More fun and exciting mortgage Q&A: “What does a monthly mortgage payment consist of?”

Have you ever been curious what you’re paying each month to live in your shiny new (or possibly dingy old) home or condo? Or how much it might cost per month to acquire such real estate?

Let’s learn more about what goes into a home loan payment so you can better estimate your total monthly outlay, or if you’re a first-time home buyer, narrow down an appropriate purchase price.

Knowing what it all costs is a cornerstone to the rent vs. buy question, and also key to knowing how much house you might be able to afford if you decide to dive into the real estate market.

What a Typical Mortgage Payment Includes

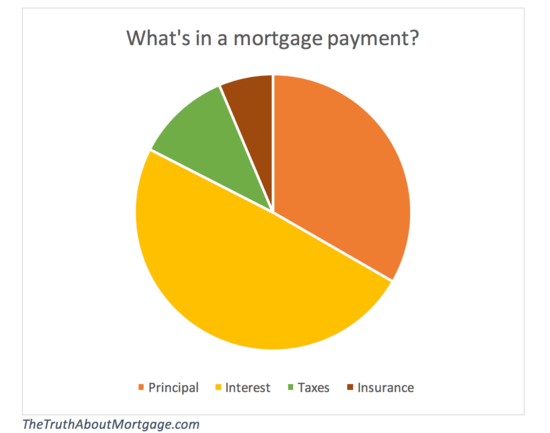

A monthly home mortgage payment, assuming it’s not an interest-only loan, generally consists of four key components:

- a principal portion

- an interest portion

- property taxes

- homeowners insurance

Mortgage Payment = PITI

There’s a handy acronym to sum up the four parts of a mortgage payment known as “PITI.”

When you say it, it sounds like “pity.” And I suppose it is a pity that we have to make mortgage payments every month, often for a staggering 30 years…or 360 months, but I digress.

Anyway, mortgage lenders typically want “X” number of months of PITI for cash reserves if you’re verifying assets when you apply for a home loan.

In short, this tells the mortgage underwriter you can actually pay back the loan, at least for a few months…

Lenders will also use the PITI payment to determine your monthly housing expense, which is then used to calculate your DTI ratio. So it’s pretty important!

Let’s look at each portion of the overall loan payment to get a better understanding of what you’re paying each month.

The principal portion of your payment is essentially the amount of debt you are borrowing, which eventually transitions into your ownership in the home as it is paid back, also known as home equity.

The interest portion of your payment is the cost of borrowing that money for the loan, or the expense the bank or mortgage lender charges for taking on the risk (how mortgage interest works).

The tax portion of the payment is paid to the local government based on the assessed property value and tax rate for the area.

Finally, the insurance portion of the payment covers homeowners/hazard insurance, which protects the borrower (and lender) from a number of dangers and provides liability coverage.

* You may also see the acronym “PITIA,” which stands for principal, interest, taxes, insurance, and association dues. This may apply if there is an HOA that charges due for your property each month.

Does the Mortgage Payment Include Insurance?

- Your monthly mortgage payment may include insurance

- Including both homeowners insurance and PMI (if applicable)

- Assuming your loan is escrowed/impounded (which many are)

- Impounds are required on loans with LTVs above 80%

- And also on FHA loans, VA loans, and USDA loans

For those with a mortgage impound account (typically required for a high LTV loan over 80%), taxes and insurance are paid monthly as part of the overall mortgage payment.

So you’ll pay the full PITI payment each month, as discussed above.

Instead of paying the mortgage and taxes/insurance separately, you’ll make an installment payment each month that covers all of those items.

Then when taxes/insurance are due, they’ll be paid from those proceeds, which are held in an escrow account.

If you aren’t subject to impounds, you must pay taxes and insurance directly to the county assessor/insurer once or twice a year, and the mortgage payment each month will consist of only principal and interest.

This can be a relief on a monthly basis, but make sure you’re good about setting aside money to pay for taxes and insurance when they eventually become due.

I’ve had friends who forgot they were on the hook for a big property tax bill, and didn’t save accordingly. Sometimes it’s better just to have the impound account…

If you’re unsure of what’s included in your mortgage payment, simply call your loan servicer or check out your payment breakdown on the servicing website. It’s best not to leave anything to chance.

Note: If your loan-to-value ratio exceeds 80 percent on a single loan, you’ll also have to pay mortgage insurance on top of the aforementioned costs, which is one reason why putting 20% down can be a smart move.

How Are Mortgage Payments Applied?

- Because of the way mortgage loans are amortized

- Early payments consist mostly of interest

- With a small proportion going toward principal

- Over time this shifts until monthly payments are mostly principal

In the beginning of the loan term, mortgage payments primarily go toward paying off interest because the outstanding loan balance is so high.

While this may be viewed as a negative, it does mean mortgage interest tax deductions are bigger and more beneficial early on.

Over the years, as the outstanding balance decreases, more of the monthly mortgage payment will go toward principal each month until you eventually own the home outright. This is how amortization works.

It also explains why some savvy homeowners choose to make biweekly mortgage payments, thereby increasing the amount of principal paid early on and decreasing the amount of interest paid over the life of the loan.

Doing so will also shorten your mortgage term, which is beneficial if you want to own your home sooner, but don’t want the commitment of larger monthly payments associated with certain loan programs such as the 15-year fixed.

Tip: As a rule of thumb, the longer your loan term, the more you’ll pay in interest because the loan is paid off slower. If you’re able to accelerate your payoff, you’ll pay less interest.

Check out my extra mortgage payment calculator if you want to make a dent in your loan sooner and save on interest.

What Will My Mortgage Payment Be?

- Add up the following items (not all may apply)

- Principal and interest

- Property taxes

- Homeowners insurance

- HOA dues

- Mortgage insurance

- Flood insurance

When attempting to figure out what you’ll be paying your lender each month, consider all the ingredients of a mortgage payment along with your mortgage interest rate.

Start with the home’s purchase price, which will be driven by the health of the housing market and your budget, factoring in down payment.

Once you know your approximate loan amount, you can check out my mortgage rate charts to quickly ballpark monthly payments at certain price points.

Know that loan rates can vary tremendously based on your credit score, down payment, occupancy, property type, and so.

Loan type is also a big consideration, with adjustable rates generally a lot cheaper than fixed interest rates.

For example, a 5/1 adjustable-rate mortgage will result in a lower monthly payment than a 30-year fixed mortgage, all else being equal.

If we’re talking jumbo loans, you might be hit twice – once for the larger loan amount and a second time in the way of pricing, which can often be higher than that of conforming loans.

Also be sure to compare rates along the way because they can vary a ton between lenders for the same exact product!

As noted, if you’ve got an impound account, add up the principal, interest, taxes, and insurance.

Those last two bits may be estimated by your lender, but it’s better to get it straight from the horse’s mouth.

The principal and interest portion is something you should be able to calculate on your own. Simply plug your loan amount and interest rate into a mortgage payment calculator to figure out the monthly payment.

If it’s interest-only, plug those two items into an IO calculator. Or simply use just the interest portion from the first fully-amortized payment. Principal will no longer be part of the equation.

The mortgage payment on an interest-only loan consists of just interest, taxes, and insurance, meaning you can only build equity in your home if the property value appreciates.

If we’re talking about a negative amortization loan, such as the once popular option arm, making the minimum payment wouldn’t even cover the interest due each month. Of course, you’d still have to pay the required taxes and insurance.

Don’t forget the extras. Do you need to pay mortgage insurance premiums each month? For example, there are monthly mortgage insurance premiums on FHA loans that must be paid.

What about monthly HOA fees? If it’s a condo, there probably are, though you’ll probably pay them separately to the association and not your lender.

Either way, it’s good to know what your total housing payment will be so you can budget accordingly.

Once you have all this key information, you can fire up a home affordability calculator to see what it’ll all set you back.

The mortgage interest rates and payments you see advertised typically only include principal and interest. That makes them look relatively cheap.

Once everything else is added, the payment can look a whole lot different depending on the state you live in and the cost of the home.

In summary, no one enjoys making mortgage payments every month, but knowing where that money is actually going should make you a more informed borrower.

And it could even save you some money! Certainly don’t make a home buying decision without knowing the answer to this core question.

Read more: When do mortgage payments start?

- Mortgage Rates Quietly Fall to Lows of 2025 - June 30, 2025

- Trump Wants Interest Rates Cut to 1%. What Would That Mean for Mortgage Rates? - June 30, 2025

- What the Fannie Mae and Freddie Mac Crypto Order Really Means - June 26, 2025

I owe 55,000.00 on my mortgage. My payments are 333.40 per month principal/interest only. I owe 24 years on my loan. How much can I add per month to make this a fifteen year note…?

Sandy,

Just find an early payoff calculator to determine how much extra is needed each month to pay off the loan in 15 years total. Keep in mind that extra payments weren’t being made for the first six years based on what you’re saying.

My mortgage payment is due on the 1st of the month. Can I put that date on the check even if it gets to the mortgage company before due date so they can’t take out the funds until the 1st.

Jodi,

Not sure, you may want to ask your specific lender/servicer first to be sure. Also, most mortgage lenders have a 15-day grace period so payments aren’t considered late until after the 15th.

I am behind a payment ($3300.00) on line of credit payment. Can I use my charge account to pay.

Ruth,

While not necessarily recommended, there are services like Plastiq that allow payments with charge cards.