It’s time for another mortgage match-up: “Mortgage rate vs. APR.”

If you’re shopping for real estate or looking to refinance, and you’ve seen a certain mortgage rate advertised, you may have noticed a second, similar percentage adjacent to or below that interest rate, possibly in smaller, fine print.

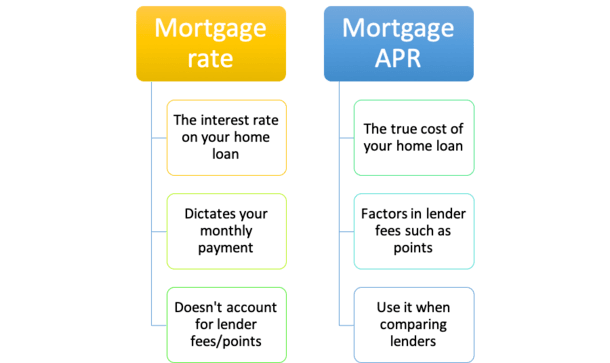

But why? Well, one is the mortgage rate, which is the interest rate you’ll pay every month on your home loan, which dictates what your monthly payments will be.

And the other is the Annual Percentage Rate, or APR, which is the interest rate factoring in certain loan costs, such as processing, underwriting, loan origination fees, mortgage points, broker fees, and so on.

Third-party loan fees, including title insurance and appraisal fees, which are provided by vendors other than the lender, typically aren’t included in this figure.

Understanding the difference between these two figures is very important, and they will undoubtedly come up a lot as you compare mortgage loans from different lenders.

That’s assuming you actually take the time to gather more than just one quote, which you absolutely should if your goal is to save money.

Mortgage Rate vs. APR

- The APR is calculated to determine the cost of the loan

- It factors in lender fees and other closing costs

- The interest rate simply dictates how much interest you’ll pay monthly, annually, and over the life of the loan

- And is used to calculate with what your monthly payment will be

In short, the APR is a calculation used to determine the true cost of a loan, otherwise known as the cost of borrowing, represented annually.

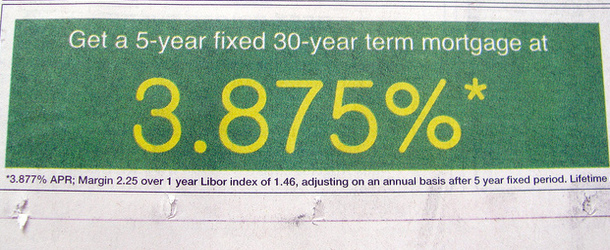

Instead of a bank or mortgage lender telling you that your rate is 6.5% with $8,000 in fees, they’ll just say the annual percentage rate is 6.87% with those fees factored in.

The annual percentage rate was created to prevent financial institutions from not disclosing fees that went into a loan to make the rate appear better than the competition.

For example, an unscrupulous lender could advertise mortgage interest rates well below the competition while downplaying the associated fees, making their offer look unbeatable.

In reality, it could be a terrible deal once the total costs were factored in.

The APR addresses this issue by including most of the fees lenders charge during the loan transaction. These fees are then rolled into the interest rate to come up with the APR.

If you receive a loan estimate from a bank or lender, you’ll find this figure on the last page, which can be handy for comparing mortgages.

However, it’s still not sufficient to choose a mortgage based on APR alone, because lenders do not include all the fees associated with your loan transaction.

You might see something like “fees included in APR” next to the rate. Pay attention to what’s actually included. The APR also assumes a loan will be paid off at the end of the full term, whether it be 15 or 30 years.

Most homeowners hold onto their mortgages for a significantly shorter period of time, which will completely throw off the actual APR calculation.

Additionally, APR is not an effective measure between different products, only like products because of APR’s time dependency.

Mortgage APR = More Accurate Representation of Loan Cost

- The APR is a more accurate representation of how much the home loan will cost you

- Because it factors in points and other lender fees you might pay

- This is why it’s important to look beyond just the interest rate offered

- But it’s not perfect either

As noted, the mortgage APR is basically the true cost of the loan, or at least a bit more accurate than a simple interest rate. I’ll explain why with a basic example.

Let’s look at an example of interest rates and APR:

Mortgage Rate X: 4.50%, 4.838% APR

Mortgage Rate Y: 4.75%, 4.836% APR

The advertised mortgage rate “X” is 4.50%, but requires that two mortgage points be paid – it also has $2,000 in additional closing costs, which pushes the APR to 4.838%.

Meanwhile, advertised mortgage rate “Y” is offered with no points and just $1,000 in closing costs, so the APR is 4.836%, just below that of mortgage rate “X.”

So even though one advertised mortgage rate might be lower than another, once closing costs are factored in, it could actually end up costing you more.

That’s why it’s very important to consider both the APR and interest rates.

At the same time, the monthly mortgage payment on mortgage rate “X” will still be cheaper each month because of the lower interest rate.

For example, if the loan amount in our example is $200,000, the monthly principal and interest mortgage payment would be $1,013.37 on mortgage rate “X” versus $1,043.29 on mortgage rate “Y.”

So if you’re more concerned with your monthly payments as opposed to loan cost, you might still be interested in the slightly more expensive option.

Of course, the goal should be both a low APR and a lower mortgage rate, which you might be able to achieve by taking the time to shop your rate and compare lenders.

Mortgage APR Limitations

- There is a major flaw with mortgage APR

- Mortgage lenders don’t always include the same fees in the calculation

- So it’s very difficult to get an apples-to-apples comparison

- APR also assumes you will hold the loan to maturity

Though it’s extremely important to know both the mortgage rate and the APR, there are limitations to this calculation.

As noted, some costs aren’t included in the APR, and banks and mortgage lenders calculate APR differently, so it’s not always simple to get an apples-to-apples comparison.

However, many third-party costs are pretty similar, so it might not matter too much. You may just want to take inventory of these costs to ensure they aren’t exorbitant or far above what other banks are charging.

Additionally, the mortgage APR assumes you’ll hold the loan for its full amortization, but most people sell or refinance long before loan maturity. That can change the picture quite a bit.

Simply put, high-cost loans held for a short period will actually result in a higher APR than advertised, because the costs aren’t spread over the full term as anticipated by the calculation.

This is why it doesn’t make sense to pay discount points on a home loan you’ll only keep for a few years. It takes time for the benefit of the lower interest rate to recoup the upfront costs.

In short, the APR will go down as the loan term goes up, and vice versa, because it is the yearly cost of borrowing. With more time, costs are spread out over more years.

Watch Out for APR on Adjustable-Rate Mortgages

- APR on ARMs can be especially deceiving

- Because the fully-indexed rate is merely estimated

- Using a fixed margin and a variable index that may change

- Disclosures often read APR may increase after loan consummation due to changes in the index

If you’re shopping for an adjustable-rate mortgage, you may see that the APR is lower than the mortgage rate.

This is essentially because lenders calculate the fully indexed rate (once it adjusts) by combining the margin and associated mortgage index.

And since mortgage indexes are so low at the moment, they assume you’ll have a lower rate (and mortgage payment) than your original start rate once the loan adjusts, which may or may not be the case.

A lot can change in a few short years and the fully-indexed rate may indeed be higher.

Don’t bank on the fully-indexed rate being lower because rates are historically close to rock-bottom and probably won’t stay that way for long.

Of course, most homeowners only hold onto adjustable-rate mortgages for a handful of years before refinancing or selling, so it might not matter too much. That monthly payment might be more important.

When it comes to fixed-rate mortgages, lenders will have a more difficult time making the math favorable, which is why you’ll typically see APR that exceeds the interest rate unless it’s a no cost refinance.

And while interest rates are generally low on FHA loans, the effect of the required upfront MIP and annual mortgage insurance can make the APR skyrocket in a hurry. In other words, they aren’t as cheap as they appear.

How to Calculate Mortgage APR

- First take your full loan amount

- Then subtract out-of-pocket closing costs to get the net loan amount

- Next calculate the monthly mortgage payment using the full loan amount

- Finally input that full monthly payment with the net loan amount to get your APR

While probably not necessary, it’s always nice to know how things get calculated using real math, as opposed to using a completely automated loan calculator.

This way you can check your lender’s math, if need be. And even impress or scare them along the way.

A simple way to calculate mortgage APR is by subtracting the loan costs from the loan amount because what you’re paying for the loan effectively reduces what you have borrowed.

For example, if your mortgage is $100,000, but there are $2,000 in out-of-pocket loan costs, you’re really only borrowing $98,000 from the bank.

Now grab a basic mortgage calculator (okay we’re still using a calculator but not an APR calculator) and input the full $100,000 loan amount and the interest rate (let’s pretend it’s 6% in our example). That will generate a monthly payment amount of $599.55.

Next, change the loan amount to $98,000, but keep the monthly payment amount of $599.55. Also make sure the interest rate and/or APR box is empty. Some mortgage calculators will allow you to do this, some won’t.

Hit calculate and you should see an APR of 6.189%. It’s a two-step process, but not that hard to manage.

See, calculating the APR isn’t so hard! Well, it gets a lot more difficult once we start talking about financing closing costs and tacking on mortgage insurance and the like.

So you should probably stick to the calculator unless the loan costs are super basic.

To sum it up, the mortgage APR provides a more complete cost of borrowing money, whereas the mortgage rate simply tells you what your payment will be each month.

Take the time to evaluate both the costs of the loan and the mortgage interest rate, instead of merely comparing payments with a mortgage calculator. And always consider how long you’ll keep the loan!

The following fees are usually included in mortgage APR:

– Discount points/broker fee/yield-spread premium

– Origination fee

– Mortgage points

– Discount points

– Prepaid interest

– Processing fee

– Underwriting fee

– Document drawing fee

– Mortgage insurance

Notice that most of the fees above are charged by the lender, not a third-party.

The following fees are typically not included in mortgage APR:

– Title fees

– Escrow fees

– Notary fees

– Recording fees

– Credit report

– Appraisal report fee

– Appraisal review fee

– Home inspection fees

– Pest inspection fees

– Doc prep fees

– Attorney fee

– Hazard insurance

– Escrows

Notice that the latter group are third-party fees, which aren’t from the lender itself. They include title/escrow company fees, home inspections, and so on.

Tip: Are mortgage rates negotiable?

- Rocket Mortgage Completes Redfin Takeover, Offers $6,000 Home Buyer Credit - July 1, 2025

- Mortgage Rates Quietly Fall to Lows of 2025 - June 30, 2025

- Trump Wants Interest Rates Cut to 1%. What Would That Mean for Mortgage Rates? - June 30, 2025