There Are Many Different Types of Mortgages

- A variety of home loan programs exist today to serve different needs

- But most borrowers just go with the 30-year fixed mortgage

- It holds a near-90% market share for home purchase loans (and also a large share of refinances)

- Take the time to learn about other products that could save you a substantial amount of money

Types of Mortgages by Category

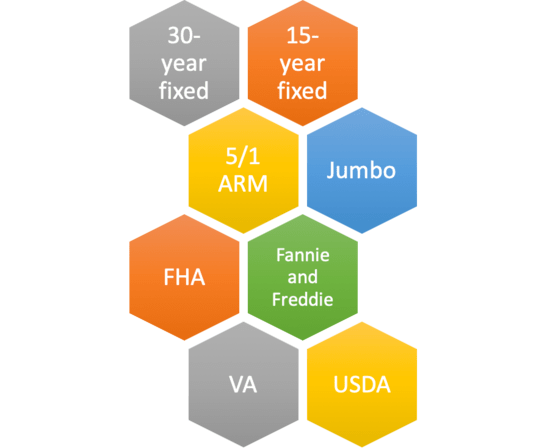

Conforming Loan: A mortgage backed by Fannie Mae or Freddie Mac (most common)

Jumbo Loan: A mortgage with a loan amount that exceeds the conforming loan limit (currently $806,500) for the year 2025.

Government Loan: A home loan backed by a government agency (includes FHA, VA, and USDA loans)

Conventional Loan: A non-government home loan (can be conforming or jumbo based on loan amount)

Fixed-Rate Mortgage: A home loan that features a fixed interest rate (does not change entire loan term)

Adjustable-Rate Mortgage: A home loan with a variable interest rate (can adjust higher/lower during loan term)

Popular Home Loan Programs Available Today

30-Year Fixed: Interest rate never changes during entire 30-year term

15-Year Fixed: Interest rate never changes during entire 15-year term

5/1 ARM: Interest rate is fixed for first 5 years and adjustable for 25

7/1 ARM: Interest rate is fixed for first 7 years and adjustable for 23

10/1 ARM: Interest rate is fixed for first 10 years and adjustable for 20

Let’s talk about the many different types of mortgages and loan programs available to prospective home buyers and existing homeowners today.

There are dozens out there to choose from, and mortgage lenders are constantly coming up with creative ways to wrangle in new customers.

The five I’ve listed above happen to be the most common and will typically be offered by most banks, credit unions, and lenders.

The type of home loan you decide to go with can make or break you as a borrower, so be sure you fully understand what you’re getting into before committing to anything.

In the early 2000s, there was an abundance of ridiculous loan programs that allowed just about anyone to buy a home, whether they truly qualified or not.

There were the now notorious 1% start rate loans, often referred to as neg-ams or pick-a-payment programs.

And 40-year and 50-year term loans that stretched the mortgage payment out over what seemed like a lifetime.

Anything to keep that monthly payment down…never mind paying off the darn thing.

Today’s Mortgages Are Pretty Tame

- The Qualified Mortgage (QM) rule introduced after the early 2000s mortgage crisis changed the game

- Nowadays most mortgages are fully-amortized (meaning no interest-only or neg-am options)

- And most are boring old fixed-rate mortgages (typically the 30-year fixed because it’s the most affordable)

- ARMs and loans with other exotic features are now mostly niche products for real estate investors

Times have changed since the mortgage crisis of the early 2000s. Today’s mortgage loans are a lot more sensible, and mortgage underwriting much more conservative.

You can thank the “ability-to-repay” rule for that, along with the Qualified Mortgage (QM), which outlawed many risky features.

Things like interest-only, negative amortization, balloon payments, and loans terms beyond 30 years aren’t permitted if it’s a QM loan. And most loans today adhere to the QM definition.

At the same time, government lending (FHA loans and VA loans) has become very popular since those riskier types of loans were eliminated.

And most folks are simply going with a 30-year fixed without giving it much thought at all.

However, that doesn’t mean there aren’t interesting and potentially money-saving loan programs to suit all tastes and needs.

Aside from specific loan programs, I want to highlight the different categories of mortgages available to prospective homeowners.

Conforming and Non-Conforming Loans

- Mortgages eligible for purchase by Fannie Mae and Freddie Mac are known as conforming loans

- They are the most common type of mortgage available (60-70% market share)

- Easy to package and sell because they adhere to the pair’s underwriting guidelines

- Mortgage loans that fall outside this underwriting criteria are known as non-conforming loans

One way home loans are differentiated is by their government-sponsored enterprise (GSE) eligibility. If the loan meets requirements set forth by Fannie Mae and Freddie Mac, it is considered a conforming loan.

If the loan doesn’t meet all the mortgage underwriting requirements set forth by the pair of GSEs, it is considered a non-conforming loan.

Pretty much all mortgage lenders offer conforming loans because they are the easiest to sell to investors on the secondary market. Consider them your basic vanilla or apple pie type of mortgage.

One of the main guidelines that determines whether a mortgage is conforming or not is the loan amount.

Generally, a mortgage with a loan amount at or below $806,500 is considered conforming, whereas any loan amount above that is considered a jumbo loan.

However, in higher-priced areas along with Alaska and Hawaii, the conforming limit is 150% higher.

The conforming limit can change annually, and has risen quite a bit in the past few years as home prices skyrocketed.

A jumbo loan may meet all of Fannie Mae and Freddie Mac’s loan requirements, but if the loan amount exceeds the conforming limit, it will be considered non-conforming and typically carry a higher mortgage rate as a result.

If your loan amount is on the fringe of the conforming limit, sometimes simply dropping your loan amount a few thousand dollars can lower your mortgage rate tremendously.

Keep this in mind any time your loan amount is near the cutoff.

Conventional Home Loans and Government Mortgages

- Conventional is just another word for non-government

- So it can refer to lots of different types of home loans

- Including those backed by Fannie Mae/Freddie Mac and jumbo loans

- On the other hand, FHA, USDA, and VA loans are government mortgages

Mortgages are also classified as either “conventional loans” or “government loans.” Conventional loans can be conforming or jumbo, but are NOT insured or guaranteed by the government.

Then there are government loans, such as the widely popular FHA loan. This type of mortgage is backed by the Federal Housing Administration (FHA), a government housing agency.

Another common government home loan is the VA loan, backed by the Department of Veteran Affairs, which allows zero down financing.

There’s even a USDA home loan backed by the same folks that grade steaks! It too allows for 100% financing.

Now that you know a bit about different home loan types, we can focus on home loan programs.

As I mentioned earlier, there are a ton of different loan programs out there, and more seem to surface every day.

Let’s start with the most basic of mortgage loan programs, the 30-year fixed-rate loan.

Home Loan Programs: Look Beyond the 30-Year Fixed

- The 30-year fixed mortgage is the most common loan program

- Mainly because it’s easy to understand and low-risk

- But you should get to know the other loan programs as well

- To ensure you make the right loan choice for your unique situation

The 30-year fixed home loan is as simple as they come. Most mortgages are based on a 30-year amortization, meaning they are paid off in 30 years, and the 30-year fixed is no different.

It works just like how it sounds; it’s a 30-year term mortgage with an interest rate that is fixed for the entire 30 years.

Simply put, the loan will take 30 years to pay off, and the rate will stay fixed during those entire 30 years. There isn’t much else to it. This explains its immense popularity among home buyers.

Let’s say you secure a rate of 6.5% on a 30-year fixed loan with a loan amount of $500,000. You’ll have monthly mortgage payments of $3160.34 for a total of 360 months, or 30 years.

You will be required to pay the same amount each month until the loan is paid off. So the total amount you would pay on a $500,000 loan at 6.5% over 30 years would be $1,137,722.44.

Loan Amount: $500,000

Mortgage Interest Rate: 6.5%

Monthly Payment: $3,160.34

Interest Paid in Year One: $32,335.45

Interest Paid in Year Two: $31,961.17

Total Interest Paid Over Life of Loan: $637,722.44

Each year, though the monthly payment stays the same, the composition of the payment changes.

More money goes toward the principal balance and less going toward interest, due to a smaller outstanding balance each month the loan progresses.

While the numbers above look steep, most people don’t stay in a 30-year loan for 30 years.

They may either pay it down quicker by making higher monthly payments (biweekly mortgage payments), apply for a rate and term refinance, or sell their home and move on.

Consider the 15-Year Fixed If Affordability Isn’t an Issue

Another common and simple to understand loan is the 15-year fixed. This works exactly like the 30-year fixed except the same fixed payment is made for half the amount of time; 180 months or 15 years.

Obviously, the monthly payment will be much higher, but you will pay a lot less interest and gain more home equity in a shorter amount of time. Additionally, 15-year mortgage rates are substantially lower than 30-year rates.

People who have an ample amount of income usually prefer this type of loan to reduce the overall cost of financing a mortgage.

This is how it breaks down, assuming the same loan amount at a rate of 6%:

Monthly Payment: $4,219.28

Interest Paid in Year One: $29,432.07

Interest Paid in Year Two: $28,114.99

Total Interest Paid Over Life of Loan: $259,471.15

Interest Savings Over Life of Loan: $378,251.29

The monthly payment is significantly higher, but the amount of interest paid over the life of the loan is much less.

Because you’re putting more money toward the principal balance of the loan, you’re paying less interest each month versus the 30-year fixed loan.

As you can see, the interest savings are nearly $400,000 if you elect to go with the 15-year fixed mortgage.

It may seem like the obvious loan choice, but it’s more complicated if you factor in tax deductions and the potential of investing that money elsewhere.

Not to mention many prospective home buyers probably can’t afford a monthly mortgage payment that high to begin with, so for most it won’t even be a viable option.

Fixed-Rate Mortgage Alternatives

We’ve just scratched the surface here. There are plenty of alternatives to fixed mortgages, including a variety of adjustable-rate mortgages like the widely used 5/1 ARM or 7/1 ARM, or even 10/1 ARM, which could come with an even lower interest rate.

Be sure to take the time to educate yourself on the many home loan types out there and how they work.

You will also need to pay property taxes and insurance on top of this mortgage payment, so keep that in mind when figuring out how much house you can afford. And don’t forget closing costs either!

You should be a happier homeowner with a better chance of making on-time payments. And you might even save some dough!

If you want to a run a similar comparison, simply grab a mortgage calculator and plug in your own numbers.

What Is the Best Type of Mortgage for Most Homeowners?

While best is always hard to answer universally, most homeowners are probably best off with a 30-year fixed.

It’s the most popular for a reason. The loan term is long enough to keep payments low. But not too long, allowing homeowners to eventually pay off their loans in full.

Additionally, the mortgage rates are reasonable, and often pretty cheap relative to other loan programs.

Sure, a 15-year fixed will be cheaper and paid off in half the time, but most homeowners can’t afford them. Or will be financially stretched to do so.

Then there are ARMs, which are typically too high-risk for the standard homeowner due to the variable rate feature.

In terms of loan type, that decision might be driven by down payment and qualifying criteria.

I’ve written extensively on FHA vs. conventional loans. If you’re active duty or veteran, a VA loan might be the best choice. And those in rural areas can take advantage of USDA loans.

Lastly, I’ve discussed the best mortgage for a first-time home buyer, though again preferences will vary.

Learn about other types of mortgages including:

– Adjustable-rate mortgages

– Alt-A mortgages

– Balloon payment mortgages

– Bridge loans

– Hard money loans

– Home equity lines of credit

– Home equity loans

– Interest-only home loans

– Islamic mortgages

– No cost loans

– No documentation loans

– Option arm mortgages

– Refinance loan

– Reverse mortgages

– Second mortgages

– Stated income mortgages

– Zero down mortgages

Read more: Which mortgage is right for me?

- UWM Launches Borrower-Paid Temporary Buydown for Refinances - July 17, 2025

- Firing Jerome Powell Won’t Benefit Mortgage Rates - July 16, 2025

- Here’s How Your Mortgage Payment Can Go Up Even If It’s Not an ARM - July 15, 2025

Good morning, I purchased my home in 2006 in the height of the market and overpaid for my property. I recently wanted to sell my home and it turns out I still owe more than it’s worth. is there anything I can do to lower my interest rate. I do not and will not refinance at this time, since I have been in there for 9 years and want to sell it in a few years. This harp program is so unfair to a homeowner like me, as I meet the criteria for everything except my loan is not through fannie or Freddie mac. Thanks.

Carol,

If your loan isn’t owned by Fannie/Freddie you could inquire with your servicer about their proprietary loan modification program.

Hello. My husband and I are a young family looking to buy our first home since we recently had our first child. I was wondering if you could maybe suggest some good loans I could look into to help us with this process. My husband is our main source of income and I work here and there but mainly stay home with the baby. I feel like every time we’ve looked at a mortgage we haven’t been able to find something that can help us. Any suggestions would be extremely appreciated. Thank you.

Kayla,

If your husband has good credit a conventional loan will probably be cheaper than an FHA loan. Also, if you can put down 20% you can avoid mortgage insurance, which can be quite costly. It’s a pretty broad question and also dependent on what you guys are looking for, such as fixed vs. variable rate, and so on. Best to do some research as to why you haven’t found something in the past to determine what you can do going forward to get approved. Good luck!

Hello, my fiancé and I are looking into buying our first property, we currently live in an apartment that is going up for sale as a condo, we love this property and location its listed at 292k and we pay 1285 in rent which we have found it just about max in what we can afford with all bills plus the 1285. with credit scores in the high 600 and mid 700 is there a loan we can find that we could afford? Thank you!

Evelyn,

You may want to get pre-approved with a bank/broker to see what you can afford based on all your attributes, such as credit scores, income, assets, and so forth. They’ll be able to give you more exact estimates based on those figures.

Hi Colin,

We are first time home buyers and have already found a house that is bank owned. I have been in contact with one lender but how do I know I am getting an honest, good deal? I know there are a lot of different mortgages, how do I know what is best for us? We do not have a lot of money to put down and we have over a 640 credit score.

Thanks!

Carrie,

You can empower yourself by learning more about mortgages on sites like mine and elsewhere. You can also look at comparable properties on sites like Redfin/Zillow to see what they sell for to ensure you’re not overpaying.

Hello there,

I am recently divorced and am looking to refinance my home. I’d like to avoid paying a PMI if possible. What types of loans can I get to accomplish this other than a VA loan since I’m not a veteran. I purchased my first home over 14yrs ago with a baloon loan, I do understand how this loan works and am not afaid to get another one if this still exists?

Thank you,

Liza

Liza,

To avoid PMI you either put down 20% or you go with a loan that builds PMI into the rate…in other words, slightly higher rate in exchange for no PMI. But the lowest cost option is generally to put 20% down to truly avoid PMI.

Hello,

My boyfriend and I are buying our first home. You always see on the home improvement shows where they have say a $200,000 pre-approval and they buy a house for $100,000. Then they use the rest to fix up the house. Is there a certain score you need or a certain program we could look into? We will be getting a fixer since the area we want to stay in is college town and expensive for anything even slightly nice. Thanks!

Hannah,

There are loans, such as the FHA’s 203k loan, which allow home buyers to finance the purchase and renovation costs in one shot.

Hi. My husband is disabled. He is on disability. He has a bad heart and also cancer. He has a good credit score of 710, I on the other hand have a credit score that is 550 and should be getting better cause I paid some things off. I am a Senior Caregiver. We have as a household about 3k a month. We live in MS. We are trying to get a home, but don’t have any money for a down payment. We bought a factory defective mobile home and that took our savings. We do have a car note that is around 556 a month, but that’s all. Help we need a house quickly. The bank says we are approved for a USDA loan, if the seller agrees to pay the closing. Is that right? We really need advice bad!

Tricia,

A USDA loan does allow for zero down payment and if the monthly payment is low enough, you might be eligible with your income. They are geared toward properties in rural areas, which might include the area in MS where you want to buy. Good luck!

Hello! I loved the information! My husband and I are currently looking for a new home to purchase. He has a credit score that is roughly 650 and mine is 600. Our combined household income is $100,000 annually. Are there any loans that you think we would most likely qualify for?