you may have.

Or it could be allocated toward a different investment or retirement account. It could also make a real estate purchase slightly more affordable.

The bad news is you’ll pay much more interest over the life of the loan, and it’ll take a very long time to build a meaningful amount of home equity.

If you use a mortgage calculator, make sure it’s set at 480 months. And pay close attention to how much interest is paid versus a loan with a term of 360 months. It’ll be an eye-opener.

In the example above, it’s about $150,000 more in interest for the 40-year mortgage, assuming it’s held until maturity.

Check out my new 40-year mortgage calculator to run your own numbers!

40-Year Mortgage Rates Are Slightly Higher Than 30-Year Rates

- Expect 40-year mortgage rates to be slightly higher than interest rates on 30-year fixed mortgages

- How much higher will depend on the lender in question and your unique loan scenario

- You essentially pay a premium to lock in an interest rate for an additional 10 years

- And the slower payoff means you must pay a higher rate of interest to the bank/lender

You may have also noticed that the mortgage rate on the 40-year mortgage in my example is 0.25% higher than the interest rate on the 30-year fixed. There’s a reason for that.

Simply put, you pay a premium for a longer amortization period. This is the opposite of a 15-year fixed, where you receive a discount for paying your mortgage off faster.

After all, a bank or lender is willing to give you a fixed rate for four decades, so they’re going to want a slight premium in exchange for all that uncertainty.

In other words, expect 40-year mortgage rates to be slightly more expensive. It might only be .125% higher than the 30-year, but could definitely range from bank to bank.

More aggressive borrowers could even invest that $105 each month in a high-yielding retirement account and essentially try to beat the relatively low interest rate on their mortgage.

The bigger problem is finding a lender that offers the product to begin with.

A 40-Year Mortgage Can Provide Short-Term Liquidity

The short-term savings of a 40-year mortgage can increase how much house a buyer can afford.

And also make qualifying easier (or even feasible) if a borrower’s debt-to-income ratio is too high for a 30-year mortgage. That’s assuming the lender qualifies the borrower at the 40-year loan payment…

This is essentially why a borrower would go with the 40-year fixed – to buy more house or make their home loan more “affordable.”

You might also come across a 40-year mortgage with a 10-year interest-only period. During the first decade, payments would be significantly lower due to the longer amortization and lack of principal repayment.

After those 10 years, you’d effectively have a 30-year fixed with a fully-amortized payment.

There are also adjustable-rate mortgages with 40-year loan terms, which make monthly payments more affordable.

Nowadays, a 40-year mortgage term may even be part of a loan modification program to make payments more affordable for a struggling borrower.

When combined with an interest rate cut on their current mortgage, the combo can help a borrower stay put in their home for the long haul.

The Downsides of a 40-Year Mortgage

- Loan is paid much back slower (harder to build equity)

- Most of the mortgage payment consists of interest

- May not be much cheaper than a 30-year fixed when all is said and done

- And they’re not easy to find these days but that could change if rates remain elevated

While the benefits of a 40-year mortgage sound good, a borrower who chooses to go with a such a loan is paying a premium to do so.

As mentioned, they are higher-rate home loans, so that cuts into the payment “discount” afforded by a 40-year mortgage.

And while the monthly mortgage payment might be lower, the total interest paid over the full loan term will be much higher, which makes one question whether $100 or so in monthly savings is worth it.

On smaller mortgages, the payment different will be even more negligible. It may also be difficult to find a 40-year mortgage, since not all lenders offer them.

In fact, the Qualified Mortgage rule outlawed loan terms longer than 30 years, so 40-year mortgages aren’t even QM-compliant.

That means you’ll probably need to go with a specialty mortgage lender or portfolio lender if you want one.

Additionally, a longer amortization period means you’ll build home equity a lot slower, which could prove to be an issue if you need to sell your home or refinance in the future and your loan-to-value ratio is still sky-high. This could be the case if you come in with a low down payment.

Some Benefits to a 40-Year Mortgage

- Could be a good short-term solution if you need monthly payment relief

- Or if you don’t plan on staying in the property for very long

- Those who wish to use their money elsewhere might be attracted to the program

- But keep in mind that you pay for the privilege of a longer term via a higher interest rate

One could argue that most homeowners don’t stick with their mortgage full term anyway, let alone for 10 years, so why pay more each month? Or worry that it’ll take forever to pay it off?

A 40-year mortgage could also serve as a good alternative to an interest-only home loan, the latter of which won’t build any equity, and could eventually land a homeowner in an underwater position.

These mortgage types are also safer than an ARM (assuming it’s a 40-year fixed rate), which can adjust higher once the fixed period comes to an end.

So you won’t have to contend with any interest rate adjustments, which could make it easier to sleep at night, especially if you’re a first-time home buyer.

As always, do plenty of homework (and math using a mortgage calculator) and consult with a loan officer or mortgage broker to determine what’s best for you and your unique situation.

Tip: You may come across a “40 due in 30” as well, which is essentially a 30-year balloon mortgage that amortizes like it has a 40-year term.

That keeps monthly payments low, but the balance due at 30-year mark. Again, most of these probably aren’t kept full term, so it might be moot.

Is a 40-Year Mortgage a Good Idea?

Some say you should only buy a house if you can afford a 15-year mortgage. So if we’re talking a 40-year mortgage, which is 10 years beyond the standard 30-year fixed, it might be a red flag.

It may reveal that you aren’t qualified for the mortgage in question, at least from a traditional, more conservative standpoint.

Of course, there are exceptions to every rule, and it depends why a homeowner would seek out this type of financing.

They might want to deploy their cash in other places where its yield is higher than the rate on a 40-year mortgage.

At the same time, for the typical home buyer, a 40-year loan probably isn’t the best idea because so much more interest is paid throughout the loan term.

And it takes a significant amount of time to pay off the loan. But every situation is unique.

Are 40-Year Mortgages Available?

One last thing. As noted above, you might have difficulty finding a 40-year mortgage because not many lenders offer them.

So they might not even be available to begin with, which stops the debate in its tracks. Before you spend too much time thinking about getting one, maybe see if anyone offers them.

The reason they’re scarce is mostly because the Consumer Financial Protection Bureau (CFPB) outlawed loan terms beyond 30 years on most residential home loans.

You can still get one, but it won’t be considered a Qualified Mortgage (QM). And only big banks and niche non-QM lenders offer such products, typically at a premium.

So even if you find one, the pricing might not be great given the lack of competition. At the end of the day, you might be better off with a more traditional loan program instead.

(photo: Derek Swanson)

- Mortgage Rates Could Drop as Much as Half a Percent with Basel Re-Proposal - June 30, 2026

- Mortgage Rates Face Big Week of Jobs Data - June 29, 2026

- Are Mortgage Rates Finally Poised to Start Falling Again? - June 25, 2026

40 years should only be use as a last resort to save a home. On higher amount loans. For cushion years need.

40 years should be never be a negative.

I had 26 years left on 130,000 short amount was 3200 went in modification on 3200 paid 2500 bank failed to credit amount and less the years. They may a huge profit on small amount that can be paid in less then 2 years.