Trulia releases a quarterly Rent Versus Buy report to determine if it makes more sense to buy a home or continue renting based on current metrics.

Their latest report for the third quarter of 2014 revealed that buying is still 38% cheaper than renting nationally, which sounds pretty compelling. It’s also cheaper to buy than rent in the 100 largest metros nationwide.

It’s better to buy now than it was a year ago (35% cheaper) because mortgage rates have moved lower and rents have climbed higher.

However, they use some assumptions to come up with their calculations, including a 30-year fixed rate mortgage as the loan type and 20% as the down payment amount.

In reality, many individuals these days put down a lot less and/or go with a different type of loan. So when determining if you should buy or rent, make sure you consider all the details, not just the home price in your desired area.

For the record, Trulia also assumes that you’ll stay in your home for seven years and itemize your taxes to take advantage of the mortgage interest deduction. Oh, and that you’re in the 25% tax bracket.

If you truly want to get an accurate apples-to-apples comparison, you must consider all of these factors before diving in. Otherwise you could be in for a nasty surprise.

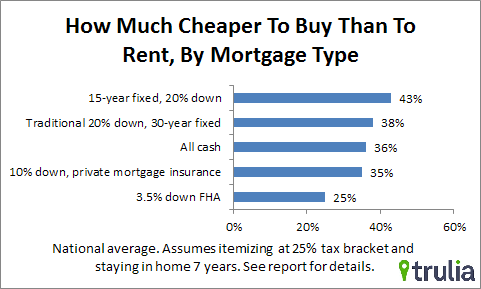

Mortgage Type Matters Beyond the Mortgage Payment

When people consider what type of mortgage to get, they probably look mainly at the monthly payment.

For some, it’s probably not even a decision that needs to be made. They simply can’t afford anything other than a 30-year fixed, assuming they’re in an expensive market like Los Angeles or San Francisco.

But if you do have a choice, consider how it sways the decision to buy vs. rent.

The baseline assumption results in a 38% advantage to buy vs. rent, using a 30-year fixed and 20% down payment.

However, if you go with a 15-year fixed instead, the buying advantage jumps to 43%. This is due mainly to the fact that you’ll pay a lot less interest and gain a lot more equity faster.

[15-year mortgage vs. 30-year mortgage]

However, the payment is also a lot higher, so as mentioned, it’s not even an option for many people. And not everyone is interested in paying off their mortgage faster because they believe there are better places to put their money.

If we consider the opposite direction, a 3.5% down FHA loan pushes the buying advantage down to just 25% because you pay a lot more interest, not to mention costly mortgage insurance.

But if you can muster 10% down and pay PMI instead, the buying advantage jumps back to 35%, not far from the baseline scenario.

Interestingly, buying a house with all cash isn’t as favorable as one would think. The advantage drops to 36% because you lose the tax deduction. Additionally, Trulia assumes a 3.5% return rate for your money.

I’m sure many individuals could do better than that if they have the cash to buy a home outright, but it is something to consider if you do have sizable assets.

These are just some of the scenarios Trulia highlighted. There are also seemingly common cases where renting makes more sense buying.

For example, if someone goes with an FHA loan and doesn’t make enough to itemize taxes (very possible), and only stays in the house for five years, buying becomes more costly than renting in 27 of the nation’s 100 largest metros.

So be sure to really dig in to your personal situation and future plans when determining what’s the right move.