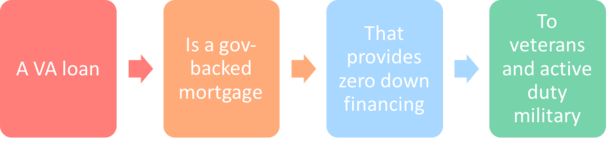

A “VA loan” is a government-backed mortgage guaranteed by the Department of Veterans Affairs (VA) available to both veterans and active duty servicemembers.

The loan program was created all the way back in 1944 and signed into law by then President Franklin D. Roosevelt.

Perhaps the most notable aspect of a VA home loan is its zero down payment requirement, which is also available to surviving spouses.

It’s one of the few places (other than a USDA loan) a prospective homeowner can still buy a property with no money down.

Other options such as conventional loans require 3% down or more, while the FHA requires at least 3.5% down.

The popular loan program, also referred to as the GI Bill, has been highly successful and has helped millions of American veterans and their families purchase a home. Let’s learn more about it.

Jump to VA loan topics:

– VA Loan Eligibility Requirements

– Types of VA Loans

– VA Mortgage Rates

– VA Loan Closing Costs

– Is There a Maximum VA Loan Amount?

– Do VA Loans Require a Minimum Credit Score?

– Pros and Cons of VA Loans

– VA Loan FAQ

– VA Loan Highlights

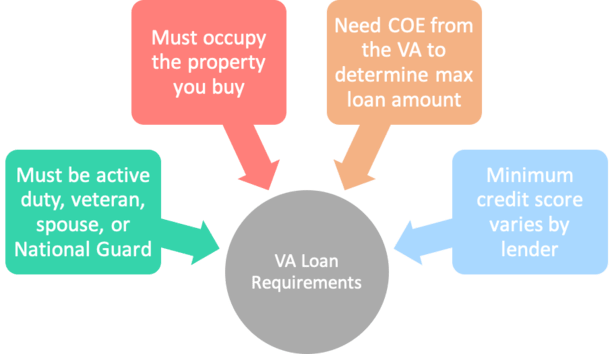

VA Loan Eligibility Requirements

- Must be active duty or veteran in the U.S. Armed Forces

- Or a surviving spouse or member of the National Guard

- Requires Certificate of Eligibility from the VA to determine financing available

- Must occupy property as your primary residence

If you serve (active duty) or served in the Air Force, Army, Coast Guard, Marine Corps, Navy, or the National Guard, you may be eligible for a VA home loan.

VA loans have varying eligibility requirements depending on the duration and type of military service performed.

Veterans who served on active duty for 90 days during wartime, or 181 or more continuous days during peacetime are generally eligible.

There is also a two-year requirement if the veteran enlisted and began service after September 7, 1980 or if the veteran was an officer and began service after October 16, 1981.

Additionally, there is a six year requirement for National Guards and reservists along with other specific criteria.

Un-remarried surviving spouses of a servicemember missing in action or a prisoner of war may also be eligible.

As you can see, it’s quite complicated, so the best way to see if you’re eligible for an VA loan is to visit the Veteran Affairs website, which lists all eligibility criteria.

Now the good news. You can apply for and obtain a VA loan with any bank or mortgage lender that participates in the VA home loan program. And there are lots of them.

So the VA loan application process won’t necessarily be painfully bureaucratic because you’re getting your home loan from a private lender.

Additionally, there are eight VA regional loan centers, known as RLCs, which administer the VA’s Home Loan Guaranty program.

They essentially act as a point of contact for these lenders, and will also field mortgage questions from veterans if you need assistance.

To prove eligibility for a VA mortgage, you will need to get a Certificate of Eligibility (COE) from the VA, which your bank may be able to complete for you. It’s also possible to call your regional loan center, as noted above.

Aside from basic military eligibility, keep in mind that a VA loan must be used for personal occupancy only (no second homes or investment properties), and can only be issued by qualified banks and lenders.

Types of VA Loans Available

- Can get up to 100% financing on a purchase loan or mortgage refinance

- A variety of popular loan types are available

- Including both fixed-rate and adjustable-rate options

- Such as the 30- and 15-year fixed and 5/1 or 7/1 ARM

There are a variety of different VA loan types available for different purposes.

You can get your hands on a VA purchase loan, a VA refinance loan, or a VA streamline refinance.

The streamline option allows borrowers with existing VA loans to lower their interest rate without jumping through eligibility hoops.

Prospective home buyers can borrow up to 100% for a purchase loan without paying private mortgage insurance.

And existing homeowners can borrow up to 100% loan-to-value (LTV) for a rate and term refinance (or 90% for a cash-out refinance).

The streamline VA refinance program, known as an Interest Rate Reduction Refinancing Loan (IRRRL), has no maximum LTV. As the name implies, the mission is to lower the existing payment.

VA loans can be either fixed-rate mortgages or adjustable-rate mortgages, with the 30-year fixed, 15-year fixed, and 5/1 ARM common options.

However, some VA lenders offer 25-year fixed loans, the 20-year fixed, and even a 10-year fixed. More adjustable-rate options may also be available in the form of the 7/1 ARM.

Are VA Loan Rates Lower?

- They tend to be cheaper than most other types of home loans

- But the mortgage rate you receive will depend on your credit profile

- Along with the lender you choose to work with as rates vary by company

- Interest rates anywhere from .25% to .75% lower than non-government rates

One big advantage to VA loans is that mortgage rates are typically cheaper than those on conventional mortgages, though it will vary based on your unique borrowing profile.

In general, you may find that VA loan rates are roughly .25% to .75% lower than conventional rates.

For example, if a conforming loan backed by Fannie Mae ore Freddie Mac is priced at 6.75%, your VA loan might be priced at 6.25%.

So you could wind up with a lower rate and less out-of-pocket expenses, which is certainly helpful for the cash-strapped borrower.

Additionally, VA loans are generally easier to qualify for than other mortgages, though there may be some increased red tape proving eligibility and so forth.

Just keep in mind that a VA funding fee of 0% to 3.3% of the loan amount must be paid, though it can be financed on top of the base loan amount.

Do VA Loans Have Closing Costs?

Like all other mortgages, VA loans have closing costs, which is completely standard and normal. However, the VA does have strict rules when it comes to closing costs. Only certain fees are considered “allowable,” including:

– Loan origination fee (typically 1% of the loan amount)

– Loan discount points (optional to lower your interest rate)

– Credit report

– Appraisal fee

– Hazard insurance and property taxes

– VA funding fee

– Title insurance

– Recording fee

If there are other fees connected to the loan, they cannot be paid by the borrower.

So if it’s a purchase, the former owner could provide seller concessions, the real estate agent could provide a credit, or the bank could provide a lender credit to cover the non-allowable closing costs.

As noted, you are welcome to contact Veteran Affairs if anything seems out of order.

Is There a Maximum Loan Amount on VA Loans?

As of 2020, there is no longer a maximum loan amount for VA loans.

After President Trump signed into law the “Blue Water Navy Vietnam Veterans Act” on June 25th, 2019, the VA did away with its lending cap.

This means those with full entitlement aren’t subject to loan limits like they are on FHA loans or conforming loans.

You have full entitlement if you’ve never used your home loan benefit, have paid a previous VA loan in full and sold the property (full entitlement restored), or you had a foreclosure or short sale in the past and since repaid the VA in full.

However, if you only have remaining entitlement, there are VA loan limits, which vary from county to county.

These VA loan limits are aligned with the conforming loan limit of $806,500 for 2025.

There are also high-cost counties nationwide that go much higher, such as Arlington, Los Angeles, and San Francisco, all at $1,209,750 for one-unit properties.

Borrowers can get loans up to these amounts with no down payment required and a guarantee from the VA if you default on your loan (they’ll pay your lender up to 25% of the loan amount).

Do VA Loans Have a Minimum Credit Score?

- While it’s true that the VA does not require a minimum score

- Lenders typically impose their own minimums to ensure default rates aren’t high

- That means in the real world you might still need a 620 or 640 FICO score

- Though some brave lenders will accept credit scores down to 500

Aside from not needing a down payment, there isn’t a minimum credit score requirement for VA loans.

However, this doesn’t mean you can get a VA loan with a 400 FICO score. Or even a 500 FICO score in most cases.

Many lenders that originate VA loans still impose their own minimum credit score, such as 620, 640, or higher. So it can be somewhat misleading to say they don’t have a minimum requirement.

The VA is happy to say approve any loan you want credit score-wise, but will penalize lenders that exhibit high default rates. As such, VA lenders will take steps to ensure credit quality is in line with industry norms.

That means you probably won’t be able to get a VA loan with a score below 620 in most cases, though there are some lenders will go into the mid-500s or sometimes 500.

However, you should still do your best to stay on top of your credit if you want the lowest mortgage rate possible, regardless of which loan program you choose and whether you can get approved with a lower score.

Sure, you might be approved, but it could cost you big over the years in significantly higher interest costs. Why not take the time to address your credit before applying for a home loan?

[What credit score do I need to get a mortgage?]

Pros and Cons of VA Loans

VA Loan Advantages

- No down payment required

- Low closing costs

- Low mortgage rates

- High loan limits

- Low credit score requirements

- No mortgage insurance

- Available to first-time and repeat home buyers

- Can be assumed by the buyer if you sell your home

VA Loan Disadvantages

- Only available to veterans and active duty

- Can only be used on a primary residence

- More stringent appraisal process

- Upfront funding fee required on all loans

- Not offered by all banks and lenders

- Down payment required if you don’t have full entitlement

As you can see, VA loans come with a number of benefits and advantages that can make them a solid choice above conventional options. And also some drawbacks.

VA Loan Q&A

Where can I get a VA loan?

VA loans are guaranteed by the VA, but actually processed by private banks and independent mortgage lenders nationwide. This means you can go to a local bank, online lender, and so on. Here is a list of the top VA loan lenders.

Do VA loans require a down payment?

No. Perhaps the biggest advantage is the lack of a down payment requirement, which was previously mentioned. You can get VA mortgages for 100% LTV. And per the VA, nearly 90% of all VA-backed home loans are made without a down payment.

Are VA loans only for first time home buyers?

Nope. You can obtain a VA loan as a first-timer or a repeat home buyer. However, you might have limited entitlement if you’ve used VA financing in the past, and thus a down payment may be required on subsequent VA transactions.

Do VA loans require private mortgage insurance?

Finally, VA loans do not require you to pay mortgage insurance, private or otherwise, which can obviously increase the cost of the monthly mortgage payments and the overall cost of your mortgage.

However, the VA does collect an upfront funding fee (unless you’re exempt), which insures your loan against default and protects the originating lender. So in a sense you’re still paying insurance for the loan.

It can be paid at closing or rolled into the loan amount, with the latter option probably being more common.

Do VA loans allow co-signers?

Yes, but it depends on the situation. If the co-signer is your spouse or a veteran, there are no special requirements. But if the co-borrower is not your spouse or a member of the military, a down payment of 12.5% may be needed (this is calculated by using half of the 25% VA guaranty).

Do VA loans cover manufactured homes?

This always seems to be a popular mortgage question, regardless of loan type. The short answer is yes, you can use a VA loan to buy a manufactured home and/or lot. However, the trick is finding a lender out there willing to provide VA financing for a manufactured home.

So it’s a yes according to VA eligibility, but a maybe in terms of finding a lender willing to extend the loan. In short, it might require a bit more legwork to track down someone willing to offer the financing.

Are there VA renovation loans?

Yes. The VA Renovation Loan allows for an all-in-one home loan that covers both the purchase of a property and costs of improvements with no down payment requirement in some cases.

Existing homeowners can also take advantage of the VA Renovation loan by pulling out funds while relying on the as-completed value of the property (appraised value after improvements are made).

While loan amount maximums vary by lender, this type of loan is intended for smaller jobs that don’t involve major work like foundation repairs and so on. All work must be completed within four months of funding.

Do VA loans require an appraisal?

If purchasing a home with a VA loan, an appraisal will be required. This is for your protection too to ensure the home is worth what you’ve agreed to pay for it.

An appraisal is also required if you’re attempting to pull cash out of your home. Conversely, if you’re simply looking to reduce your mortgage rate via an IRRRL, no appraisal is required.

Do VA loans require an escrow account?

The VA does not require lenders to maintain escrow accounts, though most impose them to ensure borrowers have the necessary funds to pay hazard insurance and property taxes in a timely manner.

In other words, the VA doesn’t explicitly require escrow accounts, but the lender you ultimately work with probably will, so there’s not much way around it. Additionally, there is typically a fee to waive escrows, so it might be cheaper just to escrow.

Do VA loans require reserves?

No, VA loans do not require reserves, which is another plus. However, if the property being financed is a multi-unit property and you’re using rental income to qualify, six months PITI will be required for reserves.

Additionally, those with non-traditional or insufficient credit may be required to provide reserves.

Do VA loans have prepayment penalties?

No again. So you don’t have to worry about being penalized for paying off your loan early or refinancing it away from the VA.

In summary, if you feel you meet the eligibility requirements for a VA loan, be sure to include this loan in your mortgage search. You may find that another type of home loan is more beneficial, but you should compare all options to be absolutely certain.

VA Loan Highlights

- No down payment required (100% financing OK)

- No maximum loan amount

- No minimum credit score

- No max DTI ratio

- Assumable

- No mortgage insurance required

- Funding fee can be financed

- Max 1% origination fee

- Limited closing costs

- No prepayment penalties

- Max loan term 30 years

Nice overview. Seems like a no-brainer for someone in the service. Especially since VA lenders probably understand the complex lifestyles of those who serve.

do va loans have pmi that must be paid each month?

Alphonse,

VA loans do not have PMI. PMI stands for private mortgage insurance, and is only applicable to conventional (non-gov) loans.

There’s no mortgage insurance on a VA loan, but there is a funding fee, which varies based on down payment and military category.

Great information. I feel a lot more comfortable applying for a VA loan now thanks to this. Most of my questions were answered, but I’m curious if you know which VA loan fees are tax deductible? Thank you.

Stephany,

As with other types of loans, mortgage points may be tax deductible if expressed as a percentage of the loan amount (and if other conditions are met). Additionally, the VA funding fee is tax deductible and can be fully deducted in the year it was charged. Mortgage interest and property taxes are also deductible if you itemize and meet other requirements. Speak to your CPA to get full details.

Good info Colin! Thanks for taking the time to post this.

can i get a va home loan with a 580 credit score in idaho sent me an email

Mike,

Some lenders are accepting 550 FICO scores for VA now, so as far as credit score is concerned you may qualify. But it depends on the rest of the loan details.

I’m applying for my 2nd VA mortgage (2nd tier), My first will become rental property. Can you confirm I am understanding this properly, my bank didn’t even know 2nd tier existed!

My first home was $92,000 and I used $34,000 of my entitlement. I live in an area where $417,000 is the VA cap. So…

$417,000x 25%=$104,250

$104,250 total available entitlement

$104,250-$34,000=$70,250 remaining entitlement

New house

$189,000×25%= $47,250 needed

So since my used entitlement plus my new required entitlement is less than $104,250 combined and the total value of both homes is less than $417,000, AND the new home is greater than $144,000, I can use 2nd tier correct?

Also, since both homes are single family, would I be required to carry reserves with a 700 score?

Josh,

It looks like the VA guaranty is well above 25% based on your second-tier entitlement and the purchase price, so you shouldn’t need a down payment. And reserves shouldn’t be required based on what you said.

I was told that I could acquire a 0% personal loan for my son’s college education. True?

Ed

Ed,

My guess is no, though some private lenders may offer low or zero introductory rates. Tread carefully. You could also inquire about the VA’s Cash-Out Refinance Loan, but you might want to speak with the Dept. of Veterans Affairs before speaking to any individual lenders.

I have an existing VA loan that was originally financed for 168k 2 years ago in western NC. I was transferred out of state and am currently renting the property which covers the entire payment including insurance and interest. How much of a second tier loan would I be eligible to take. I now live in Blount County TN.

Fred,

Probably best to sit down with a VA loan officer to figure out the specifics.

Thanks.

What is the maximum amount you can have in collections (on your credit) in order to qualify for this type of loan? Or is this even relevant?

p.s Referring to the 2nd tier entitlement

Mary,

VA lenders have different rules regarding collections and whether they need to be paid depending on type, size, date, etc. Probably best to speak to a VA lender for specifics.

Thank you for the interesting and informative article. I do have a question. I took out a VA loan to purchase our house in 2007 (15 yr). I though we were going to retire in MO but now I have a great offer to move to the DC area and are looking to buy a house over there. Of course a $200,000 house here is $500,000 there and I would love to use the VA loan to avoid all the extra expenses (i.e. down payments and PMI). I am not moving for 5 months so could I refinance out of the VA loan through my bank and basically pay off the VA loan so it is available to be used again? I am really not looking forward to renting until we sell our house here and release the VA loan. Thanks

Have never used my G.I./V.A. Home Purchasing Certificate that entitles me to a zero down payment on any house I buy. Now that I am thinking about moving to California, near Oceanside ( where I used ti be stationed) or up in one of the communities in the hills. I need to find out what real estate prices in these communities cost. and how much of would my G.I. Loan cover the cost of buying a home here.

How difficult would it be to get a mortgage using my zero-down V.A. Loan there for a 3-4 bedroom, 3.5.bath, kitchen,Living Room and Study-Office where I would conduct my business from in a gated secure area?

What would my monthly mortgage price be on such a property? Possibly single or two-story dewelling?

WJD.

William,

It depends on the city…the range in property prices in that area of California probably runs the gamut, and a gated neighborhood probably won’t be cheap. Might want to see what you can get approved for before house shopping.

Herschel,

Refinancing might be an option, there’s also the possibility of using second-tier entitlement and keeping the existing VA loan in place. Probably best to speak with a VA specialist to see what route is best to take.

I am in the process of looking for a home. I am looking into the property tax exemptions for my state (Wisconsin) and I am being told I HAVE to roll my property tax payment into my mortgage payment if I use a VA backed loan. Is this true and if so why?

Robby,

Impounds are generally required on all low down payment loans, and since VA loans are no down payment loans in many cases, lenders require you to impound taxes and insurance to ensure you can actually make the required payments each month.

If lenders typically want 20% down, will lenders take into consideration that the VA is covering 25% of $417,000 or $104,250? It seems like I could get a VA loan for up to $521,250 and the lender would be just as protected (521,250×20%=104,250). Is it possible to find a lender that will consider this?

I currently have an IRRL on a rental due to relocation. I am looking to purchase a new home in a higher cost of living area but my certificate of eligibility won’t cover the full cost of the property. Is it possible to use the remaining balance of the VA certificate in conjunction with second fixed private mortgage? Therefore, the main portion of the loan is covered under VA, which would make the second (private) mortgage less costly and I could cover the 20% down payment to avoid PMI.

Have you looked into using the second-tier entitlement?

Brent,

General rule of thumb is that VA guaranty must cover at least 25 percent of the loan, so if the loan limit in the county is $417,000, divide that by 4 to get $104,250 (maximum guaranty), then divide that by $521,250 and it’s only 20%, short of the 25% needed to get a VA loan without a down payment. Probably best to speak with some VA lenders to see what you qualify for.

My husband is a Navy vet. We have a Chapter 7 that was discharged in July 2014. I know we have to wait 2 years from that date. Can we apply before then and not close until after the 2 year mark or do we have to wait the 2 years to even apply? Thanks!

Kim,

Probably have to wait to apply after the two years from discharge date, but best to speak with some VA lenders to be sure.

Don’t bother with a VA Re-Fi unless you like a microscopic financial colonoscopy! Nosiest questions and continual hassles I’ve ever encountered. And then they turned around after the appraisal and REQUIRED that I FIX everything they thought wrong about the house, thousands in repairs, before they’d loan the money. If I had the money I’d not need a loan, right? It makes no sense, but then very little about almost anything VA connected, does.

I’m fed up and going to just get a conventional re-fi.

A few little teeny points or fees won’t matter. Seems like a VA loan is only good for a first time buyer with no down payment, IMO.

My son in law is a vet and trying to buy a home , he has good credit but his wife (daughter) does not have credit or had credit and can not find it on the credit report, what can they do?

Bryan,

Does he need the wife’s income to qualify? Might be able to apply for the mortgage alone if her credit is no good, or ask about alternative credit in place of traditional credit history.

I am currently buying a home with VA and I would like to know are you able to borrow 100% of the appraisal value at the time of closing? ex: buying for 269.000 appraises at 294.000..can the whole amount be borrowed or would you have to do a refi in 6 months?

Julie,

The loan amount should be based on the lower of the purchase price or appraised value.

I have a question? If you currently have a VA loan and are selling and purchasing a new home, are you locked in to your current APR for the VA loan on your new home?

Megan,

If you sell your home the existing mortgage is paid off and you will receive a new loan (with new rate/terms) when financing the new home.

Colin,

This blog is great! However, I served just under two years and I joined in 2007. Does this mean I will not qualify for a home loan?

Kiana,

Best to check your eligibility directly with the VA. Sometimes exceptions to the minimum service requirements.

If I have an awesome credit score, 800+ and a combined family income of 185K what would me funding fee look like for a 215K VA loan when it’s for a second property? I currently carry approx 240K on an existing home.

Gianni,

You’ll need to speak with a lender to figure out the fee. It should be based on down payment amount and military level.

Colin: I purchased my first home, VA loan, in 2001 and had to do a “quick-sale” a year later when my work hours dropped to ten/week. Two years later I joined the service again and retired at twenty years. Am I eligible to take out another mortgage using the VA option or will I have to consider traditional loans? Thanks Chris

Chris,

You may want to contact the VA or a VA lender about your eligibility. You may be able to use second-tier entitlement.

Hi, is it possible to add the money from renting a room in the home i would buy with a va loan to my total income, resulting in a larger loan amount and ultimately a better home? Im a single guy and i plan on buying a home and renting a room to my current roommate, until i meet that someone and start a family and give my buddy the boot. if i could get a future rental contract is that something i could submit to my lender to increase the loan amount ?

Drew,

If it were a 2-unit property and you were renting out one of the units it might fly, but a room in the house is a different story. And as you said, it’d only be a matter of time before you booted your roommate, so a lender can’t rely on that temporary income and give you a bigger loan.

My husband had a VA loan years ago, paid off/home sold and we have recently obtained a new certificate of eligibility showing the full amount restored. Our bank is saying that because the loan has been used once that the terms will be different and not cover as much as a first time user of a VA loan. (Higher interest, etc) Thank you!

Laurie,

You may want to get some second/third opinions from other lenders, but VA funding fees are higher for second use when putting nothing down.

Are vets still allowed to take secondary loans to pay for their closing costs? Specifically, are they still allowed to obtain unsecured installment loans, or even use credit cards, to pay for their closing costs? I have done loans that way, but not for some time. What had always been required was to disclose such new debts, verify balance and payment, and include any payment in DTI.

My daughter has been in the Air Force for 6 months, she wants to buy a house. Can she say she will be renting the basement out to me to boost her income up for a larger loan amount?

Dawn,

Generally future rental income can’t be used to qualify for a mortgage unless it’s a multi-unit property (like a duplex) and the buyer has landlord experience.

What is the maximum loan term (period) a VA loan can have?

Pooja,

30 years. Technically up to 30 years and 32 days.

I am doing a family member’s taxes and they were charged $3770 in PMI on their VA loan. At least this is the box that it is in on their 1098. When we called them they said that was just the price for doing the loan. I can’t deduct it as PMI, because of their AGI being too high. Is it possible for them move it to a different box since it really isn’t PMI??

Liz,

Probably best to ask a CPA/tax specialist.

Does adding the funding fee into a VA home loan which puts it over the limit of 417,000., does that make it a jumbo loan?

Purchase price of home=415,000.+ funding fee=9,130.=loan amount of $424,130.

Thank You

Ken,

I’ve seen it both ways…some lenders say max loan amount is $417,000 including financed funding fee, whereas others state maximum loan amount is $417,000 plus VA funding fee. Probably best to ask specific lender you’re working with.

Why is the IRS treating my VA Funding Fee as a PMI and not giving me deduction because my AGI is over 109k?

IRS Publication 936 specifically states:

“You can treat amounts you paid during 2015 for

qualified mortgage insurance as home mortgage

interest. The insurance must be in connection

with home acquisition debt, and the insurance

contract must have been issued after

2006.”

VA does not require PMI but you do have to pay their funding fee.

So frustrating!!!

Michele,

Unfortunately there are limits on certain deductions but it might be wise to go over these details with your tax preparer or CPA to be sure.

Good Evening,My brother and I are trying to buy a home together at home.(Orlando where we have lived with our mom) My mom will soon be selling her home,and we would like to purchase a new home and that way our mother and sisters can stay there and we keep our “home base” Orlando. Is there a way we could do it together? or will it be considered an investment property and we couldn’t do a VA loan.

Anjellica,

If you both intend to occupy the property as your primary residence you might be able to go the co-borrower route.

My wife and I are both veterans and trying to purchase a home priced at $580,000. The maximum loan amount in the area is $417,000. I have used my entitlement before but have $57,250 remaining. My wife on the other hand has never used her entitlement so has it in full. We would like to have my wife as the primary borrower and use her full entitlement then use my remaining entitlement for the difference to reduce the required down payment. It is our understanding based on our research that VA will require a down payment of $40,750 based on our situation. We would like to use my remaining entitlement to cover the difference. Do you know if this is allowed or how this would be handled?

Hey Troy,

May be best to get with some VA lenders to determine the best structure for your situation.

Hello Troy,

There are plenty of options for people in your position.

Feel free to shoot me an email to set up a time to go over some of the options that you have regarding the different loan products available.

Hey Troy,

I own land and want to put a manufactured home on it and wanted to know can I use my VA loan to pay for driveway, garage and fencing for the house as well. Kind of do a bundle loan?

I’m using my VA loan for a purchase (in CA) and the lender lied to me saying it was under review with the VA 10 days before it actually was. Now I’m late to close escrow and the seller is trying to charge me $100 per day until we close. Can they charge that on a VA loan? Thank you

Dave,

Maybe your lender can give you a credit (since they lied) to cover the per diem interest requested by the seller.

Bret,

You may want to inquire with some VA lenders about a one time close construction-to-permanent loan to get all your financing in one shot.

I bought a home on a VA loan and not even 3 years later, I have structural damage. Had an inspector come out and he said $30K to repair. I thought the VA is supposed to protect the homeowner? He said house not up to code. Floors sagging, not enough support, moisture in crawlspace, fungus on wood causing soft rot…. My real question is isn’t the VA appraiser supposed to identify structural damage? I did not have a home inspection done at time of purchase because I was under the assumption that VA would be inspecting. My brother has bought several houses in Florida & VA always required a home inspection. My home is in Mobile, AL. Not sure what they require here. But I’m thinking of sueing the VA. So you have any info or know a good lawyer? Thanks

Very helpful overview, Thank you~ I might have missed it, but can you get VA loan, that you would other wise qualify for, if you had a bankruptcy over 3 years ago, but a foreclosure less than 3 yrs. ago?

Candice,

Generally it’s two years since those events to qualify for a VA loan, assuming you meet all other VA requirements and have remaining entitlement.

I applied for a VA cash out loan through my bank. It’s close to 800k so the bank told me another bank “broker” is underwriting the loan. Now my bank said ” the loan is with the VA for some exceptions”. I thought the VA was a insurance policy only and they do not make decisions like that, especially since they are not going to service the loan. Is it possible for my loan to be ” at the VA for review and exception?” Thanks

Casey,

They might mean the underwriter is communicating with the investor of the loan to iron out some details to ensure it’s saleable.

I want to re-finance my house to lower payments. It’s worth $350,000 and I owe $150,000. I only want a loan for the balance. The problem is that we have had unexpected expenses this year and have had late payments. I was told that we are not eligible because of the late payments. I have paid 11 years on the loan and because of the recent late payments I can’t get help?

Joy,

Most lenders won’t issue you a mortgage if you’ve had multiple recent late payments. While it sounds like a harsh penalty to pay, they just see it as too risky. However, some specialty lenders out there might be willing to offer financing, but if they do, it’ll likely be with less favorable terms. Still, if your current interest rate is high, it could still benefit you. May want to shop around and/or enlist a broker to see if one of these types of lenders will help you, or if you can get granted an exception. Good luck!

We are looking at a VA loan to do refi our first and do a debt consolidation using the equity of that loan. We have a HELOC as well that is maxed out at 126k and is used as our second. Will our HELOC HAVE to become our first because the bank financing that HELOC feels us pulling cash from our first as too risky? In other words, is it required to become our first and then the new VA refi loan become our second??

Can a VA loan be recast?

Ricardo,

If part of a loan modification then potentially.

I would like to have my VA loan reviewed for corrective action regarding the fees charged. How do I request this?

My refinance was completed 3 months ago (November) and I have not received the escrow refund (they took out extra due to the timing of paying taxes). The old company refunded their escrow but the new company is holding on to what they took out as a just in case amount

Why do I need to wait 1 year from the sale of my home (FHA Loan) to utilize a VA loan?

If I have 10 conventional (non-VA) Fannie Mae mortgages on investment duplexes can I still get a VA loan for my primary residence?

If I own 12 or more duplexes (not in an LLC) can I still get a VA loan for my primary residence?

Does a newly constructed home have to be completely finished by the builder to qualify for a VA mortgage, or can the basement be left unfinished?

If you sell your house and the buyer wants you to keep the loan in your name because of a low interest rate. Are you violating the VA contract and what would the VA do?

Lyle,

Not sure that would fly because the seller would be on the hook for any missed payments and the loan would remain on their credit report. If buyer wants to assume the loan because of the low rate, which may not even make sense because rates are near all-time lows today, it would likely need to be transferred into the buyer’s name after they qualify for the loan.

I sold my house with a VA loan but they requested that I keep it in my name and now I’m being informed that I’m in violation of contract?? What happens if the lender finds out?

Is it normal to not get a difference between 15 year and 30 year rate? Do mortgage companies get more money for 30 Year VA Loans?

Aaron,

The 15-year should definitely price below the 30-year, though the spread can widen and shrink over time. Things are weird at the moment, but you should still see a discount on the 15-year.

I have a 2014 conventional cash-out refinance loan…I’m attempting to get a VA refinance. The lender is saying I can’t in the state of Texas! I’m not trying to do a cash out now. I can never do a VA loan again????

Robert,

Texas has restrictions on VA cash out loans, though you noted your conventional to VA refinance would be rate and term. Did you ask them why specifically it can’t be done? Perhaps you can’t streamline it, but a traditional refinance still works?

If someone assumes a VA loan and doesn’t make the payments will the original owner be liable for the payments?

Elizabeth,

Good question – you’d want to get some sort of release from liability from the VA, and you’d also have to consider the entitlement too if that’s also tied up by the assumption.

ok first I am a 100% rated disabled veteran. My mother is now my dependent because of problems mentally that are slowly coming about. She watched the love of her life wither away for nine months. She did not pay taxes for two years nor the mortgage from the first week he was diagnosed with pancreatic cancer until today. To start this complex question you needed to know that. It starts…. my mother got a mortgage and when she was almost done with paying it off she then refinanced. Then she wound up messing that up and then messing the modified mortgage up too due to the company her and pop had was failing. I made a call and I got her a re-mod on the re-mod. The bank said they would hold the foreclosure over her head but they never went through with it due to the lenders switching three times and confusion. Now we got a letter in the mail stating “satisfaction of mortgage” and that the mortgage was paid in full and will be fully removed from record. We did not pay this and I want to know what is going on here. How is this possible.. Also with the couple of years of not paying taxes we got a letter from the town saying we are hereby notified of the pending sale of a tax lien against the property described below. I am not on the deed but I have power of attorney over everything of hers because of her mental deterioration that has started. I did not know anything about the taxes. Plus the big question is how is the deed paid off and whats going on? Please advise.