The “debt-to-income ratio” or “DTI ratio” as it’s known in the mortgage industry, is the way a bank or lender determines what you can afford in the way of a mortgage payment.

By dividing all of your monthly liabilities (including the proposed housing payment) by your gross monthly income, they come up with a percentage. This key figure is known as your DTI, and must fall under a certain number in order to qualify for a mortgage.

The maximum debt-to-income ratio will vary by mortgage lender, loan program, and investor, but the number generally ranges between 40-50%.

Update: Thanks to the new Qualified Mortgage rule, most mortgages have a maximum back-end DTI ratio of 43%. However, there is a temporary exemption for many loans, but a lot of lenders still want this number to be under 43%!

Jump to DTI topics:

– Front-End and Back-End Debt-to-Income Ratios

– Max DTI for Conforming Loans

– Max DTI Ratio for FHA Loans

– Max DTI Ratio for VA Loans

– Max DTI Ratio for USDA Loans

– How to Calculate Your DTI Ratio

– What’s Included in the Debt-to-Income Ratio

– What’s Not Included in Your DTI

– What Is a Good Debt-to-Income Ratio?

– Stated Income to Avoid Debt-to-Income Ratio Problems

– Qualifying Rate for Debt-to-Income Ratio

Let’s look at a basic example of the debt-to-income ratio:

- Annual gross income (as reported on your tax returns/W-2 form): $120,000

- Monthly gross income: $10,000

- Monthly liabilities: $3,500

- 35% debt-to-income ratio

In this example, your debt-to-income ratio would be 35% ($3,500/$10,000). Pretty simple, right?

Well, before you think you’re done calculating your DTI, you should know that the debt-to-income ratio goes into greater detail and comes up with two separate percentages.

One for all of your monthly liabilities divided by your gross monthly income (back-end DTI ratio), and one for just your proposed monthly housing expense (including taxes and insurance) divided by income (front-end DTI ratio).

Front-End and Back-End Debt-to-Income Ratios

- There are actually two DTI ratios

- One for the front-end (your proposed housing payment)

- And another for the back-end (that includes all monthly debts)

- Some lenders may require you to stay below both limits

In the example above, if your proposed monthly housing payment makes up $2,000 of your $3,500 in monthly liabilities, your front-end DTI ratio would be 20%, and your back-end DTI ratio would be 35%.

Some banks and lenders require both numbers to fall under a certain percentage, though the back-end DTI ratio is more important since it considers all your monthly debts, and is thus more representative of the risk you present to the lender.

You may see a debt-to-income requirement of say 30/45. Using our same example, your front-end DTI ratio of 20% for the housing expense only would be 10% below the 30% limit, and your back-end DTI ratio of 35% would also have 10% clearance, allowing you to qualify for the loan program, at least as far as income is concerned.

*If you own other property with a mortgage, it should be included in the back-end DTI ratio because it’s not part of the new loan you are applying for.

Max DTI for Conforming Loans (Fannie Mae and Freddie Mac)

- Historic max is 28/36

- Fannie and Freddie allow up to 43% DTI

- But may go as high as 45-50% with compensating factors

- And only 36% if it’s a manual underwrite

The classic, “rule of thumb” ratios are 28/36, meaning your front-end ratio shouldn’t exceed 28%, and your back-end ratio shouldn’t exceed 36%.

To calculate the 28/36 rule, simply multiply your monthly gross income by 0.28, then by 0.36.

If you make $10,000 per month, that’d give you a max housing liability of $2,800 and a max total liability of $3,600.

However, this measure is more conservative than what you might actually see in practice today. For example, back in the day many homeowners put down 20%. Today, the down payments are often just 3-10%, to give you some perspective.

But, Fannie Mae still does impose a max DTI of 36% for manually underwritten loans, though the majority of loans are approved via their automated underwriting system called Desktop Underwriter (DU).

And DU will allow DTIs up to 45%, and as high as 50% with compensating factors, such as plentiful assets, larger down payment, great credit, etc.

In other words, you can bend the rules a little bit if you’re a good borrower otherwise. But if you have bad credit and nothing in your savings account, don’t expect any favors in the DTI department.

For Freddie Mac, underwriters must include a written explanation that justifies exceeding the 28/36 ratios when files are manually underwritten. Like Fannie, the ratios may go higher if the file is approved via automated underwriting.

Max DTI Ratio for FHA Loans

- General guideline is max ratios of 31/43

- Though it can potentially be much higher

- Based on the findings from an automated underwrite

- Potentially as high as 55% (or even higher case-by-case)

The max DTI for FHA loans depends on both the lender and if it’s automatically or manually underwritten.

Some lenders will allow whatever the AUS (Automated Underwriting System) allows, though some lenders have overlays that limit the DTI to a certain number, say 55%.

These limits can also be reduced if your credit score is below a certain threshold, such as below 620, a key credit score cutoff.

For manually underwritten loans, the max debt ratios are 31/43. However, for borrowers who qualify under the FHA’s Energy Efficient Homes (EEH), “stretch ratios” of 33/45 are used.

So if you make $6,000 per month, you’d have a max housing liability of $1,860 and a max total liability of $2,580 with the 31/43 rule in place.

These limits can be even higher if the borrower has compensating factors, such as a large down payment, accumulated savings, solid credit history, potential for increased earnings, a minimal housing expense increase (no payment shock), and so on.

This is yet another reason to build credit and save up money before applying for a mortgage!

To sum it up, if you can prove to the lender that you’re a stronger borrower than your high DTI ratio lets on, you might be able to get away with it. Just note that this risk appetite will vary by mortgage lender.

Also note that mortgage insurance premiums are included in these figures.

Max DTI Ratio for VA Loans

- VA states 41% is max acceptable DTI

- And 41% max without compensating factors is likely the limit

- Possible to get approved with DTI between 41-50% with compensating factors

- Or even higher in certain cases with exception

For VA loans, the same automated/manual UW rules apply. If you get an AUS approval, the maximum DTI ratio can be quite high.

However, if it’s manually underwritten then the maximum debt-to-income ratio is 41% (back-end). There is no front-end debt ratio requirement for VA loans.

So if make $5,000 per month, your max housing liability would be $2,050 using the 41% DTI rule.

Again, as with FHA loans, if you have compensating factors and the lender allows it, you can exceed the 41% threshold and enjoy higher DTI limits.

Specifically, if your residual income is 120% of the acceptable limit for your geography, the 41% DTI limit can be exceeded, so long as the lender gives you the go-ahead.

In other words, most of these limits aren’t set in stone, assuming you’re a sound borrower otherwise.

Max DTI Ratio for USDA Loans

- Generally set at 29/41 max

- But automated underwriting may allow higher limits

- Such as 32/44 max with compensating factors

- And minimum credit cores of 680

For USDA loans, the max DTI ratios are set at 29/41.

So for a home buyer making $4,000 per month, they’d be looking at a max housing liability of $1,160 and max total liability of $1,640.

However, if the loan is approved via the Guaranteed Underwriting System (GUS), these ratios can be exceeded somewhat, similar to FHA/VA loans.

If the loan is manually underwritten, the limits may be exceeded if loan is eligible for a debt ratio waiver.

Long story short, if you have a credit score of 680 or higher, solid employment history, and the potential for increased earnings in the future, you may get approved for a USDA loan with higher qualifying ratios. But they’re still pretty strict.

How to Calculate Your DTI Ratio

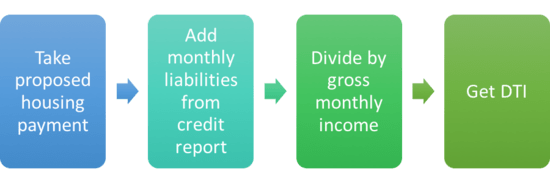

- Take your gross monthly income (e.g. $5,000)

- Then divide it by your proposed housing payment (e.g. $2,000)

- And then add your proposed housing payment and monthly liabilities

- To get both the front-end and back-end DTI ratios

If you’d like to figure out your debt-to-income ratio, simply take your average gross annual income based on your last two tax returns and divide it by 12 (months).

So if you made on average $100,000 gross (before taxes) each year for the past two years, that would equate to $8,333 per month in income.

Next, add up all your monthly liabilities and your proposed housing payment (including taxes, insurance, HOA if applicable) and divide that total by your monthly income and voila.

For that proposed housing payment, you can use my mortgage payment calculator to get the P&I payment. Then gather the insurance, taxes, and other costs from each source for an accurate estimate.

When I say liabilities, I mean all the minimum payments that appear on your credit report. Bills that don’t show up on your credit report generally aren’t counted toward your debt-to-income ratio because they aren’t credit-related and/or documented.

For example, health insurance premiums, a cell phone bill, cable bill, gardening bill, gym membership, or a pool service may not figure into your DTI. This is a good thing if you’re cutting it close.

Keep in mind that you’ll need a free credit report to accurately see what all your monthly payments are. Fortunately, these are very easy to come by these days.

A credit report will show you what your minimum or monthly payment is for each tradeline listed, which makes it simple to add them up.

Typical monthly costs included in the debt-to-income ratio:

- credit card payments

- student loans

- auto loan/leases

- personal loans

- alimony

- child support

- mortgage loans and home equity loans on other properties you own

- housing costs on subject property including homeowners insurance, mortgage insurance, property tax, HOA dues

All the above count against your income, so if you can eliminate or reduce these debts, your income go will further in terms of what you’re able to afford.

When it comes to plastic, the minimum credit card payment listed on your credit report will be considered. All the more reason to apply for a mortgage when all your credit cards are paid off, with no new charges, if practical.

Some banks and lenders allow installment (charge) credit cards such as those issued by American Express to be excluded from the debt-to-income ratio as they often account for thousands of dollars a month, and likely get paid off in full monthly.

What’s Not Included in Your DTI

- Car insurance premiums

- Health insurance premiums

- Cell phone bills

- Cable bills

- Gardening bills

- Pool cleaning bills

- Maid service and so on

At the same time, a lot of items aren’t included in your debt-to-income ratio. Examples include car insurance, health insurance, and various monthly expenses like cell phone bills and cable bills.

Additionally, stuff like a monthly pool cleaning bill or gardening bill likely won’t be included.

This isn’t a sure thing, but generally this type of stuff isn’t included in your debt-to-income ratio, though it might already be factored in because the DTI limits assume you have these other expenses.

That’s why lenders don’t allow DTI ratios up to 100% – there’s a big buffer to account for these everyday expenses we all incur.

Anyway, let’s assume you’ve got $1,000 in monthly liabilities on your credit report thanks to some credit cards and a car loan, and a proposed housing payment of $2,000, including insurance and taxes. If we combine those two figures, we come up with $3,000.

Now simply take that $3,000 in monthly debt and divide it by our original monthly income figure of $8,333. That gives us a debt to income ratio of 36%. This number is below the maximum and should be sufficient to get a mortgage, as long as you qualify otherwise.

By the way, the front-end debt to income ratio would be 24%, which is $2,000 divided by $8,333.

The debt-to-income ratio is a great way to find out how much house you can afford, as well as the maximum mortgage payment you qualify for. Simply add up all your liabilities and your proposed mortgage payment plus taxes and insurance to see what type of loan you can take out.

Obviously, you’ll need to take a gander at current mortgage rates and then plug your loan amount into a mortgage calculator to find that proposed payment, and then do your best to ballpark insurance and taxes.

If you want extra credit, get insurance quotes early on and visit your tax assessor’s website to fine-tune those numbers.

You’ll probably want to err on the side of caution and round everything up, including the mortgage rate, to ensure you’re not calculating your DTI too liberally.

What Is a Good Debt-to-Income Ratio?

- The lower the better

- Which is the opposite of credit scoring

- But as long as you’re below the max

- It shouldn’t affect your home loan application

Unlike a credit score, where higher is better, a good debt-to-income ratio for a mortgage is one that is low.

If you’re weighing the rent vs buy question and/or looking at properties to purchase, you should definitely know your DTI ratio well in advance to fine-tune your search.

But like credit scores, which stop benefiting you at a certain level, there’s a point where it doesn’t matter how low your DTI is either.

Really, you just want/need it to be below the key thresholds listed above. As long as you’re below those numbers, you’re “good.”

So just focus on being below the maximum ratios and you’ll have a good shot at getting approved for a mortgage, assuming you meet the other qualifying criteria for things like credit history, assets, and so forth.

As noted, it’s nice to have a buffer in case mortgage rates increase from application to funding, or if any monthly debt was left out or underestimated in error.

Tip: If your DTI is too high, you might be able to lower it by putting more money down and/or buying down your interest rate, both of which will reduce the monthly payment. So there are always options if you take a wrong turn!

Stated Income to Avoid Debt-to-Income Ratio Problems

- For those who have trouble meeting DTI ratio requirements

- A stated income loan could come in handy

- But expect a higher interest rate as a result

- And be prepared to document a significant amount of assets

It’s also possible to go the stated income route if you feel you won’t qualify for the loan based on your gross income alone. But unlike the liar’s loans of the early 2000s, today’s stated loans rely on a healthy stable of assets to offset any income shortcomings.

One such example is a bank statement loan, which calculates income by using bank deposit history over a certain period of time. So you still need to have lots of money in the bank to get a mortgage.

If you find yourself in this situation, mortgage brokers can be helpful because they work with a variety of banks and lenders, including specialty lenders. The big retail banks may not be able to accommodate you.

Before the crisis, pretty much every bank and lender offer reduced documentation loans such as SIVA (stated income, verified assets) loans and No Ratio loans (no income, verified assets), and very few borrowers actually documented their income. Those days have come and gone.

Many people think reduced-doc loans are just stretching the truth, but they can also come in handy for borrowers who have increased their gross income recently, or those with complicated tax schedules, usually self-employed borrowers.

Qualifying Rate for Debt-to-Income Ratio

- Pay attention to the qualifying rate used by the lender

- Which could differ from the note rate on the loan

- If you apply for an adjustable-rate mortgage

- You might be required to qualify at a higher interest rate to account for future rate adjustments

One important thing to keep in mind is the qualifying rate banks and mortgage lenders use to come up with your debt-to-income ratio.

Many borrowers may think that their start rate or minimum payment is their qualifying rate, but most banks and lenders will always qualify the borrower at a higher interest rate to ensure the borrower can handle a larger amount of debt in the future assuming payments rise.

For example, a borrower may be in an adjustable-rate mortgage with a monthly payment of only $1,000, but their fully-indexed payment could quite a bit higher, say $1,500, after the fixed period ends.

For a bank or lender to effectively gauge the borrower’s ability to handle debt, especially once the minimum payment is no longer available for the borrower, the lender must qualify the borrower at the higher of the two payments.

This gives the lender security and prevents under-qualified borrowers from getting their hands on mortgages they can’t really afford.

Borrowers should also note that most debt cannot be paid off to qualify. If you have debt on credit cards or other revolving accounts and plan to pay them off with your new loan, the monthly payments will likely still be factored into your DTI.

This prevents a borrower from refinancing their mortgage or buying a new home and piling all their outstanding debt on top of the mortgage, just to rack up more debt on those cards a month later.

It also allows the bank or lender to gain a true measure of a borrower’s ability to handle debt. However, lenders will usually allow borrowers to pay off installment debt to qualify so long as they have sufficient, verified assets.

But as mentioned earlier, it’s better to apply for a mortgage when you don’t have a lot of outstanding debt. Aside from be able to qualify for a larger loan amount, your credit scores will probably be higher as a result, which can land you a lower rate!

You can download my Excel-based Debt-to-Income Ratio calculator below to figure out what you can afford: Debt-to-Income Ratio Calculator. Or check out similar loan calculators on the web if you need help with your DTI calculation. I also have a web-based mortgage affordability calculator that may help.

Read more: Do I qualify for a mortgage?

Are lenders allowed to charge more for higher DTI ratios?

Yes, certain lenders may add adjustments to fee for DTI ratios between a certain percent, or above a certain percent. So if your DTI is above 50%, they might charge .50% as an adjustment to account for what they see as higher risk. And if your DTI is between say 45.01-50%, they might charge something like .25%.

I’m considering making an offer on a home this spring. What steps can I take to lower my debt to income ratio over the next couple months?

Are deferred student loan payments included in the DTI ratio for a mortgage? I’m wondering because I don’t need to start paying back my loan until 2015.

Curtis,

Basically reducing your outstanding debt is the name of the game if you want to lower your DTI. That means paying down credit card balances, auto loans, etc, and avoiding opening new lines of credit. The less you owe, the smaller your monthly obligations will be. It could also boost your credit score. Just be sure not to deplete your assets in the process.

For conventional loans, deferred student loan payments must be included in the DTI. However, for FHA/VA lending, student loans deferred more than a year (12 months) after loan closing can be omitted from the DTI calculation.

I have approached the refi process over the past six months several times to no avail. I have been turned down because my dti 48-50%. I am on a fixed income and retired. I desperately need to refi and believe I can managed the extra $200-300 a month vs. the debt repayment of $1000 I have now. Who will help me refi?

Margaret,

Have you tried brokers or just individual banks? A broker will be able to shop you with a slew of lenders at once to find someone that specializes in higher DTI and fixed income.

My current front end DTI is .28%

My back end is .478%

What’s the chances of myself getting a loan

Jeremy,

Your chances will be a lot better if you can get below 43% because that’s the new Qualified Mortgage cutoff. So if you have large monthly debt payments, perhaps paying off those can lower it, or putting more money down/finding a cheaper house. But there should still be options if your overall credit profile is good. Shop around to see what’s out there.

My current front end DTI is 21%

My back end is 21%

What are the chances of my getting a loan with these percentages and a credit score in the mid 600?

Melissa,

Your DTI and credit score shouldn’t hinder you, though you could work to improve your credit score for more options and more favorable pricing. And are you including a future mortgage payment in your back-end number? The rule of thumb nowadays is to stay below 43% to avoid extra scrutiny.

Hi,

we are looking at buying a new house in an area that we really like. This house is on the market for 1M. Our current house is paid off and its worth approx. 400,000. I plan on putting all of the 400k as down payment. We have zero debt (no car payments, no CC payments, etc..). Credit score in the upper 800s. My question is this: I’m concerned that the DTI may be looked as too high showing an annual salary of $110,000. Do you think we will have difficulty qualifying for a loan.

Kal,

The $400k down payment and zero debt will certainly help your cause, but you also have to consider taxes on the $1 million property, homeowners insurance, etc. It could be close to some lenders’ cutoffs but you should use a calculator/get pre-qualified or pre-approved to be sure you’re factoring in everything properly.

I am confused about the front end dti ratio you figured in the above example. How did you get 20% front end with 2000.00 mortgage and 3500.00 in debt?

Thanks

Joy,

The example assumes $10,000 in income, so $2,000 going toward housing costs would be 20% of that $10,000. The $3,500 is the total monthly debt including housing, making the back-end DTI 35% based on that $10,000.

Colin –

I just finished your great article on DTI. Thanks for posting. But I am curious if my situation is unique and wanted to ask your opinion.

We have zero current debt and a gross household income of $235,000/yr. A conservative front end ratio limits us to roughly $900,000 purchase price, while an aggressive back end ratio might qualify us for $1,400,000. That’s a big difference between the two, and I doubt we will ever accrue other debts (just as a matter of personal preference/philosophy).

Do you think we’d ever qualify for something more than the front-end ratio ?

If you have time to give some quick input, it would be sincerely appreciated. Thanks.

Hey GB,

It depends on the lender’s risk appetite, as you’ll be in the jumbo loan realm where DTI maximums vary quite a bit. I’ve heard of lenders that allow the max DTI ratios to be the same for front- and back-end, but others that limit the front-end ratios significantly. Even if you say you won’t accrue other debt in the future, there’s no absolute guarantee you won’t. So approving a loan with a very high front-end DTI can be risky. It might be wise to get a pre-approval with a bank or two to see what you can truly afford based on their maximum qualifying ratios, then shop for a property from there, seeing that there’s quite a range in your situation.

I get the back-end ratio, as a bank wouldn’t want to lend to a borrower who’s too leveraged.

But the front-end ratio seems arbitrary. I have no other debt. If a 40% back-end DTI is okay, why can’t I allocate all my debt to my house?

Jared,

Imagine after taking out a mortgage that you take on other non-housing related debt…all of a sudden your high front-end ratio becomes a problem because you’ve compounded it with a bunch of other debt. Once you own a home you might need to apply for more credit for things like repairs, maintenance, furnishings, etc. And the lender has no control over what you do after you get your mortgage.

Do 5% down conventional loans ever allow for more than 36% DTI? My only debt is student loan debt. I am not interested in FHA.

Bob,

Fannie and Freddie allow DTIs up to 45%, or even higher with strong compensating factors, but the outcome may depend on your loan/borrower attributes and the lender’s own policies.

I recently inherited property and need to refi. I’m married and currently have a mortgage with my husband in our primary residence. Trying to refi the inherited property as sole borrower, which would be considered an investment property. My broker is telling me that my DTI is too high due since the calculation is using the entire amount of my residence mortgage. Is there a way to only have half of that considered, since the that loan was based on our joint income and co borrowers?

Candy,

Sometimes the existing mortgage can be excluded from your DTI if you can show (with cancelled checks or some other proof) that the co-borrower has been consistently making all the payments on their own. If you’re not far off DTI-wise is it possible to go with a smaller loan amount to get that number down?

my DTI is 63% I am self employed. I did not take a salary this year that’s why my DTI is so high. I could kick myself for this…live and learn….. are there any lenders out there that will do a cash out refi with that 63% or a line of credit? my credit score is 775, my spouse is 733.

Thanks

Nick,

Maybe speak with an experienced mortgage broker (or two) to see if they can work something out for your situation.

I’m self employed and 2013 showed my lowest income in the last 5 or more years. However last year was great. The problem is the average of the two fictionally lowers my DTI to around 50%. On last year alone (and all the years before that) I am well within the allowable 43%. What can I do to refi? I have a non-FHA loan and wan to take advantage of the record low rates. My credit score is excellent. Im really frustrated that I cannot get into a premium product because of a fiction on paper.

Some lenders still offer loans with DTI ratios above 43%, though it is less common thanks to the QM rule.

We are in a interest only loan which is going to convert this August and are looking to refinance. I recently took on a second job (last month) as well as received a raise on my first job. How long will I need to wait before applying for a mortgage refinance. Will banks take only one month of pay stubs to verify my income. I fear that if they only look at our past two years of taxes we won’t qualify. Combined between myself and my husband we’ll make $100,000 and need to refinance a $517,000 loan. We have no debts great credit and our DTI is 36%.

Heather,

Lenders generally ask for your two most recent pay stubs along with your two years of tax returns. They do so to ensure income is stable and predictable. A broker could be helpful to shop with a variety of lenders all at once to find some possible options for you.

If your student loans are in deferment when applying for a housing loan, how exactly do you add that to your monthly debt?? When the loans are no longer in deferment I have no idea how much I will be required to pay monthly.

We are currently looking at a VA Loan. I am self employed, have a credit score of 794, will be putting down 40 thousand on a 315 thousand dollar home, and will be paying off all other debts.

The obvious problem is that what I show on paper as income is much less than I actually make. Combining the past 2 years, my payment would put me at 46% DTI. My true DTI, just off of my last years taxable income is appx 30%. My Loan Officer is pretty confident. Her cover letter gave some very good contributing factors, Is that 46 too difficult to look over for an underwriter, or do my other factors outweigh that risk. I guess my questions are is that just too difficult of a number for an underwriter to justify?

Shaun,

Lenders will generally ask for the proposed monthly payment or use 1-2% of the outstanding balance to determine the monthly debt obligation. For FHA financing the debt can be ignored if deferred for at least 12 months from loan closing. So it depends on the loan type and lender, and what documentation you can provide. It may be helpful to know the actual eventual monthly payment because it will probably be lower than 1-2% of the balance.

I’ve heard of higher DTIs getting approved for VA financing, but you’ll have to wait and see.

I plan to apply for a home loan in a month or 2, but I’m waiting for one more hard inquiry to fall off to improve my score and to have most of my credit cards paid off. I make about $1200 to $1400 a month between two jobs. I spend about $350 to $375 a month on my dti and my credit score is 634. What are my chances of getting approved. Plus I have a down payment between $8000 to $10,000 to put down. But I want to keep my loan range $60,000 or less.

Elizabeth,

I can’t tell you with certainty that you’ll be approved, but if you get your score up and your income/jobs have been steady, a $60k loan seems reasonable. Your assets should also help. Good luck!

My loan is Not backed by Freddie/Fan and I have ARM loans with the balance on Loan 1 at $190,000 with 6.5% interest rate and Loan 2 $47,000 with interest rate 9.45%.

Home is underwater based on current market sales.

I am now 1099 and current before tax income is $17,4200 and monthly expenses is $4,575.44. I am not living in the home either bc my work is in a different state. What are my options besides selling?

Colin, my mid score is 695 and my monthly gross is 5720 would i still get a loan? my lo is saying my back end ratio is .5 over…..so i resubmitted everything for him to give to the underwriter. my total monthly debt with mortgage included is 2455 no late payments on my credit and 2 of my cc are close to the max bc of recent wedding

Justin,

That sounds like a tricky situation based on the occupancy and high LTV, might want to speak with some brokers/lenders about potential options.

Brie,

Since you can’t change your income, maybe you can reduce some of your other monthly liabilities to get your DTI lower or put more money down to reduce the mortgage payment?

My issue is a bit more involved but here is the crux of the matter. My income fluctuates from year to year. I got a 1 million dollar loan, however the two years that the bank asked for, my monthly average was about $6,400 my Mtg. payments are $6,900. I paid it for some time but I’ve run into a severe medical issue and I find it difficult paying my mortgage. Does the bank have any responsibility being that my DTI was at over 120%. There was additional money given to me as a loan under my business to pay off the land.

Manny,

That’s a tough one, not sure how the bank would view that. Hopefully they can help you out in some way if you are unable to make payments.

Looking to sell home, currently have high back end DTI , can we get pre approval if proceeds from sale of home be used to pay down debt as well as be used for down payment for new home?

Hi – I am preapproved for a mortgage and am in the middle of a purchase. However, I am using my 401k loan for the down payment and the repayments will greatly reduce my net pay. I did not want to do a distribution because of tax ramifications and the fact that my fiance will be living in the house with me, so we have no problem paying the mortgage with combined net pay. And, I want my retirement account replenished as soon as possible. I have very liitle debt, high income, and great credit scores. My worry is the UW denying the mortgage b/c of the 401k replayments.

I’ve heard that lenders cannot use your 401k loan payments in figuring your DTI. Is this true?

Kate,

It is true that loans secured by your own financial assets, such as a 401k loan, generally don’t count toward your monthly debt obligations. If you don’t want to take out a 401k loan, have you considered other options like having your fiance co-sign to avoiding tapping into your retirement?

Thanks Colin –

Yes, we did, but he had some serious credit issues from a setback during the recession, so it would have really hurt us when applying for a loan. They would have used his scores versus mine & we were told it was better for me to apply on my own.

It also kept us within a very manageable budget as he makes the same income as I do; the actual mortgage payment will be well within our household budget.

I rechecked my disclosures last night and an existing loan on my 401K is not showing as a liability. My new loan was simply rolled into that with a short payoff (hence the large hit to my net pay), but the lender preappoved me with the original small loan payment clearly showing on my paystubs. I’m assuming if they didn’t count the original loan & repayments as a liability/debt, then they cannot count the increased amount as one.

Thanks again for your reply!

Colin,

Thank you for this helpful article. I’ve enjoyed reading the comments and your responses as well.

Here’s my pickle. We currently own a home and need to upgrade. Given that we have a young baby and animals, we had always planned to buy and move into the new house before putting our current home on the market. Houses have been selling quickly in my neighborhood, but we plan to keep roughly 6 months of the current home mortgage in reserves, just in case it takes a while to sell.

Having just started looking for financing for the potential new home, my husband is being told that holding the two mortgages puts our debt-to-income ratio too high. Obviously we don’t plan to keep two mortgages permanently, just until we can sell the old house.

Do lenders have a way to account for this? I know we can’t be the only people who will have 2 mortgages for a few months. We thought that having the savings in reserve for paying mortgage #2 should suffice.

Any thoughts?

Katie,

Reserves are one thing, income and DTI are another. Unfortunately, if there’s no guarantee you’ll actually sell your old house, it’s a potential risk to the new lender. They can’t just take your word for it. Things don’t always work out as planned.

Check out Fannie Mae’s guidelines regarding a current principal residence pending sale: https://www.fanniemae.com/content/guide/selling/b3/6/06.html

Bought a fixer triplex with partners. It turns out, they are horrible and we want to buy them out.

The appraisal will be ok (the loan to value will be enough to pay them back). We have credit in the med-high 700s. My husband makes about 170K per year.

But we took and maxed a line of credit to buy and remodel this investment property. Although the rental potential is huge (we are running it as a short term rental) and I anticipate about $150k a year in rent, this is very far from 2 years of income to help lower our dti.

Will any banks consider this income (no leases as this is short term). How can we work around this?

Kelly,

Most lenders want a lease and history of rental payments in order to count future rent. Seeing that you’re going after short-term renters that might be tricky. Could try portfolio lenders if conventional guys won’t approve you.

I am trying to refi my home and consolidate two mortgages; I have a separate business that is handled from its own bank account and I file that income separately. Should that second/separate business be excluded from the calculations and consideration on refi due to how it’s filed with IRS and paid through business account?

Julie,

The business gain/loss should affect your other income and thus your DTI. You can’t really exclude things that could make you a higher risk to lend to.

Can improving your credit score increase the DTI allowed for a VA loan?

Meg,

Yes, it’s possible that a good credit score can be a compensating factor if your DTI is high.

They are trying to raise my husband’s mid score by doing a rapid re score to compensate for our current DTI of 54%. Our DTI is only high because he is self employed and we are not able to use all of his income the way he filed his returns. His current mid score is only a 639. At what score would we see a higher allowed DTI? We paid all debts off except a car loan a small business loan and one small credit card. Hoping this raises it enough.

Meg,

Typically you need really good credit for it to be used as a compensating factor. But the reduction of debt you guys paid off to boost his score may also push down the DTI.

Colin,

We are looking to move into a new construction home around $430K. We are going to sell our current home and with the equity can cover a 5% ($22,000) down payment. I have used a mortgage calculator and factored roughly what our new mortgage payment would be a month. I plugged that number in and our DTI comes in at 43%. My fiancée and I will both be applying and we have great credit scores 750+. Do you think we have a decent chance at being approved for this loan?

Thanks

Colin,

I currently receive $1750/mo. Social Security Disability, which is non-taxable income. Do all lenders “gross up” your SSDI monthly income by 25% to reflect the non-taxable status? If so, would the income used in the DTI calculation be $2,194 mo?

Also, if it’s not a case of a permanent disability, and eventually I might be able to work again, how does that affect your qualification for a loan?

thanks

Colin,

I’m currently approved by the USDA GUS and my lender with a 26.71/42.56 ratios, and tomorrow my lender will sent the file to USDA for final commitment. What are the chance of a denial if any?.

Thanks!

Arelys,

I’m assuming you already found out, but DTI is just one piece of the pie and as mentioned ratios can be exceeded. There are plenty of other reasons why you could be denied but hopefully you were approved.

Collin,

I have around $15,000 in the bank, a credit score of 730 and two car payments around $709 a month with making $58,000 per year and $0 cc debt. I recently went to apply for a conventional loan and got approved. The question I have is that I would like your input on my DTI. I should be around 39%-40% with a 1,000 mortgage a month for the house i am trying to buy. Do you see anywhere that i might not get financed for this house?

David,

On DTI alone it sounds like it shouldn’t hinder financing, but DTI is just one slice of the approval pie. Good luck!

Hi Colin,

I’m trying to refi my investment property but my DTI I a little higher than 50%. Where can I find a lender that will charge me the extra point to qualify?

Hi Colin,

I have a few questions in regards to the DTI rules.

1. Does the 43% DTI condition only apply to the first five years? Doesn’t this mean that banks can raise this number with mortgage payments along with it after the first five years?

2. What happens if a borrower has a DTI of 33% in the first year, but then 55% in the third year? Does he or she lose the loan?

3. Why doesn’t the DTI condition apply throughout the life of the loan?

Thank you!

Fatima,

Might want to try a broker who can search for a lender willing to work with a high DTI combined with investment property…

Jon,

Lenders don’t keep track of your income once your loan closes. They underwrite based on your past and expected income. I think it’d be impossible to make loans if you could constantly monitor the borrower’s income and make changes accordingly.

Hi Colin . I’m in the middle of obtaining a loan. I have been approved for FHA and MCC tax credit. They wouldn’t accept the DPA I applied for because it came with a higher projected house payment which sends my DTI over 45%. So I have to come up with a down payment. I don’t understand how the DPA is sending my ratio over 45%? Also, I got a standard deduction of 9250 on my taxes and they are subtracting that entire amount from my income. I only deducted 4K worth of things but the standard deduction was given to me. Does any of this make sense? What should I do?

Danielle,

You can gather second/third opinions to see if other lenders will be more forgiving.

They said the ratios DTI are high, almost 50%. What I don’t understand is that they qualified me for a FHA loan which almost has the same ratios guidelines as an USDA.

It’s a new construction and the developer had allowed $9,000 for closing costs.

Maybe I could get other lenders, but they told me not to get my credit involved, etc.

Thanks!

Madeline,

Maybe their automated underwriting system is approving FHA but not USDA…maybe they don’t want to make an exception and deal with the USDA? Could get second opinions to see what other lenders can do, or see if there’s a way to get the DTI down. If concerned about credit you can ask lenders not to run your credit initially to see if they can help first.

Hi Colin,

My DTI is coming out to be around 48.5% for a high balance conforming loan. I have good credit score >750.

My Wife is also working full time but she doesn’t have a strong credit history (<4-5 months). As she recently graduated. I am not able to use her income included in my DTI ratio.

What are my options. What are the chances that my loan would get approved. I am paying around 6% as down payment.

SF,

You’ll have to ask what the max DTI is then if it’s exceeded, determine if there’s a way to get the number down either by coming in with a larger down payment and/or paying off some liabilities to lower your DTI.

How long to most lenders require you to be with current employer?

Bree,

They prefer two years, but exceptions can be made if shorter assuming the job is in the same line of work, a promotion, recent grad, or some other reasonable situation.

I have a very good FICO 745 and i have some rental properties due to that

my DTI goes close to 50% now i am willing to pay 40% down payment

am i able to get the loan ?

Raj,

Might be some lenders that can go that high with compensating factors or automated underwriting. If not, might look at ways to get the DTI down such as paying down outstanding balances.

Hello, I’m looking to purchase a home in a state that I don’t work in, so it would be considered a second home. Income is about 270k/year. I have 46% DTI, 700 middle credit score. I have 2 credit cards- 1 I am going to pay off in 2 days and completely stop using it. The other I will have that paid off in 3 months. I have a 33k car loan and was wondering if I should max out my 401k to lay the 33k car loan. Also have LOADS of students loans. Thanks for your advice.

Stacy,

You might want to run some scenarios to see how low your DTI goes when paying off certain items…and also determine the max DTI you’re allowed with whichever lender ran the numbers (unless you ran them yourself). Also important is knowing exactly how student loans are calculated to ensure you don’t underestimate. Good luck.

Hello!

Thank you for all of the valuable information. We are looking to purchase in the next few months, but we are wondering how far mortgage companies look back for frontend and backend ratio. We don’t carry any debt month to month other than our current house, but we do put a lot of charges on our credit card (that gets paid off). We are curtailing our spending, but we also wonder if we should pay cash for our purchases as well.

HW,

For liabilities, they’ll look at your most recent credit report to see the minimum monthly payment(s) listed. So it can be beneficial to keep outstanding balances at or close to zero so there’s little or no monthly payment counting against your income.

Hi Colin,

I am in contract to purchase a new home from builder. I have been pre-qualified and pre-approved from the builders preferred lender. My current DTI is about 50%. With interests rates rising I can see my mortgage payment going up. Lender has not locked in a rate as of yet because the home will not be done until mid March. Also, I am in the process of selling my current home to have the down payment that the lender approved us with. Not sure I will even have the full amount. My concern is that I will not be able to afford the final monthly payment. The lender keeps reassuring me that everything is okay. I am worried. Your advice is appreciated.

MaryEllen,

One thing you can do is reduce any other monthly liabilities in the meantime…so any credit card balances you can knock down to zero to reduce associated monthly payments that will count against your income could help. May also want to ask specifically how high your DTI can go to ensure a rate rise won’t knock you out of the running. Good luck.

Hello Colin,

We are in the process of buying a new home from builder. We also are selling our current home to the original owners of our home. We plan to use the money from the sale to pay off all debt. Credit cards, loans etc. the only debt would show $50 from credit and my wife’s student loan $920. The student loan is a shocker since she has loan forgiveness and she doesn’t pay anything, we were told they take 1% and add as a debt. Our dti is around 44. We have excellent credit. My Fico is 836 and wife is 790. We are worried we will get denied. During the pre qualifiication process two lenders said we would have no problem. Should we be worried.

Jim,

It’s definitely a concern if the number is that high, but many lenders will go higher if your loan file is clean otherwise. It might be prudent to see how high they can go DTI-wise and what interest rate (if you’re not locked) would be the tipping point. Rates could rise in the meantime. Additionally, you may just want to be careful to avoid any new debt that could push any monthly liabilities on your credit report higher.

Looking,

Hmm…some lenders may allow for consistent and ongoing monthly draws from retirement to be counted toward income, but early withdrawals might not fly unless they’re somehow going to be regular withdrawals for the foreseeable future.

I am in the process of purchasing a home. I am almost at the end. I have gone through the underwriter process, have already been appraised. Part of the conditions of my loan was to pay off some of the debt I owed which I did by consolidating to one payment. I’m afraid this will now prevent me from getting the mortgage because my debt to income ratio is too high. I really don’t want to lose this loan. I noticed on the paperwork my car which is paid off was not included as an asset. Can this help in any way to secure the loan?

DeShunn,

An asset might be used as a compensating factor to allow for a higher DTI…otherwise there might be another option to get the DTI lower such as paying discount points to push the mortgage rate lower. Hopefully your lender can find a solution, good luck!

Hello Collin,

I am looking to purchase a home soon. However, I have students loans which I am on a $0 payment IBR plan. I was told by one lender that they will use 1% of the total student loan debt. I was also told by another lender that if I started to make payments on my own that the underwriter will use that amount as payments. I am not sure what to do.?

Lanay,

I wrote about this topic elsewhere on the site. In any case, you may want to get a pre-approval to see if you can qualify in all the scenarios or just certain ones, then go from there. Good luck!

My income is all tax FREE it dont make Lot of sense to me that the same dti ratios should apply

Scott,

Lenders take gross income, so taxes wouldn’t factor in anyway.

Hi Colin, i am preparing my figures (Profit and loss/ self employed) to do a modification on my loan. I am a bit confused on two things:

1: The 55% of debt to gross income requirement. My main question is, does that 55% of Gross income to debt ratio , include all expenses like groceries, internet, phone etc… + modified loan payment, OR JUST modified loan payment, + any revolving credit cards & HOA fees.?

2. If my profit and loss gave me my net monthly profit, wil they multiply that income by something to reduce ofr taxes or anything else?

Please share your knowledge on this one and thank you.!

Jonathan,

It really depends how the lender interprets it all, but generally DTI only factors in liabilities found on a credit report. So groceries and utility bills are typically not part of the DTI because they’re factored in elsewhere, like via credit card bills and so forth that do show up on credit reports with associated minimum payments. Not sure on the P&L bit, you’ll have to ask your lender how they calculate it specifically.

Hi Colin,

I need advice on my situation. My wife is planning to buy a house around 3/01/2018. Here is the situation; the house that she wants is about 250k in Virginia beach, VA. Her income is 50k a year, no debts except a car loan for $520 a month, her credit score is around 740. She has a saving of 20k but we planning on a minimum down payment. She wants to use the first time homebuyer program available in our area. I know 50k for a 250k mortgage sounds too high. The car loan is under her name but I use the car and I pay the loan since day one so that will be an issue for sure. My question is do you think she can get a 250K loan on her self according to the profile that I gave you?

Right now she is just saving as much as possible for next year so she can have at least 20 or 25k by 3/1/2018 and paying all her bill on time.

Now I know you are asking yourself why not to include myself on the loan or just transfer the car loan under my name, and the answer is that I recently file for chapter 13 but my wife is not included because we separated for a few months. I can afford the car loan and I will be paying it. also all expenses for our kids comes out of my paycheck, in other words she will only have the mortgage responsibility.

Edwardo,

It will depend on the down payment, the interest rate she receives on her loan at that time (they could be higher), and if the lender treats the car loan as your debt since you’ve been paying it (and can document that fact). You may want to get a pre-approval to address any concerns now so you’re prepared come next March. Good luck.

ok I understand. lets say we refinance the card and the payment comes down to $380. having the $380 a month and no other debts. with only 1% down payment (1st time H. owner) and the lowest today’s rate, making 50k. by your experience, what would be the max mortgage that I can get?

My husband and I are looking at buying a house. I’ve never owned a home. He hasn’t owned a house in almost 20 years. So we will qualify for first time homebuyer programs. Our middle scores are both at 600 and our DTI is around 54%. We moved states a little over a year ago for better jobs, but since we haven’t had current jobs for at least 2 years, they can’t include our mandatory overtime or my monthly bonuses that average $350/month. Otherwise our DTI would be around 47%. What types of loans do you think would be best to look into? I don’t want to have every company under the sun running our credit and putting more hard inquiries on our credit (literally the worst thing on our credit report is how many hard inquiries we have, hence why I want to avoid it as much as possible) I want to stick with only the most likely options. I know some inquiries will fall off our credit and we’ll have some loans paid off within the year, plus I get raises every 6 months, so our credit scores and DTI will both be a lot better within a year, however our current rental is not safe for our kids (and our landlords won’t fix anything), and due to Hurricane Harvey, there are very few safe rentals in this area that wouldn’t be charging an arm and a leg to rent due to the high demand, low supply ratio. That’s why we don’t want to wait another year to buy and why we’re anxious to find a lender who can work with us now. We even found a house that would be within our budget and is listed at $25,000 below appraised value. Our scores and DTI are what’s holding us back… And with 4 kids, we wouldn’t be able to put more than 5% down, and even that would be a hard stretch….

CJ,

Yes, you would be considered a first-time buyer, but that might not be necessary. As it stands, you’ll likely need to look at the FHA or USDA because of the low credit scores and high DTI. Ideally, you could work on upping your scores to 620+ to also qualify for a Fannie/Freddie loan as well. That would probably be my first step personally, but if time is of the essence, you might not have that luxury. The DTI is tougher but there are exceptions if you exceed 43% with compensating factors. And having down payment funds and some assets to spare is always helpful. The FHA only requires 3.5% down for 580+ credit scores and the USDA has no down payment requirement, but for the latter the home will need to be located in a rural area. You can also look at your state housing finance agency for even more flexible programs that are based on those already mentioned. Do some more homework and see if you get your scores up in the meantime. Good luck!

Hi! So my wife and I purchased a house and we are in our final push we are closing in 4 days and the lender is giving us problems we gave them all the information while back! we got approved for the mortgage! But now with four days left to go that denied us and all the paperwork at the lawyers are signed what should we do???

Would love some advice – I’ve been on Social Security Disability for the past 12 years and I’m currently 49. As a result, I have limited income, but had my student loans discharged due to my situation and pay off my credit cards monthly. My current home needs significant remodeling – only one of the three toilets and only one of the two showers are currently working. I’ve talked to two mortgage brokers I’ve worked with in the past about doing a cash-out refi and they say they can’t help me because my DTI is too high. I have plenty of assets (I could actually pay off my mortgage if I wanted to cash out my investments), but the only income I get is the social security, plus interest, dividends and capital gains on my various assets. My front-end DTI is 54.4% and back-end DTI is 56.7% (as I said, I pay off my credit cards each month).

I’ve thought about a HELOC, but although my LTV is great (about 38% right now) and would still be under 80% with the amount I’d want to take on the HELOC, and I have excellent credit (over 800), I still have that DTI problem. What are my chances of getting a HELOC anyway, despite that DTI problem?

The only other option I see is a pledged asset/securities-based line of credit (which was recommended by one of the brokers). However, it does not appear that the company where my IRAs/investments currently are offers this option and I am extremely happy with my current financial advisor planner and do not want to move my assets. Do you know of any other options?

Thanks for you time and assistance.

Michelle

Hi Michelle,

A HELOC might be a viable alternative if you can get the amount needed for the work. Perhaps a smaller line of credit will keep your DTI in check, and as you pay it back, you can borrow again as needed for the next phase of work. This can also keep your first mortgage untouched if the terms are good and it’s close to being paid off. Good luck!

Experian is reporting a High Estimated Debt-to-Income ratio of 82%.

My Monthly payments are correct, but my monthly income is shown as only half of what it should be.

How do I get the reporting corrected? My calculation shows a ratio of 42%. Thank you.

Steve,

It sounds like it might just be an estimate of income? I don’t know how good the credit bureaus are at collecting real income data. Is this a report you order yourself?